How To Reduce Taxes for High-Income Earners

Are you interested in learning how to reduce taxes as a high-income earner? Some individuals pay an income tax rate at or above 50%, depending on specific state and local taxes.

The unfortunate, but realistic truth, is that ultra-rich and well-informed individuals often pay lower effective tax rates than people making substantially less income. So let’s level the playing field and work toward equality. In this article, I will outline several key tax strategies I use and will educate you on making tax-smart moves like the top 1% do.

There are several tax-reducing strategies for high-income and mid-income earners that many financial advisors or CPAs may or may not bother to discuss with you. Some tactics are beyond their expertise, and others won’t earn them any additional money, so it’s not in their financial interest to overcomplicate their roles.

Nevertheless, I have learned several tax optimization strategies that I will share here to help you legally reduce your taxes. If you are into saving money, get ready for the entire journey- I’m going to share my tax-smart strategies that you can implement yourself.

Tax Basics and Legislation

High-income taxpayers typically fall into one of the top three federal tax brackets. Nevertheless, most tax issues and savings tactics apply to just about any taxpayer. Savings are usually more pronounced at the higher brackets, where each dollar is taxed at a higher marginal tax rate compared to lower-income tax brackets.

The SECURE Act

The SECURE Act was implemented in 2019 and significantly overhauled tax implications on individuals. The most notable updates for most individuals to be aware of include the following:

- The age for Requirement Minimum Distributions (RMDs) was raised to 72 from 70½. This delays when individuals must start withdrawing funds from their traditional retirement accounts and pay ordinary tax on the proceeds.

- The age limit was removed for Traditional IRA contributions. Individuals can now still contribute to a retirement account if they continue working past 72. Therefore it is possible to contribute and withdraw RMDs from a retirement account within the same year.

- New updates and increases to retirement account contribution limits, social security base wages, long-term care deductions, and income ceilings for Roth IRAs were established.

The takeaways from the updates to the SECURE Act are as follows:

If you continue to work and earn income after age 72, you are eligible and should continue contributing to tax-advantaged retirement accounts.

Updates to retirement account contributions and social security wages support the following strategy: You should aim to contribute as much as possible to tax-deferred retirement accounts during your working years.

Additionally, you should delay the start of your social security benefits as long as possible to benefit from the increases in base wage with the 8% increase per year for delaying your claim.

With proper planning, you can supplement any needed cash flow from your retirement account contributions and allow social security to grow with inflation adjustments and higher benefit premiums.

Above The Line Tax Deductions

There are two broad categories of tax deductions – above-the-line and below-the-line. “The line” is simply an accounting term separating adjusted gross income (AGI) from net taxable income (NTI). Simply put, “above the line” deductions reduce your income in the eyes of the IRS, while “below the line” deductions are additional tax breaks based on your AGI and tax status.

Above-the-line deductions may be more valuable if they reduce your AGI enough to qualify you for additional below-the-line tax deductions or tax credits. However, if you are a very high-income earner, then dollar-for-dollar, you will see little difference between above- or below-the-line deductions. Nevertheless, to stay organized, we’ll use these separate categories.

Health Savings Accounts (HSAs)

Health savings accounts are the most beneficial type of tax-advantaged accounts but are often ignored by most individuals. You can contribute to an employer-sponsored HSA account or open your own, as long as you qualify by having a high-deductible health plan.

Contributions to a HSA are not only deductible from your income, but the money grows tax-free and qualifying withdrawals are tax-free. Because of these three benefits, HSA combines the best of both a Traditional IRA and a Roth IRA.

Company retirement plan contributions.

A company-sponsored retirement plan would include retirement account types such as a 401(k), 403(b), 457(b), or Thrift Savings Plan. Additionally, several options for self-employed individuals (covered in the retirement account article) offer the single most significant above-the-line deduction opportunity. High-income earners looking for maximum tax deductions should consider contributing the maximum amount possible towards eligible retirement accounts.

Deductible Traditional IRA Contributions

Contributions to a Traditional Individual Retirement Account (Traditional IRA) may be deductible if you are not offered a company-sponsored retirement plan, such as a 401(k).

Additionally, depending on your income level, you can make a deductible contribution to a Traditional IRA, even if you have access to a company-sponsored plan.

Backdoor Roth IRA Contributions

Are you above the income limit for making a deductible IRA contribution in addition to your 401(k) contribution? In this case, you can still take advantage of a backdoor Roth IRA contribution, a tremendous tax-saving technique for high-income earners.

Qualified Charitable Distributions

A qualified charitable distribution is a distinct type of charitable contribution distributed to a charity directly from an IRA, available for individuals over 70½. If you are charitably inclined and receiving required minimum distributions from a Traditional IRA, this method is likely the most favorable source for your charitable gifts.

Charitable Gift Annuities

Charitable gift annuities are a particular type of contract between the donor and the non-profit, charity, or university. Charitable gift annuities are complex and make sense for individuals looking to receive cash flow from an asset with a significant amount of unrealized capital gains.

For example, let’s say you invested or received stock in a startup with a low cost basis, but now the stock is worth $10 million. In this case, you could donate the stock to a qualified institution. However, unlike a traditional donation, in a gift annuity, the non-profit would structure a series of annuity payments back to you based on the total value of the stock (because they have more preferential tax treatment as a non-profit).

Structures are custom-built by the endowment or fund manager of the institution and, in many cases, will offer a larger net cash flow than you would realize by selling the securities and recognizing all the capital gains yourself.

In summary, this is an effective way to tap a large, unrealized capital gain without selling the asset and realizing a sizeable taxable capital gain. The relationship is worthwhile for the institution as they will realize the value of your pre-tax assets over your lifetime.

Below The Line Tax Deductions

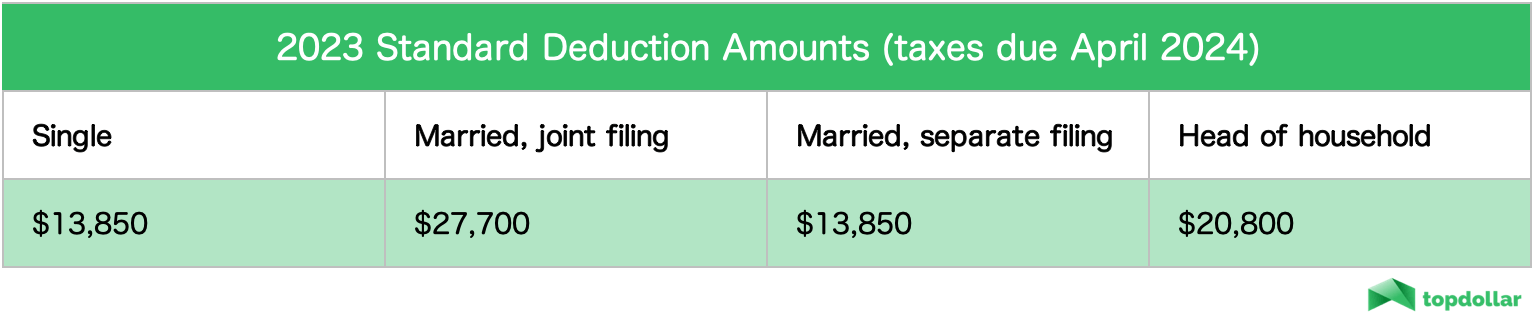

When it comes to below-the-line tax deductions, 90% of taxpayers will take a standard deduction instead of choosing to itemize deductions.

High-income earners may have a more challenging time itemizing above the standard deduction than in the past, primarily due to the passing of the Tax Cuts and Jobs Act (TJCA) in 2017.

TJCA doubled the standard deduction but eliminated many itemized deductions to discourage itemizing, notably on Schedule A of a tax return. Most notably, TJCA limited the deduction for state and local taxes (SALT) to $10,000 for couples filing jointly or $5,000 if married filing separately.

There are a plethora of tax credits and changes that we made under TJCA. Further in this article, the most substantial itemized deductions are detailed.

Charitable Contributions

If you are inclined to make a simple charitable gift, contributions are below-the-line tax deductions that could be made in the form of cash or assets.

Donating appreciated assets with unrealized capital gains is the most tax-efficient method of making a charitable contribution dollar-for-dollar. For example, if you want to donate $1,000, consider donating $1,000 worth of appreciated stock instead of cash.

Stacking Charitable Contributions

Stacking contributions refers to the practice of making charitable donations in grouped clumps in the same taxable year instead of spread out over time. The benefits of this practice are twofold.

Stacking contributions can raise your itemized deductions above the standard deduction threshold in some years if you do not exceed the threshold every year. For example, if you make a charitable contribution in a year where you are still under the standard deduction limit, you will not receive any additional tax deduction for this donation. However, moving this donation to a year in which you are above the standard deduction and itemizing will allow you to add this contribution to your total itemized deduction.

Furthermore, because marginal tax rates increase as your AGI increases, stacking contributions allows you to optimize your deductions at higher tax bracket rates. Put another way, dollar-for-dollar gifts create a larger tax deduction the higher your tax bracket.

Mortgage Interest Expense

Mortgage interest on a primary home is still tax deductible, up to $750,000 in loan principal. Mortgage interest is usually a significant source of the itemized tax deduction for tax filers choosing this method.

Medical Expenses

Medical expenses are tricky because they can only be deducted if they are substantial relative to your income. Currently, medical expenses for you or your family that exceed 7.5% of your AGI are allowed as an itemized deduction.

Qualified Accounts for Income Tax Deferral

Income tax deferrals refer to above-the-line deductions in qualified accounts (tax-advantaged accounts). These deferrals as the most straightforward way to reduce taxable income.

If you are a high-income earner (in the top tax bracket), I recommend taking the immediate tax deduction offered from qualified retirement plans and education savings plans (assuming you are saving for education costs).

Qualified Retirement Plans

As mentioned above, high-income earners should undoubtedly be maximizing their retirement account options. Not only should you maximize your employer-sponsored plan – 401(k), 403(b), 457, SEP IRA, SIMPLE IRA, or Solo 401(k), but you should also be contributing to a Roth IRA, even if you are over the income threshold and need to backdoor the Roth IRA because you are over the income thresholds.

Education Savings Plans (529 plans and Uniform Minors Accounts)

Although 529 contributions are not exempt from federal taxes, they are exempt to some degree from state-level income tax. Additionally, money grows tax-deferred and qualified withdrawals are entirely exempt from future taxes, much like a Roth IRA or Roth 401(k).

529 plans also allow for “super funding,” contributing five years’ worth of contributions simultaneously. By itself, super funding will save you little on taxes. However, when you consider the improved compounded returns over time, you can reduce the total contribution you will need to invest for tuition expenses.

Additionally, a Uniform Minors Account can also allow for a small (but why skip it?) tax deduction.

Health Savings Account

As mentioned previously, Health Savings Accounts (HSA) are not extensively used by everyone, but their tax benefits are fantastic. HSAs are eligible for individuals with high deductible insurance plans, regardless of whether they are employed individually or through a company.

Health Savings Accounts not only let you take an immediate tax deduction (above the line) against your income but the money can be invested and withdrawn tax-free as long as it’s used for qualified medical expenses.

Other Taxable Income Deferral or Acceleration Methods

Savvy individuals do not just try to defer taxes from one year to the next but rather take a long-term strategic approach to allow returns to compound with as little tax drag as possible.

Deferred Compensation

If you receive compensation based on performance-based results (such as sales, profits, deals, etc.), you may want to see if your employer will offer deferred compensation.

Some employers offer specific deferred compensation plans, but in other cases, you may ask if they could defer your end-of-year bonus or compensation from the end of one tax year to the beginning of another. This is often not a big issue for small companies or partnerships.

For example, my former company’s variable compensation accounted for over 80% of total annual compensation. After discussing the tax implications of ‘good years’ vs. ‘bad years,’ we put a structure in place whereby we could pay end-of-year performance bonuses either the last week of December or the first week of January, depending on annual company performance.

Accelerated Compensation

Increasing Tax Rates

A tax-savvy investor keeps an eye on tax rate legislation. For example, the current reduced tax rates are set to expire in 2025, meaning it makes sense to accelerate gains or income if possible if you will otherwise need to realize it the following year.

By no means do I suggest that you realize gains on long-term investments to save an extra few percent. Still, it makes sense to realize the gain under the lower tax brackets if you will be cashing in some gains or receiving deferred compensation that you plan to use for a large expense in 2025 or 2026.

Roth Conversions

Furthermore, in years of low compensation, there may present a window to convert a Traditional style retirement account (Traditional 401(k) or IRA) into a Roth account. This conversion does realize tax but may make sense if you are presented with a temporary, lower tax bracket.

Deferred or Accelerated Retirement Account Withdrawals

Savvy planners budget how much money they will need to support the cash flow of their lifestyle – and try to realize capital gains in years of lower tax brackets, but never more than they anticipate needing for expenses.

Retirees should always consider their current tax bracket before making additional withdrawals from their IRA or 401(k) beyond the requirement of required minimum distributions. Not only does money in retirement accounts continue to grow tax-free, but it is also taxed at ordinary income rates. Therefore over-withdrawing from these funds is the least efficient method of funding.

Invest Your Money With a More Favorable Tax Status

Municipal Bonds

It is no secret that municipal bonds offer increased value for high-income earners. Although municipal bonds offer lower interest rates than comparable non-tax-exempt bonds, their tax-adjusted yield makes them more attractive for individuals than taxable bonds for individuals in higher tax brackets. Municipal bonds purchased in your own jurisdiction are triple-tax-exempt.

Passive Index Investing

Investing in tax-efficient passive index funds keeps management fees low and your returns high. Additionally, using either passive ETFs or mutual funds, you can further reduce your tax liability and let your diversified investment grow without unnecessarily realizing capital gains.

Passive ETF index funds conduct tax-efficient rebalancing and minimize taxable capital gains distributions – making them my favorite type of investment. Investing in passive index funds over individual stocks removes the need to rebalance your portfolio often and can avoid realizing capital gains while maintaining a diversified portfolio.

Manage Your Portfolio’s Taxes Wisely

Savvy high-income earners should always ensure they do not needlessly realize capital gains. Sticking with passive index funds is the first step to gaining more flexibility when minimizing taxable gains, as we’ll discuss below.

Time Your Capital Gains and Tax Loss Harvesting

Investing in low-fee passive index funds is an intelligent tax decision for most investors. Not only will your portfolio be well-diversified, but these funds avoid the need to trim specific outperforming stocks and pay unnecessary gains because of their distributed risk across various companies.

Make sure not to realize gains or rebalance a portfolio unless it is absolutely necessary to stay within the confines of your investment plan.

Tax loss harvesting is an efficient method for minimizing capital gains taxes. All investors should always review their realized capital gains throughout the year and determine if there are losses that should be taken (realized) against the gains.

Savvy investors should also look to harvest losses for the future when the stock market is down- regardless of whether they have current gains to offset. If you are investing in passive ETF index funds (as I recommend), you can simultaneously roll from one passive ETF to another similar (but not identical, for wash sale purposes) to lock in capital losses when the market is down. This loss can be carried forward indefinitely to offset capital gains in future years.

![]() Top Dollar Edge: $3,000 of harvested tax losses can be against ordinary income per year if you don’t have any capital gains to offset. Losses over $3,000 will be carried forward and can be offset again in future years.

Top Dollar Edge: $3,000 of harvested tax losses can be against ordinary income per year if you don’t have any capital gains to offset. Losses over $3,000 will be carried forward and can be offset again in future years.

Advanced Methods To Avoid or Manage Capital Gains Tax

1031 Exchanges

Avoiding capital gains tax is an important tactic that separates the tax savy from most ordinary investors. Unfortunately, there are not too many techniques to completely avoid capital gains tax, but 1031 exchanges are the gold standard when investing in real estate.

1031 exchanges allow you to roll the proceeds from a property sale to another similar type of property without realizing capital gains or having to pay back depreciation deductions you took prior.

1031 exchanges can also allow you to ‘step-up’ a personal vacation home or second property similarly. You would still be able to use all the proceeds from a property sale to purchase the new residence free of tax.

Deferred Sales Trust on Capital Gains

Sometimes a seller may not qualify for a 1031 exchange due to multiple factors, such as short-term holding or an inability to identify a qualifying property within the required tax window. In the absence of a 1031 exchange, some investors choose to use a deferred sales trust to roll the sale of real estate into a trust.

This trust is an effective vehicle to dispose of the asset and control the size and timing of the proceeds. Smaller distributions from the capital gain can be made to the owner over the years, thereby delaying the realized capital gains. The owner would only realize capital gains as they take distributions from the trust and could delay this out over many years depending on their cash flow needs.

The best part is that the trust can still invest the gross proceeds from the sale into various investments or assets, so compounded returns can still be gained on the gross proceeds without having to first pay the capital gains tax on the sale.

The downside of a deferred sales trust is the need and cost of hiring an expert to establish and administer this specialized vehicle. Additionally, most firms specializing in creating these trusts also charge an annual management fee.

Because of the extensive costs, deferred sales trusts are only viable for huge capital gains tax scenarios with a tax liability of at least several million dollars.

Qualified Opportunity Zone Investments

Qualified Opportunity Zones (QOZ) did allow investors to defer realized capital gains on certain investments if the proceeds were reinvested into economically challenged communities.

Although the incentive for deferring capital gains has lapsed, the growth of QOZ investments is still tax-free, providing a valuable benefit to this program that may still be worth pursuing.

Conclusion for Reducing Taxes

High-income earners can reduce their income taxes through the various tactics mentioned above.

Taxpayers should always maximize above-the-line and below-the-line tax deductions and maximize the use of tax-advantaged accounts such as HSA plans, retirement accounts, and education savings plans.

Furthermore, individuals should make sure to consider more tax-advantaged vehicles, such as passive index ETFs and municipal bonds, and always avoid realizing capital gains taxes whenever possible.

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.