My Portfolio: Asset Allocation Model

Professional wealth managers strategically allocate investments across multiple assets. Stocks, bonds, and cash are the primary assets in portfolios, but savvy investors and professionals also use additional categories to further diversify and create rebalancing opportunities.

Check out my model portfolio below. Each asset class can be viewed in more detail to see which specific holdings I choose and why. I also provide a groundwork for maximizing returns, setting targets, assessing risk, and minimizing taxes.

Stocks

Stocks will always make up most of my portfolio because equity investments have proven to be the highest-performing asset class throughout modern history. I have a medium-high risk tolerance and only invest money in stocks that I will be able to leave in the market for 5+ years minimum.

Low-cost index ETFs are the best option for most investors to get broad, diverse stock market exposure. I only add company-specific stocks to get slightly over-weighed in names I strongly believe in.

Investing in passive index stock ETFs removes the need to rebalance your stock winners against losers, ultimately resulting in fewer taxes and more tax-deferred growth. Also, very few professional investors have outperformed benchmark index funds over the long run, further supporting a passive index strategy.

You may have noted that I hold QQQ despite this ETF not necessarily being the cheapest option. This position is due to significant unrealized capital gains in what was once a cheap ETF. Newer, cheaper ETFs seem to be continuously emerging, so when possible, I try to roll the ETF into better options using tax loss harvesting and tax-efficient portfolio rebalancing techniques.

![]() Top Dollar Edge: Check out my unbiased list of Best ETFs to make sure you are choosing the cheapest, best options when adding an ETF to your portfolio.

Top Dollar Edge: Check out my unbiased list of Best ETFs to make sure you are choosing the cheapest, best options when adding an ETF to your portfolio.

I like a mix of growth and value stocks but do not set portfolio targets for these subcategories. Why? Because I think both categories have merit but not significant enough diversification benefits to require mandatory thresholds. Plus, I am getting a reasonably balanced exposure by investing heavily in an S&P 500 index fund, VOO.

However, I do set target allocations for international stock exposure- currently set at 7%. See my rationale for setting international stock exposures in more detail.

Bonds

Based on my marginal income tax rate, investing in triple-tax-exempt municipal bonds offers a tax-equivalent yield greater than other comparable bonds. Unfortunately, there are no excellent muni ETFs for my state and local tax region, so I have to buy individual bonds.

Muni bonds are hard to purchase through an online-only brokerage account. So, if you want exposure to this asset class, a financial advisor or full-service brokerage company is usually your best method to facilitate the buying of individual bonds.

I focus on investment grade (high credit rated) muni bonds within my state and local tax regions. Buying issues within your municipality is imperative when investing in municipal bonds to achieve full tax benefits.

To round out my bond exposure, I use SCHR (Schwab Government Bond ETF) and VCIT (Vanguard Corporate Bond ETF) for more accessible liquidity to maintain my target percentages and rebalance my portfolio.

![]() Top Dollar Edge: Looking for a specific bond exposure through ETFs? Check out my list of Best Bond ETFs.

Top Dollar Edge: Looking for a specific bond exposure through ETFs? Check out my list of Best Bond ETFs.

Commodities

I use commodities for diversification as well as a hedge against inflation. Generally, I use gold and an ETF that invests in gold miners- GDX. Investing in commodity producers (like gold miners or oil producers) provides a very high correlation to a specific commodity while still investing in established companies.

Non-professionals often do not use commodities as commonly as stocks and bonds, as they tend to have infrequent periods of popularity followed by busts. However, recent periods of high inflation have led to a general boom and reinterest among investors in these assets.

Nevertheless, I preach caution, especially now with many raw commodities trading at elevated historical prices. If you feel it makes sense within your investment plan to have a small commodity allocation, practice sound rebalancing techniques by trimming or adding positions within your target thresholds.

Check out my top recommendations for Best Commodity ETFs.

Real Estate

First, let’s be clear: real estate investing does not include your primary residence. Unless you plan to downsize soon, you can’t usually realize a return on your home.

After owning and managing my own rental properties, I recently decided to realize a capital gain and reallocate my capital into equities during 2022. Time will tell if this will be a good move. My portfolio had become too heavily invested in an asset that had been overperforming, so a rebalance of sorts seemed logical.

In this same method, I recommend reviewing your investment plan annually and deciding if you want to make any fundamental changes to your targets and objectives.

Currently, I am invested in a property in the manufactured housing sector and maintain the rest of my exposure with SCHH REITs. Although investing in REITs is very different from owning physical properties, I view it as an easy, liquid option to temporarily hold my exposure to the real estate sector.

Interest in REIT investing? Check out my analysis for Best REIT ETFs.

Cryptocurrency

Should crypto be in your portfolio? Is bitcoin just one big Ponzi scheme? These are excellent questions, and to be honest, I don’t have the answer (anyone who makes confident declarations about crypto should be viewed with skepticism, in my opinion).

I do believe though, that with every moment bitcoin exists (without crashing to zero) it gains more legitimacy as a digital store of value.

Personally, I choose to keep a small allocation in crypto, about 75% in Bitcoin and 25% in Etherium. I won’t lose my mind if it all goes to zero, and I make sure to rebalance it regularly as it swings up and down.

Startups (Early Investing / Venture Capital)

Although usually lumped in with ‘alternative investments,’ I believe startup investing should be separate, as it has a very different risk vs. reward profile than most other alternative assets.

Investing in startups involves huge risks but also has enormous upside potential. Most investments become flops, and accurate valuations are often a bit more than a guess. It’s not quite like ‘Shark Tank,’ where an investor makes a killer deal (whereas Sharks seem to buy companies for pennies on the dollar).

Startup investing focuses on significant growth potential, but the business fundamentals are often murky as hell. Nevertheless, nowadays, there are ways for everyday investors to get access to Kickstarter movements or private investments through friends and family. There is an insatiable appetite for capital investment in new ventures, even for individuals on a smaller scale. Finding suitable investments may require effort, research, and persistent networking, but you can often connect to entrepreneurs directly and determine if some opportunities seem comfortable for you.

I currently invest a small allocation through a small VC fund (in several different ventures).

Cash

“Cash is king,” some people say. I don’t say that, but rather believe holding too much cash on the sidelines is a common mistake many investors sadly make. You should have cash in an emergency fund and up to 3 months’ worth of expenses in a checking/savings account, but other than that, I don’t recommend leaving too much money in cash (including cash equivalents) for the long term.

If you are preparing for a major upcoming purchase (such as a new house or large payment), by all means, you could move the needed cash aside, but in the long run, cash doesn’t offer significant enough returns to warrant hoarding it.

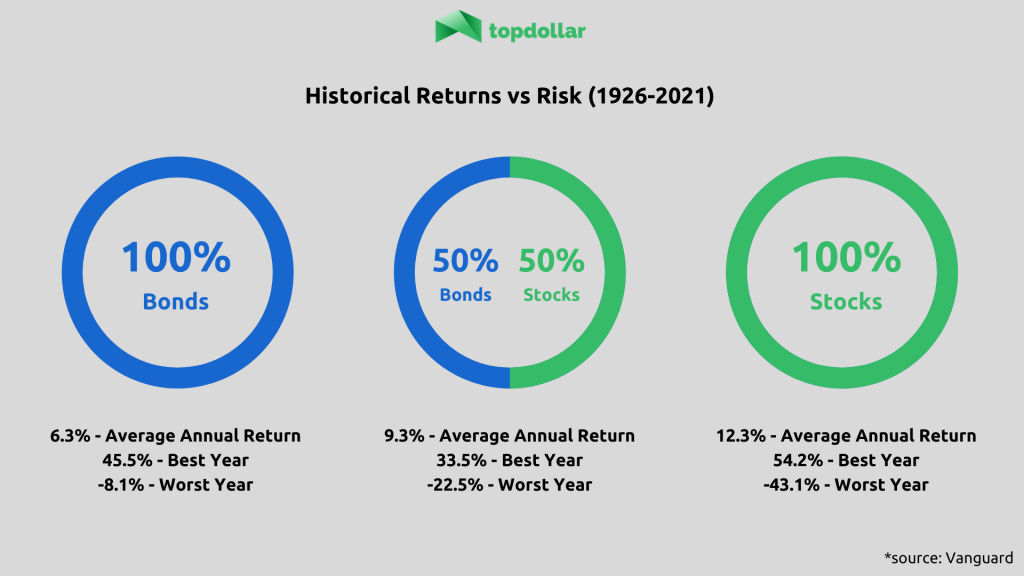

Even while entering a new era of higher interest rates for the first time in a generation, investing in bonds will often produce better returns (at about 6.3% over the past century).

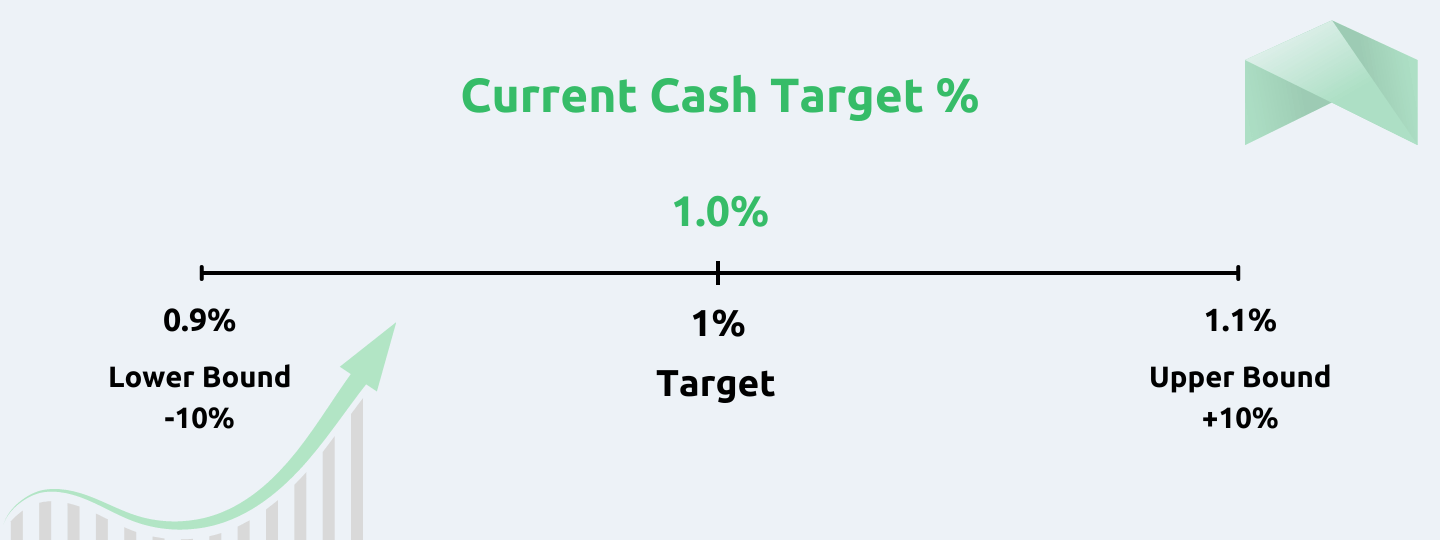

I recommend staying disciplined with cash, and do not let too much accumulate in your accounts. I regularly reinvest cash once it gets above my maximum threshold, as set forth in my investment plan.

In fact, I use new cash to rebalance my portfolio (tax efficiently) at regular intervals. This technique is a slightly more intelligent form of dollar cost averaging, as it allows me to consider where I reallocate my new money. The key is once I hit my maximum cash allocation threshold, I force myself to invest the cash into another asset class- usually into my most underweighted category.

Alternative Assets

Currently, I don’t have a target for any alternative assets holdings in my portfolio.

Why no alternatives? Alternatives can provide excellent returns, but they do require specific expertise and research in order to be successful.

Alternatives offer the benefit of increased diversification and often have returns that are least correlated to traditional assets (which is excellent!). Physical products, such as collectibles, are often seen as a hedge against inflation in the same manner as gold or real estate.

However, these assets are often very illiquid, difficult to value, and don’t have a centralized marketplace- making it very difficult to buy and sell investments for most individuals.

What Are Alternative Investments?

Alternative investments include:

Pros

Cons

Learn More About Alternative Assets

Have any questions or comments? Feel free to contact me.

Disclosure:

Consider your own unique risk tolerance and investment goals before making any investment decisions. Perform your own research and make educated investment decisions based on how they relate to your personal situation. Consult a licensed financial or tax advisor should you need professional advice.

The author (Josh Dudick) currently has positions in the companies and ETFs listed and may purchase or sell shares within the next weeks or months. This article should not be viewed as a solicitation to purchase shares in any security and is provided for informational purposes. Investors should consult a financial advisor or exercise their own due diligence before making any investment decision.

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.