Step-By-Step Method to Make an Investment Plan Yourself

Financial advisors charge significant fees, which ironically may cause more harm than help in reaching your financial goals. Due to costs, I always recommend a do-it-yourself approach if you are serious about achieving financial independence.

Managing your own financial planning may sound a bit intimidating, but I promise to support you with the information and tools necessary to pull it off. It’s not that complicated if you are organized and understand all investment options and accounts available to use.

If you are looking for a step-by-step guide, you have come to the right place. I will take you through the framework used by most financial advisors, discuss proper investment allocations, and review tax-optimized savings accounts. The foundation here will help you build wealth and financial freedom for the long term (so I apologize that it’s a bit lengthy).

Let’s jump in and build your investment plan the right way, step by step.

Step #1: Your Net Worth Today

Before charting your specific investment plan, you first need to understand your current financial situation clearly.

Do you know your net worth? If not, your first step is to calculate this number. Everyone has a net worth (even if it’s negative), and it’s critical to understand where you currently stand.

Assets include everything you own. Common assets may include:

- Cash in checking and savings accounts.

- CDs or government savings bonds.

- Total value in all investment accounts (retirement accounts, education savings plans, and regular brokerage accounts).

- Home equity, investment properties, and any land you may own.

- Cryptocurrency

- Cars, Boats, Motorcycles, Jetpacks, and Spaceships (still awake?)

- Significant collectibles or other assets of value

Your liabilities include all the debt you may have accumulated:

- Student loans

- Credit card debt

- Car loans

- Mortgages and home equity loans

- Loans financed against expensive purchases (cell phone, tv, computer, etc.)

- Medical debts

- Personal loans

- Payday loans

- Unpaid bills

After calculating your net worth, you should understand how your assets are allocated.

Here are some situations that may suggest your personal finances are not ideal:

- A negative net worth without enough foreseeable income in the future to pay off your debts and build positive wealth.

- Having more than 40% of your net worth in your primary residence is generally too much, it reduces your ability to invest in higher-returning assets.

- Having a significant portion of your net worth in not-returning assets, such as in cash or in a car.

If you do find yourself with an asset allocation issue, don’t panic. Identifying weaknesses is part of the goal. Your recourse is to address the issues going forward- in your financial plan.

Step #2: Where Are You In Life?

Now you want to consider where you are in life and what goals you hope to achieve personally, professionally, and financially. The more detailed you can be, the more productive your plan will be. Don’t worry if you are unsure or change your mind in the future. You can (and should) reflect and update your plans at least annually as life and goals inevitably evolve.

Personal Plans

- What are your plans and vision for the next few years?

- Do you currently have or envision getting married?

- Do you have or want children, and if so, how many?

- How do you want to be spending your life?

- Do you know where you want to live in the future?

- Do you have any dreams or goals you want to work towards achieving?

- Do you have any significant expenses coming up in the next 3 years?

Professional Plans

- Where are you in your career, or what are your future work aspirations?

- Are you considering going back to school or considering shifting careers?

- Are you satisfied with your work/life balance? Are you planning on working more or less?

- Do you see yourself on a path you are content with? If not, are you considering career changes?

Financial Plans

- How much do you currently make per year? How do you see your income changing over the next 3, 5, or 7 years on your current path?

- You should know your marginal tax rate, and how much you take home net of taxes.

- Do you have a budget?

- How much are you putting into tax-advantaged retirement accounts?

- If you already have children, do you plan to save for educational costs? Have you started college savings plans?

- How much extra are you currently saving in regular brokerage or savings accounts?

This basic framework should form the foundation of what expenditures you need to plan for. Money compounds quicker with more time, so the sooner you can start saving for milestones, the easier it will be to grow your money to your desired targets.

Step #3: Determine Your Money Goals

Your next task is transcribing your vision and goals into actual expenses and estimated timeframes. I recommend using a spreadsheet (I use excel) to organize yourself by year. The goal is to be as specific as possible, such as: “I want to have $100,000 for a down payment by 2028.”

Common goals may include the following:

- Homeownership (Down payments)

- Education savings

- Wedding costs

- Vacations (You need to enjoy life)

- Second property

- Retirement savings

The Rule of 4%

When it comes to setting a retirement target, people often have no idea how much they will need.

Generally, the rule of 4% is used by advisors to determine how much total savings you need for retirement. The rule states you can use 4% of the total amount you have saved for retirement per year, and that adjusts for inflation.

For example, if you saved $1 million, the rule says you can withdraw $40,000 in your first year of retirement. In subsequent years you can withdraw $40,000 + an extra amount to account for yearly inflation. This should last you about 30 years of retirement.

Other sources of Income

Of course, you may have other income sources at retirement, such as passive income from dividends or real estate. Social security (in some form) is also a reasonable assumption, assuming you have been paying into the program during your working years.

These other sources of income will allow you an increased buffer or increase your spending budget over the 4% rule.

Step #4: Understand How Your Savings Will Grow

Each specific plan will ultimately require a specific saving plan on how you will get there. Let’s review some simple math- here is how you can calculate your future value, given your starting value, rate of return, and time.

Returns can never be guaranteed, but you should have a reasonable estimate of what various investments should likely return. I recommend using conservative numbers- 6.5% for stocks, 4% for bonds, and 0% interest for cash. These returns will all be reduced further by taxes.

Step #5: Understand Your Taxes

Taxes must be paid on any earnings from interest, dividends, or capital appreciation. Taxes can be complicated, and you should speak with a tax expert if you have complex or unusual tax circumstances. Let’s review the most important tax considerations.

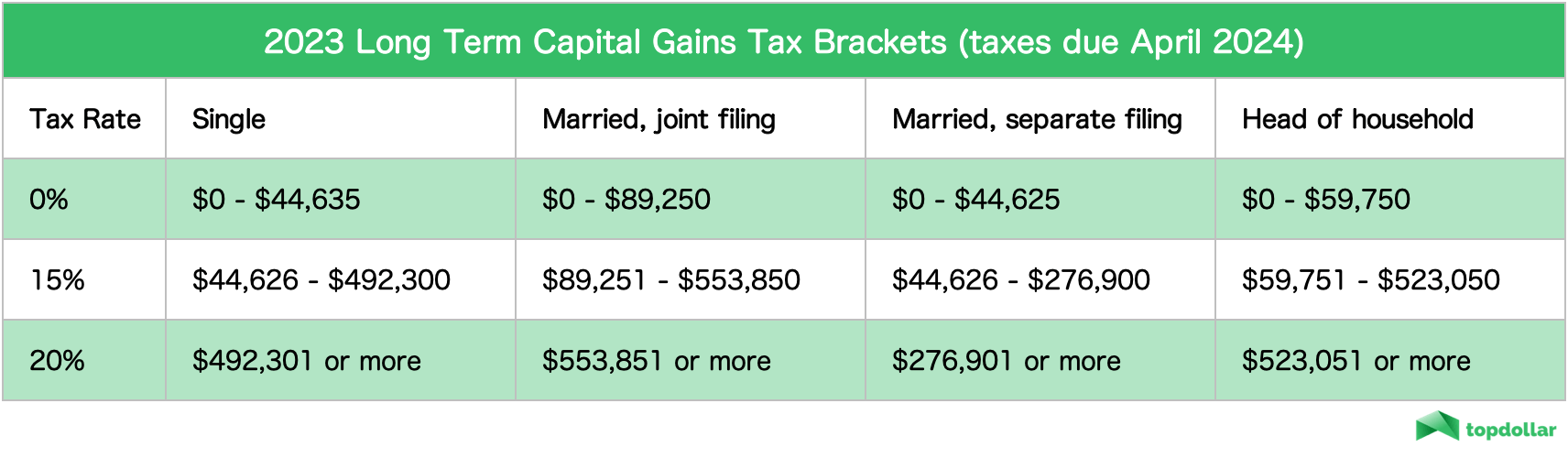

Long Term Capital Gains + Dividends

Long-term capital gain includes investments held longer than one year. Although there are rare exceptions, most LTCG and Dividends are taxed at more favorable rates than ordinary income tax rates.

Short-term capital gains get taxed at higher rates, so it is wise to keep investments in the market for at least a year or longer, assuming you don’t need the money immediately.

Not only do tax rates decrease after one year, but taxes are only paid once gains are realized. When saving in a taxable account, it is not advisable to switch investments often.

Buying and selling between various stocks will trigger taxes and significantly reduce the effect of tax-deferred compounded growth. Using tax-efficient passive index funds, you can achieve your target investment allocations and diversification goals without unnecessarily realizing capital gains.

Short Term Capital Gains + Interest

Investments held for less than one year and interest-rate products (bonds, CDs, savings account interest) are taxed at ordinary income rates. Interest and bond coupons are taxed every year, thereby removing any opportunity for tax-deferred growth. Nevertheless, interest-rate products do have less risk than stocks, and the balance between these allocations should come down to both expected returns as well as individual risk tolerance.

When calculating your savings needs, it is imperative that you remove the taxes from the estimated returns. State and local taxes need to be included and are usually treated the same for all earnings- short and long-term.

When calculating your returns, follow these rules:

- Short-term capital gains, interest, and wages are taxed at ordinary income rates and are due every year. Therefore, they need to be deducted annually from your gross returns.

- Long-term capital gain can be deferred until the end of the investment period, assuming you don’t sell or reallocate the earnings.

- Dividend taxes will be paid due every year, but account for them at the long-term rate.

For example, if your marginal tax rate is 40% (federal and state) and your long-term capital gains rate is 20%, your estimated returns assuming a 6% return would be:

- Short-term gains and interest: 6% x (1 – 40%) = 3.6% annually

- Long-term gains: 6% annually, with 20% removed only at the end of the investment period.

- Dividends: 6% x (1 – 20%) = 4.8% annually

Step #6: Building A Portfolio

Asset Allocation

Building your plan requires at least a basic understanding of the differences between assets risk vs. return. If these terms are unfamiliar to you, I recommend starting here.

Don’t get caught up on picking specific stocks; rather, the focus is to allocate to specific asset classes- such as stocks, bonds, cash, or real estate. I always recommend investors use diversified passive index ETFs or low-cost mutual funds to get diversified exposure, especially if you are not planning to spend time learning to research and value individual companies.

Returns can never be guaranteed, but you need to estimate what different assets will likely return. As mentioned previously, I recommend using 6.5% for stocks, 4% for bonds, and 0% interest for cash.

Calculate Out Various Allocation Models

You should use the future value formulas explained above to determine how much savings and time you need to achieve your goals. Consider how much risk you are willing to take as you examine asset allocation options. You should not take on more risk than you are comfortable with to try to gain higher returns. Never feel pressure to invest with excess risk, as this will often lead to poor decisions and less flexibility in the event of a stock market crash.

You should always be prepared with a ‘Plan B’- whether that means postponing your retirement or purchases, going with a cheaper option, or adjusting your budget.

Conduct an annual review of your investment plan. Be sure to monitor your progress to avoid unpleasant surprises and have the opportunity to make necessary adjustments.

Risk Tolerance and Stock Market Volatility

As you get closer to your investment horizons, stock market volatility gets more dangerous. Therefore, take less risk as you approach your planned milestones.

Using passive index funds, mutual funds, or ETFs will not help against a broad market crash, but they will help to minimize individual company risk.

Model the returns of several different allocations between stock, bonds, and cash, and more knowledgeable investors may consider commodities, real estate, or alternative investments. Diversification is key, and spreading risk across various asset classes is the best practice for reducing overall portfolio risk.

Step #6.5: Sample Asset Allocations

Don’t know where to start with your allocations? Consider some popular sample portfolios.

3 Fund Portfolio

The 3 fund portfolio is the classic foundation for most portfolios. It includes allocations in the U.S. stock market, the U.S. bond market, and a smaller allocation in international stocks.

Example:

- 65% VTI (Vanguard) U.S. Broad Market Stocks

- 20% SCHR (Schwab) U.S. Government Bonds

- 15% IXUS (iShares) International Stocks

I don’t recommend going over 15% in international stocks. The amount you wish to allocate to bonds over stocks depends entirely on your risk tolerance and investment preferences. A 3-fund portfolio is logical and can be accomplished with just three ETFs. I recommend using low-cost ETFs. You can review the cheapest ETFs here.

Variation Guidance

Do you want other assets besides just three funds? No problem. Feel free to add 5-10% of another stock ETF against your total stock holdings or a bond ETF from your total bond holdings. If you are considering adding alternative assets (such as REITs or commodities), I urge you not to add more than 5% allocation in any alternative asset class unless you fully understand the investments and expected returns.

Example #2: If you want more dividend stocks, and a bit less overall risk.

- 30% VTI (Vanguard) U.S. Broad Market Stocks

- 20% SCHD (Schwab) U.S. High Dividend Stocks

- 40% SCHR (Schwab) U.S. Government Bonds

- 10% IXUS (iShares) International Stocks

Example #3: If you want some corporate bonds in addition to U.S. government bonds, and more large-cap growth stocks.

- 35% VTI (Vanguard) U.S. Broad Market Stocks

- 20% SPYG (SPDR) U.S. Large Cap Growth Stocks

- 20% SCHR (Schwab) U.S. Government Bonds

- 15% VCIT (Vanguard) U.S. Corporate Investment Grade Bonds

- 10% IXUS (iShares) International Stocks

Example #4: You want some exposure to real estate using REITs.

- 60% VTI (Vanguard) U.S. Broad Market Stocks

- 20% SCHR (Schwab) U.S. Government Bonds

- 15% IXUS (iShares) International Stocks

- 5% SCHH (Schwab) U.S. Real Estate

Example #5: You want significantly less risk (more bond exposure).

- 35% VOO (Vanguard) U.S. Broad Market Stocks

- 25% SCHR (Schwab) U.S. Government Bonds

- 20% VCIT (Vanguard) U.S. Corporate Investment Grade Bonds

- 10% SCHP (Schwab) U.S. Inflation-Protected TIPS Bonds

- 5% IDEV (iShares) International Developed Market Stocks

- 5% SCHH (Schwab) U.S. Real Estate

As you can see, the variations are endless. Don’t get overwhelmed about making the perfect portfolio, there is no such thing. Choose your asset allocations and then let time and compounding returns do the rest of the work.

![]() Top Dollar Edge: I update my real investment portfolio here. Keep in mind I have a high-risk tolerance, and my high allocation of stocks is not necessarily appropriate for other investors.

Top Dollar Edge: I update my real investment portfolio here. Keep in mind I have a high-risk tolerance, and my high allocation of stocks is not necessarily appropriate for other investors.

Minimize Taxable Events

Consider taxable gains before making tweaks to your portfolio. Deciding to decrease risk over time makes sense as you get closer to needing your money. Changing within an asset class (such as moving from European stocks to Emerging market stocks) will not make profound differences in the long run, so I would not do so if the taxable impact is significant.

It’s ok to make adjustments if there will not be significant taxable gains. Always consider if the move is logical, including the tax implications. Remember, realizing taxable gains prematurely can significantly hinder the tax-deferred growth of a portfolio. This is why passive index ETFs are such an effective set-it-and-forget-it tool.

Summary: Building Your Own Portfolio

- Consider the total stock holdings vs. the total bond holdings and ensure they fit your risk tolerance.

- Don’t invest too big in alternative assets unless you are an experienced investor and understand the risks thoroughly.

- Stay the course, and do not overtrade your holdings.

Step #7: Use Tax-Efficient Accounts Whenever Possible

It is imperative that you use tax-advantaged accounts when possible to reduce tax drag and allow your money to grow as efficiently as possible. The best tax savings opportunities come from retirement accounts and education savings accounts.

Retirement Accounts

Retirement accounts come in two main varieties- Traditional plans and Roth plans.

Traditional plans allow you to take a tax deduction against your income on any contributions you make to the accounts (within the maximum limit). When you take the money out at retirement, you will have to pay tax at your ordinary income tax rate in the future.

Roth plans do not allow you to take an immediate tax deduction. Your contributions are made with post-tax dollars. However, Roth plans allow tax-deferred growth and no future taxes on any money or earnings (assuming you stay invested until retirement).

If your company offers a 401(k), I recommend maximizing this account first. Secondarily, if you are already maxing out your 401(k) plan, you can contribute to a backdoor Roth, regardless of your income level.

If you want more information the best retirement plans or don’t have a company-sponsored plan offered, I recommend these articles:

Educations savings

529 education savings plans provide an excellent tax advantage and work similarly to a Roth IRA. Additionally, many 529 accounts offer state tax deductions, tax-deferred growth, and tax-free withdrawals on qualified education expenses.

If you are planning on saving for a child (or yourself, spouse, grandchild, etc.), a 529 plan is an intelligent tax-saving tool. However, qualified withdrawals do have to be related to educational expenses, or the earnings will incur taxes and a 10% penalty. Therefore you don’t want to over-contribute to these plans more than you plan to spend on education.

There is some flexibility if you have extra funds left over, and you can learn more details about education savings plans in this article.

Step #8: Review Annually and Make Adjustments

Congratulations, you completed your investment plan! But wait, you’re not quite done. Every year you should plan to conduct an annual review of your entire financial plan.

- First, review your accounts and update your savings and net worth calculations.

- Consider how financial or life goals may have changed since your last update and determine what changes need to be made (if any) to your goals and plan.

- Recalculate your expected investment returns, given your current balances. Reconsider if you need to make any changes to your investment allocations or risk views. Aim to be objective and not emotionally based on how markets have performed. For example, it is sensible to reduce risk if you can achieve your targets with less risk. It is not advised to reduce risk just because the market is in a downturn.

- Every year repeat this process and make any necessary changes to ensure you are on track to achieving your goals.

Remember, if you are not on track, your options are:

- Set a stricter budget so you can save more

- Adjusting your asset allocations may make sense depending on your time horizon and risk appetite.

- Lower your investment goals or establish an acceptable backup plan in case of reduced returns.

- Work harder, start a side hustle, plan to work longer, or look for higher-paying jobs.

I check in on my portfolio and review my investment plan once per quarter, but once per year is my recommended minimum. If you are serious about reaching your financial goals and independence, one day building your own plan and following through on your targets, follow my recommendations and guidance.

Summary:

Setting and controlling your own financial plan can empower and help you achieve financial freedom. Remember these essential tips:

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.