What Is Tax Planning? Strategies, Concepts, and Techniques

It is often said that, other than death, the only guarantee in life is paying taxes. And while this perspective might be a little bit morbid, it is undeniably true. Understanding taxes plays a very important role in the world of financial planning.

Anyone who wants to establish lasting financial stability will need to consider how proper tax planning affects their finances. Depending on your current financial situation, your tax obligations might equal as much as 50 percent of your pre-tax income. That’s a figure that most people simply cannot afford to ignore.

Luckily, there are a lot of things you can do to dramatically improve your current tax planning strategies. In fact, with the right tax plan in place, you can accurately forecast your future tax obligations and also minimize your total tax obligations.

Let’s take a closer look at the most important things you need to know about creating a personal tax plan:

What Exactly is Tax Planning?

Tax planning is a relatively broad term that includes all components of financial planning that are related to taxes. Generally, “tax planning” will involve looking for ways to minimize your tax obligations, along with looking for ways to predict what your future federal income tax obligations might be.

There are a lot of different resources available to help you with tax planning, including certified financial planners (CFP), accountants (CPA), resources provided by your bank or credit union, and more. However, I have learned that no one is more motivated than you to learn ways to lower your taxes, so I always self-education instead of relying on experts.

Many people assume that their taxes will be done “automatically” or that tax planning is a luxury service reserved for the ultra-wealthy. But this is simply not the case—anyone who has an income should develop a personal tax plan. In fact, the lack of tax planning is why the American population overpays their taxes by billions of dollars every year.

Who Needs to Tax Plan?

Everyone needs to create a tax plan. Regardless of your current work situation, your income, your marital status, and every other personal detail, all citizens of the United States will have an ongoing financial relationship with multiple governing authorities. Even if your expected tax obligation for the year is $0, that is still a “financial relationship” that can present valuable opportunities, such as rolling over a retirement plan, while you are out of work.

Without a detailed tax plan in place, you will end up leaving your financial future to chance. In some cases, intelligent tax planning could help you reduce your ongoing tax obligations by 20 percent, or even more. Over the course of a lifetime, this could amount to saving hundreds of thousands, even millions, of dollars.

In other words, tax planning is a really big deal. This is why Americans, collectively, spend about $12 billion on tax preparation and related services. By using the most effective tax planning strategies, you can minimize your tax liability, increase your likelihood to qualify for tax breaks, and otherwise reduce your federal income taxes.

Understand How Your Income and Investments are Taxed

In general, anytime you have money flowing in, that money will be subject to some sort of tax (unless it’s already been taxed, such as a Roth IRA). That means it will be important to understand who is responsible for taxing your cash flows, along with how your cash flows will be taxed.

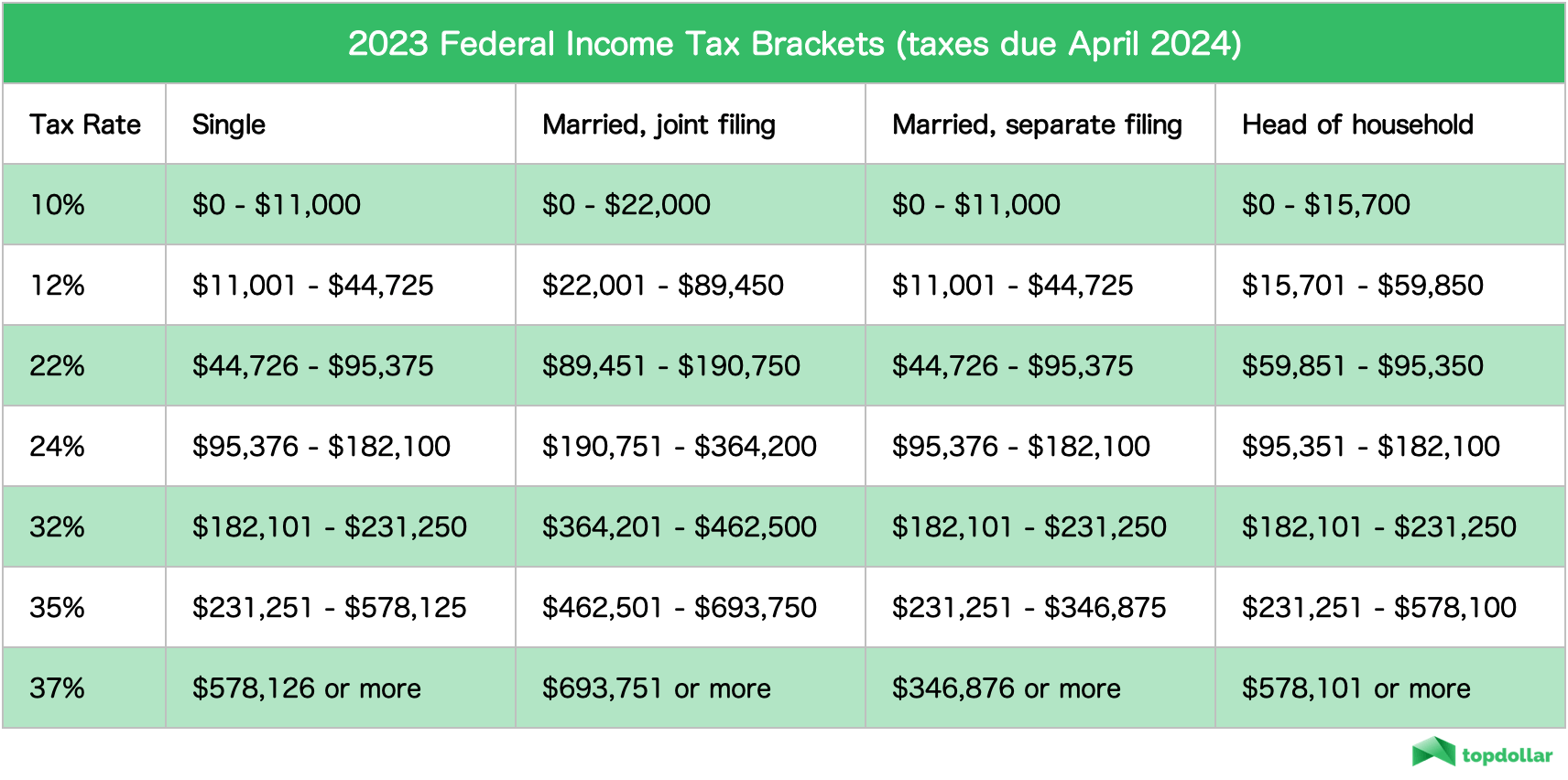

Tax Brackets

The United States—along with most other countries—uses a progressive tax bracket system. This means that, at least for ordinary income, the more money you make the more you will end up paying in taxes.

Tax brackets are applied marginally, meaning that the tax bracket you are “in” does not necessarily apply to all of your income. Instead, it applies to the next dollar that you earn. This means that, contrary to what many assume, there will never be a situation where moving “into the next tax bracket” will end up costing you money.

Suppose you generated $50,000 in taxable income last year. Despite what you might assume looking at the chart above, your average personal tax rate will not be 22% (that is only your marginal tax rate). Instead, your marginal rate will be slightly less

In this example, you’ll pay 10% on your first $9,950 of income. Then you’ll pay 12% on your next $30,575 of income. After that, you’ll pay 22% of all remaining income.

In the example above, this means your total federal tax bill is $6,748.50. This is notably less than what you’d pay if your tax rate had been 22% for every dollar ($11,000).

Identifying Taxable Income

Having these figures in hand will be incredibly useful whenever you are creating a personal tax plan or tax strategy. But of course, we still haven’t covered the whole picture. After all, the current IRS tax code is more than one million pages long. We will also need to consider the type(s) of income you are generating, as well as the effects of tax deductions and tax credits.

Ordinary Income vs. Capital Gains

When you are filing your taxes, you will need to “declare” your income for the given tax year. In general, income represents any positive cash flow into bank accounts that you earned. In some cases, your corresponding expenses might be greater than your claimed income. But in both situations, this income will need to be “declared.”

When declaring income, the IRS will ask you to clarify the type of income that you are declaring. The majority of income in the United States is “ordinary income”, which is income that is generated from wages, salaries, and interest from certain accounts.

Whenever you declare ordinary income, it will be subject to the ordinary income tax rate. Most people who declare ordinary income will file their taxes with a W-2, 1040, or a comparable tax form. In some cases (especially for W-2 tax filers), the amount of money owed to the government may have already been withheld from your paycheck.

But there are other ways of generating income, as well. For example, if you have recently sold any stock, sold your home, or sold another “investment vehicle”, then you may have generated capital gains.

What Does the IRS Consider a Capital Gain?

To the IRS, a capital gain occurs when you sell a capital asset for more than you initially paid for it. So, if you bought some stock in a company for $40 and eventually sold that stock for $50, you will have generated a $10 capital gain.

Income that is generated through capital gains is often treated differently than ordinary income. In most cases, the capital gains tax will be significantly lower than the ordinary income tax.

However, as we will further explain below, not all capital gains are taxed the same way. Specifically, long-term capital gains will be subjected to lower tax rates than short-term capital gains.

Long Term vs. Short Term Capital Gains

If you are investing in any sort of capital asset, the profit you gain from holding that asset is considered a capital gain. Capital assets are a broad category of investments that includes stocks, real estate (with exceptions), collectibles, bonds, other securities, and more.

Generally, in order for something to qualify as a “long-term capital gain”, you must hold possession of that asset for at least one year. Once you have held the asset for a year, it will be treated as a capital gain, meaning that your marginal tax rate for whatever you earned will be between 0% and 20%.

On the other hand, if you hold onto the asset for less than a year, any earnings you gain from that position will be taxed as ordinary income. This means that short-term trading strategies—while effective, at times—are not considered long-term capital gains. The tax you will need to pay for trading will be notably higher than if you sold your capital after holding it for a year.

Maximizing Tax Efficiency

In the world of personal tax planning, the term “tax efficiency” describes the portion of your gross income that will be subject to various taxes. Ultimately, this means it will be important to think about how long you are holding onto each of your capital assets.

If, for example, you are thinking about selling a stock you’ve held onto for 11 months and 20 days, it might be worth holding onto that stock for another two weeks in order to get taxed at a lower bracket.

When preparing for capital gains taxes, there are a few other details you’ll want to keep in mind. When prepping your taxes, your capital losses can be used to deduct your capital gains, meaning that your projected tax bill can be lowered by offsetting capital gains (assuming they have been locked in or realized).

Additionally, it is important to note that art, jewelry, real estate, and a few other asset classes have limits, deductions, and exceptions available for anyone who has profited from holding them.

Current Bracket vs. Future Brackets

When creating any sort of personal tax plan, it is important for your tax plan to be as comprehensive as possible. That means in addition to accounting for what your tax obligations are in the current year, you should also consider what your tax obligations might be in the future.

If you believe you will be in a different tax bracket in the future, then that might have a tremendous impact on your tax planning strategies in the status quo. For example, if you believe your income will be much greater in the future, then you might want to consider establishing a Roth IRA instead of a Traditional IRA. (This allows you to pay the taxes on your retirement contributions now, rather than later).

So, when tax planning, be sure to think about how your income is likely going to change over time—and be realistic with your income expectations. But additionally, you should also consider how the tax brackets themselves might change in the near future.

Right now, there is a considerable amount of debate regarding how Americans are taxed. But one of the most common sources of debate is whether state and local taxes (SALT) will be completely deductible. If you live in a state with relatively high-income taxes (NJ, NY, IL, CA, etc.) be sure to keep track of how SALT deductions are applied.

When Do I Need to Pay Taxes?

An important component of the tax planning process is knowing when your tax bills are actually due. While many people will have their tax liability automatically withheld from their paycheck, others might need to make quarterly payments on their own, especially people who file IRS Form 1040 (self-reported annual income).

What are Tax Deductions?

Now, let’s take a look at common tax deductions—which can potentially save you thousands of dollars per year in income tax.

A tax deduction is a specific item on your tax return that reduces your taxable income. With the right tax planning strategy, you can significantly reduce your tax burden and minimize the pain of paying taxes.

Suppose your taxable income is $80,000. And suppose you qualify for a $1,000 tax deduction. When applied, the tax deduction will reduce your taxable income to $79,000. In the end, this deduction won’t end up saving you $1,000; however, you’ll still end up saving about $200, which is why tax deductions are always worth pursuing.

The Standard Tax Deduction

The most common tax deduction utilized in the United States is the standard deduction. This is the amount that anyone can deduce their taxable income by, if they choose to do so. Current standard deduction rates for this year’s taxes can be found here.

In most cases, taking the standard deduction will make sense. But if you currently have a lot of business-related expenses, it might make sense to itemize your tax return and reduce your taxable income even further. Utilizing itemized deductions and other tax savings opportunities can potentially save you thousands of dollars per year.

If you do decide to itemize, be sure to consider the following tax deductions:

Common Tax Deductions

As suggested, tax deductions will reduce your taxable income. Here are a few of the tax deductions that can help reduce the amount of money you owe to the government:

- Capital Losses Deduction: This helps offset any losses you’ve accrued while selling your assets.

- Charitable Contributions: Any contribution you make to qualifying charities can be deduced from your taxes.

- Retirement Contributions: Contributions that are made to qualifying accounts (IRA, 401k, etc.) can be deducted under certain circumstances.

- Education Expenses: If you are currently paying for your own education, you can likely deduct associated expenses.

- Medical Expenses: Most medical expenses—including dental and vision—are tax deductible, but only if the bills exceed a significant portion of your income.

- Home-Owner Deductions: A lot of homeowner expenses can be deducted, including mortgage interest expenses, property taxes, and even home office expenses.

- Business Deductions: Almost any expense associated with your business can be deducted, which is why it is crucial to keep detailed records.

- Disaster/Theft Losses: Even if you’ve received payment from your insurer, you might still qualify for disaster and theft deductions.

- Family Deductions: If you have dependents, you might be able to qualify for deductions via a Dependent Care Flex Spending Account and other options.

- SALT Deductions: Depending on your current situation, the taxes you pay to your state and local government might be deductible.

These are most of the common tax deductions you might encounter.

What are Tax Credits?

Tax credits are similar to tax deductions in the sense that they both remove the amount of money you will end up owing to the government. However, when all else is equal, tax credits are better than tax deductions. These credits not only reduce the income that will be taxed—they directly decrease your total tax owed.

Let’s suppose your income for the year was $85,000. If you have a $1,000 tax deduction, that means the amount you are taxed will be reduced from $85,000 to $84,000. Using current tax brackets, this means that a $1,000 tax deduction will end up saving you about $220.

With a $1,000 tax credit, on the other hand, your tax bill will be reduced by a clean $1,000. In this situation, a tax credit is about four times as valuable as a $1,000 tax deductible. As a result, tax credits should be made a top financial priority.

Common Tax Credit

Tax credits are one of the most effective ways to reduce the amount of money you owe the federal government. And this can be applied on the Federal, State, and Local levels. Be sure to check out these tax credits:

- Family Credits: Utilizing the Child Tax Credit—along with several others—can help significantly reduce your ongoing tax obligations.

- Education Credits: If you are currently engaged in any sort of secondary education, there will likely be a corresponding tax credit.

- Earned Income Tax Credit: This credit is ideal for low and middle-income taxpayers—just be sure to double-check that you qualify.

- Homeowner Credit: In addition to the deductions mentioned above, you might also qualify for credits, such as clean energy credits.

When combined, using both tax deductions and tax credits can put you in a much better financial situation.

Tax Refunds: Giving Uncle Sam an Interest-Free Loan

While getting a tax refund might be nice, it’s important to realize that getting one means you overpaid the government. A tax refund is merely the government giving you money back, and doing so without interest!

With better tax planning strategies, you can eliminate the need for a tax refund and keep the money you’ve earned. But, furthermore, a personal tax plan can help you reduce the total amount you owe and prepare you for a better financial future.

Further Tax Saving Resources

Want to learn more actionable tax-saving ideas, check out the following resources:

- Individual vs. Roth retirement accounts.

- How to make your own financial plan.

- Choosing an education savings plan to save taxes.

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.