Financial Planning: Why You Need an Investment Plan

Do you ever wonder how much you really need for retirement? Do you feel unsure if you are investing your 401(k) optimally or wonder if you are earning too little return on your money? These are all questions that a good investment plan will cover. Having an investment plan will save you the time and stress of doubting your money decisions so you can spend more time living your best life.

If I randomly jump in my car and try to drive cross country without a map, perhaps I might make it to my destination. It may take me an extra day or week. But give me a road map, and I’ll be there in three days flat. Your investment plan is your road map, and a little planning will save you a lot of trouble.

After fifteen years as a market strategist and investing through the crashes of 2008 and 2020, my returns have significantly beaten the market. Why? Not because I took any unreasonable risks or got incredibly lucky. I performed well because I had a solid investment plan that provided me with the strategy and flexibility to buy and rebalance my portfolio when the markets became volatile.

Having an investment plan is not only a road map to accomplishing your financial goals, but it also acts as your playbook for improving risk-adjusted returns when the stock market presents opportunities.

What is an Investment Plan

An investment plan is your specific money strategy that starts with your current financial situation today and sets your path forward to achieving your long-term goals. But before you jump into charting your path, you first need to identify where you are today and where you are going.

A sound plan begins with a snapshot of your current finances- debt, income, tax rates, retirement savings, brokerage accounts, real estate holdings, and any alternative assets you may hold. Your total assets minus your total liabilities (debt owed) equals your current net worth (which could be negative).

If your current financial situation includes any bad debt, your first priority is to set a plan for getting out of debt.

Assuming you have no debt (not including a home mortgage or student loans), you then need to take a look at your household’s net income vs. budget to determine how much money you can reasonably plan to save per year.

Next, you need to set your long-term goals, such as homeownership, college tuition savings, or any other large purchases you are working toward achieving. Lastly, you need to determine your retirement savings target, which is usually the most challenging and most important goal.

Make an Investment Plan

I assume at this point, you are already at step #5 on your path to building wealth and financial freedom. You should understand where you are financially and where you are going. After you have already put together an emergency fund and removed any bad debt, you can begin to build your investment plan.

Building your plan requires some basic understanding of the differences between various asset classes and risk vs return. If these terms are unfamiliar to you, I recommend starting here.

Stock Market Risk Tolerance

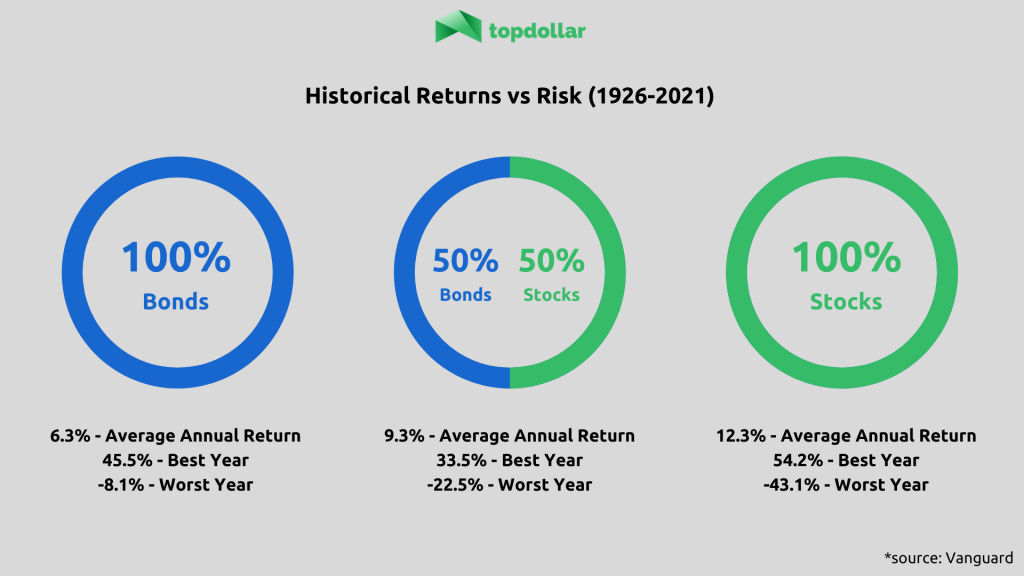

You can play with the allocations of different assets to understand how your savings may grow with more savings in risky assets (such as stocks) as compared to bonds or cash. I always recommend diversifying using index mutual funds or ETFs. These funds allow your investment to gain all the benefits of growth and dividends while removing most company-specific stock risks.

You should test several different allocations between stock, bonds, and cash (and for more sophisticated investors- commodities, real estate, and alternative types of investments) to determine what total value your net worth could grow under different allocation options. This step is where you need to consider how much risk you are willing to take.

Your goal is not to take on more risk than you are comfortable with, but to understand what you can expect to achieve under different allocations. Ideally, you take the least risk possible necessary to achieve your financial goals. Furthermore, you should plan to take on less risk over time as you get closer to retirement.

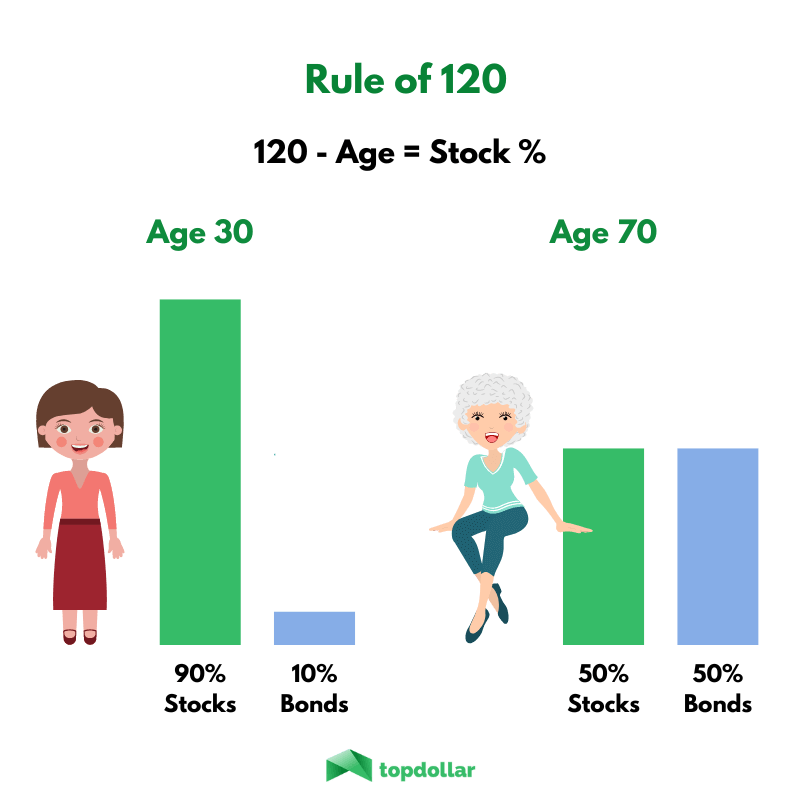

The rule of 120 is not sacred, but rather an intelligent guideline that suggests how time until retirement should affect your stock allocation. In the event that you lose money during a market downturn, you would not have as many years to wait out a recovery.

Remember, there are no guarantees as to real returns. The best any financial advisor can do is use historical returns to try to estimate likely outcomes in the future. I recommend assuming returns of 6.5% for stocks, 4% for bonds, and 0% interest for cash over the long term. It is a good idea to be a bit conservative to ensure you will have enough money in the end.

Setting Financial Goals

Investors need to consider how much they specifically need for retirement, what their future tax rates will be, and how much they will need for large expenditures. At the same time, you should be conservative, plan for moderate inflation over the long term (2-3%), and have a backup plan in case you do not reach your goals. If you choose the do-it-yourself financial planning method, make sure to include all these factors in your sheets and models carefully.

The main goals and vehicles used by most investors should include the following:

The math in your plan should add up to allow you to reach your milestones. The more buffer, the better. Every year you should review your plan and updated financial situation to see if you are still on track toward your goals and consider if any goals have changed. You have several options if your plan no longer achieves your targets.

How Can an Investment Plan Grow Your Wealth

There are several ways an investment plan can directly lead to greater wealth.

Increased Savings

On the most basic level, planning identifies the pitfalls that most individuals otherwise don’t recognize in order to meet their desired goals. By understanding the savings or returns required to achieve one’s goals, you become empowered and have the actionable knowledge to improve your financial position.

If you are behind on your financial targets, your choices are straightforward: either save more or earn more. By knowing what you actually need to do, most individuals will be better equipped to accomplish their goals. It can also be invigorating to see how much you could save from the power of compounding returns!

Portfolio Rebalancing and Asset Allocation

Rebalancing opportunities can provide opportunities for increased returns. For most investors, building wealth does not come down to stock picking, but rather is based on intelligent asset allocation.

“The most fundamental decision of investing is the allocation of your assets: How much should you own in stocks? How much should you own in bonds? How much should you own in cash reserve?”

-Jack Bogle, the founder of Vanguard

Once you have a target allocation that reflects your preferred risk vs. reward profile, you have a strategy for behaving in volatile markets. Contrary to popular opinion, market crashes and volatile markets are not a time for investors to sit and wait on the sidelines. The volatility that occurs during uncertainty is a key opportunity for investors to rebalance their portfolios.

Rebalancing gives you a tactic by which you can buy more stocks as they decline, and trim some stocks as they go up. This reallocation from overperforming to lower-performing assets keeps your risk tolerance consistent while adding more stocks at discounted prices.

Tax Savings

You can take advantage of essential tax benefits by increasing your financial literacy and performing sound financial planning. The rich do this all the time, by taking or delaying taxes to redistribute their taxable income.

Tax planning is foundational to effective financial planning, and not taking advantage of tax savings can cost you a fortune over a lifetime.

Any tax-advantaged accounts such as retirement plans or education savings plans should always be utilized to the maximum contribution limits. After using these tax-smart accounts, an investor should consider their current vs. future marginal tax rates to determine if there are more sophisticated tactics available. Some intelligent techniques include recognizing or delaying taxable gains, tax loss harvesting, setting up a backdoor Roth IRA or rolling a plan into a Roth.

Should I Make My Own Plan or Hire A Financial Planner?

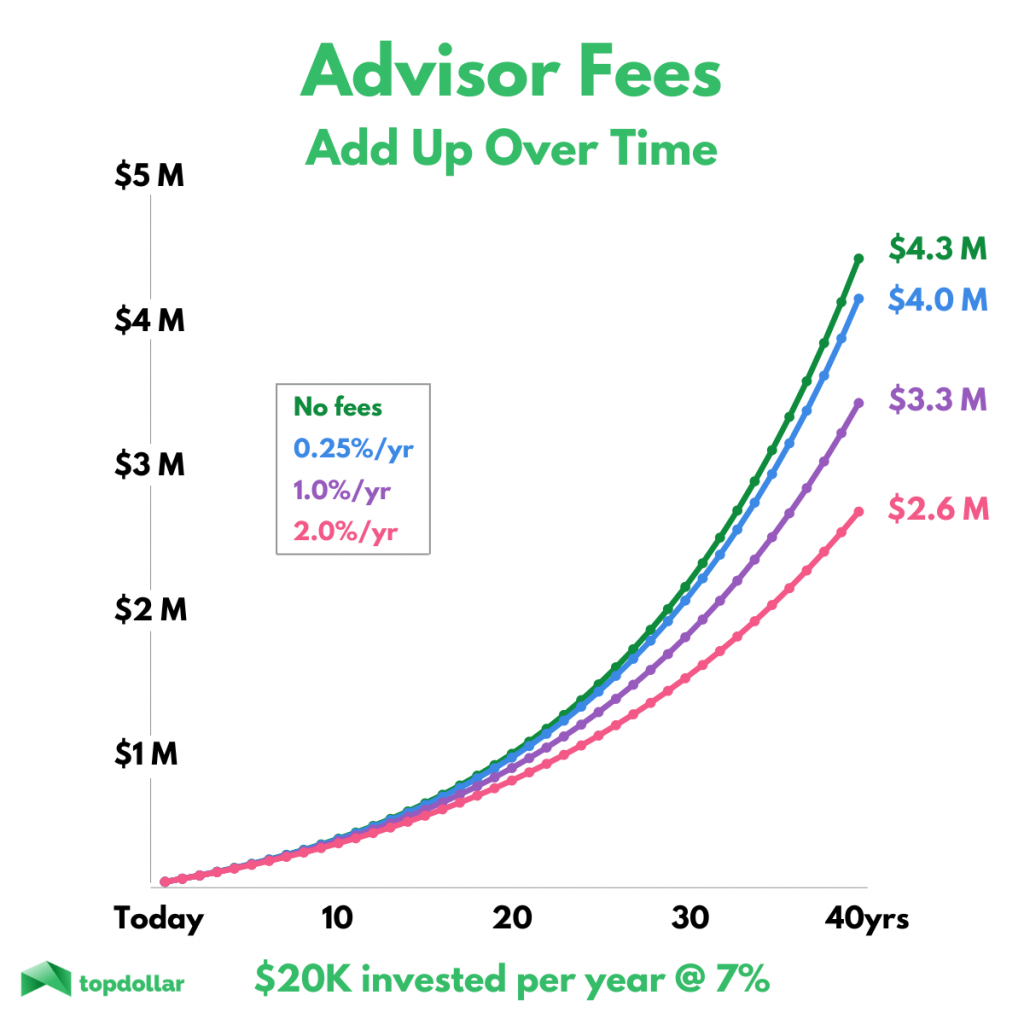

I am a proponent of do-it-yourself financial planning if you believe you can manage it. Why? Because it will save you a fortune over a lifetime. Most planners charge a fixed percentage of your total assets. Rates can range from 0.25% – 2.0% depending on the extent of the personalized service they provide (or how well you can negotiate). Let’s take a look at how much these fees can cost you over a 40-year investment horizon.

So, is it worth hiring a pro? Ultimately, you pay a lot over a lifetime for financial advisory services. Obviously, the lower the fees, the less drag you will have. If you do choose to hire an advisor, I would always recommend that you choose a trustworthy fiduciary with a low expense rate.

Personally, I chose years ago to commit my time and resources to learn how to manage my own finances. My primary objective when starting topdollar was to provide this foundational knowledge to everyone for free. Throughout this site, you can learn all the basics of managing your finances and reaching your financial independence and retirement goals.

Will Advisors Overperform Your Returns?

Will a professional advisor do better than you do yourself? Here’s the truth. If you are looking for hot stock tips or improved market returns, an advisor will likely not be worth the expense.

According to S&P Dow Jones Indices research, 90.03% of active managers benchmarked to the S&P 500 underperformed over the past ten years. No advisor will consistently provide better returns than you would yourself by investing in a no-fee passive index portfolio strategy. Even if you found an incredible advisor/active manager, they would have to overperform their fee every year (net of taxes!) in order to justify their expense.

Financial advisors can make sense if their fees are low enough to justify their guidance for sophisticated investment and tax-saving strategies. Additionally, many people are happy to pay for the comfort of taking the guesswork out of the process, especially if it seems overwhelming or time-consuming to manage. When you interview a financial advisor, you should make sure you are clear on how they will be adding specific value beyond your own knowledge to determine if the proposition is worth the cost.

The Best Value Option: The Roboadvisor

Robo-advisors have become increasingly popular over recent years. I have come to realize that for many investors, they offer significant added value through features such as portfolio rebalancing, tax loss harvesting, and professional guidance to recommend them as smart options if you are not prepared to do it all yourself.

If you find yourself struggling to have the right temperament or time to stick to your investment plan during a stressful market crash, a robo advisor will make the correct (but challenging) decisions on your behalf.

Most people use financial advisors because they offer confidence (using a professional money manager) and time savings. If you fall into this camp and are not looking to set up complex trusts or estate planning tools, then the robo-advisors offer the best value for the least cost.

Summary

Investment plans are essential for determining your individual progress and setting a strategy for achieving your financial independence. The plan should be reviewed annually to determine if you are on track, and if not, where you need to improve.

Depending on your current knowledge or your desire to learn, you have three general options:

Everyone should absolutely have an investment plan regardless of which option you choose.

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.