2023 Tax Rates & Federal Income Tax Brackets

Every year the IRS releases updates and makes minor changes to the federal income tax brackets and tax rates to adjust for inflation. New rates have been published for the 2023 tax year. Additionally, you’ll find data for the 2022 tax rates, in case you have a tax extension or back taxes you need to file for the previous tax year.

Federal Income Tax Brackets

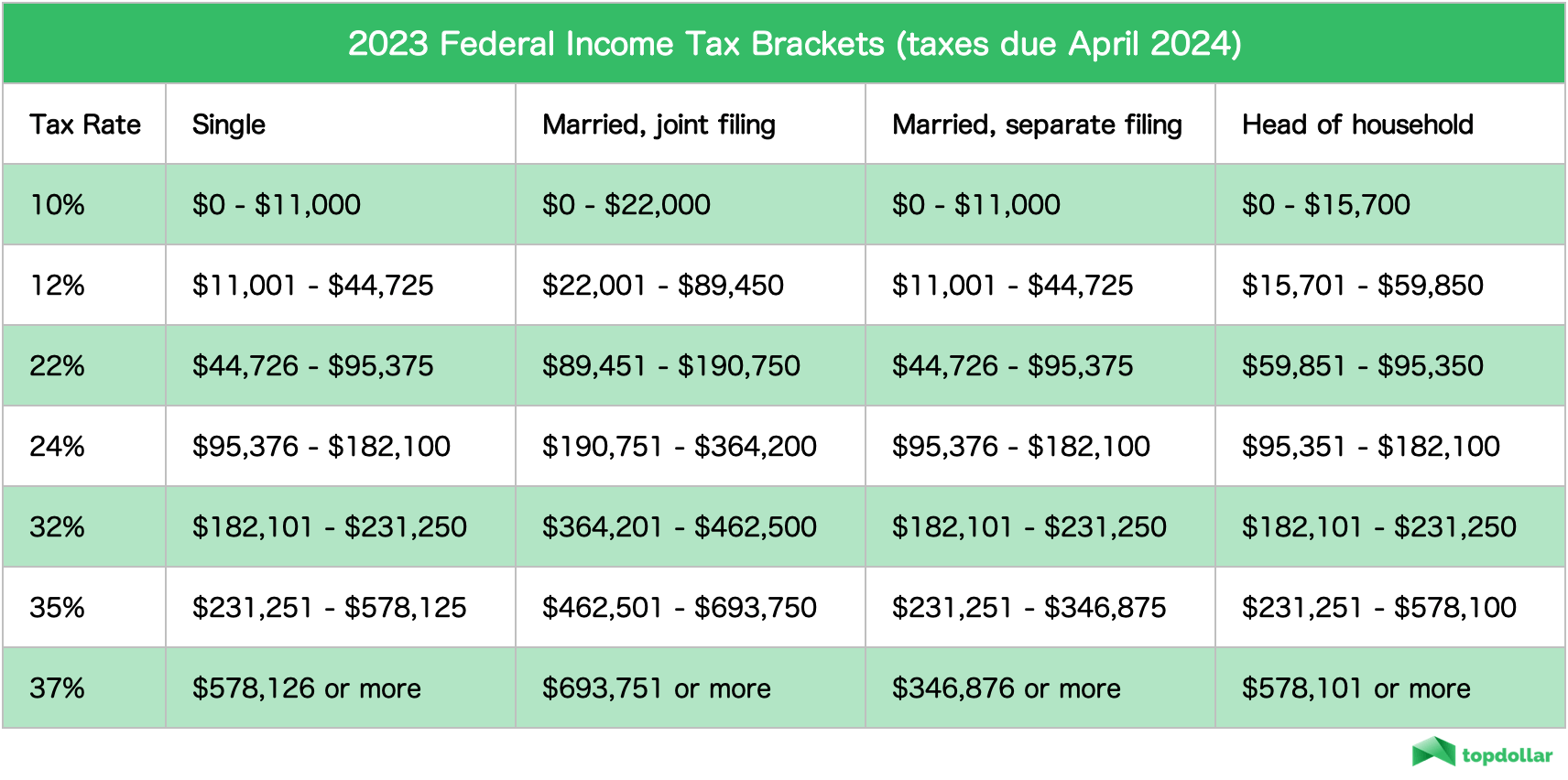

2023 Federal Income Tax Rates

For 2023 federal income tax, due in April 2024.

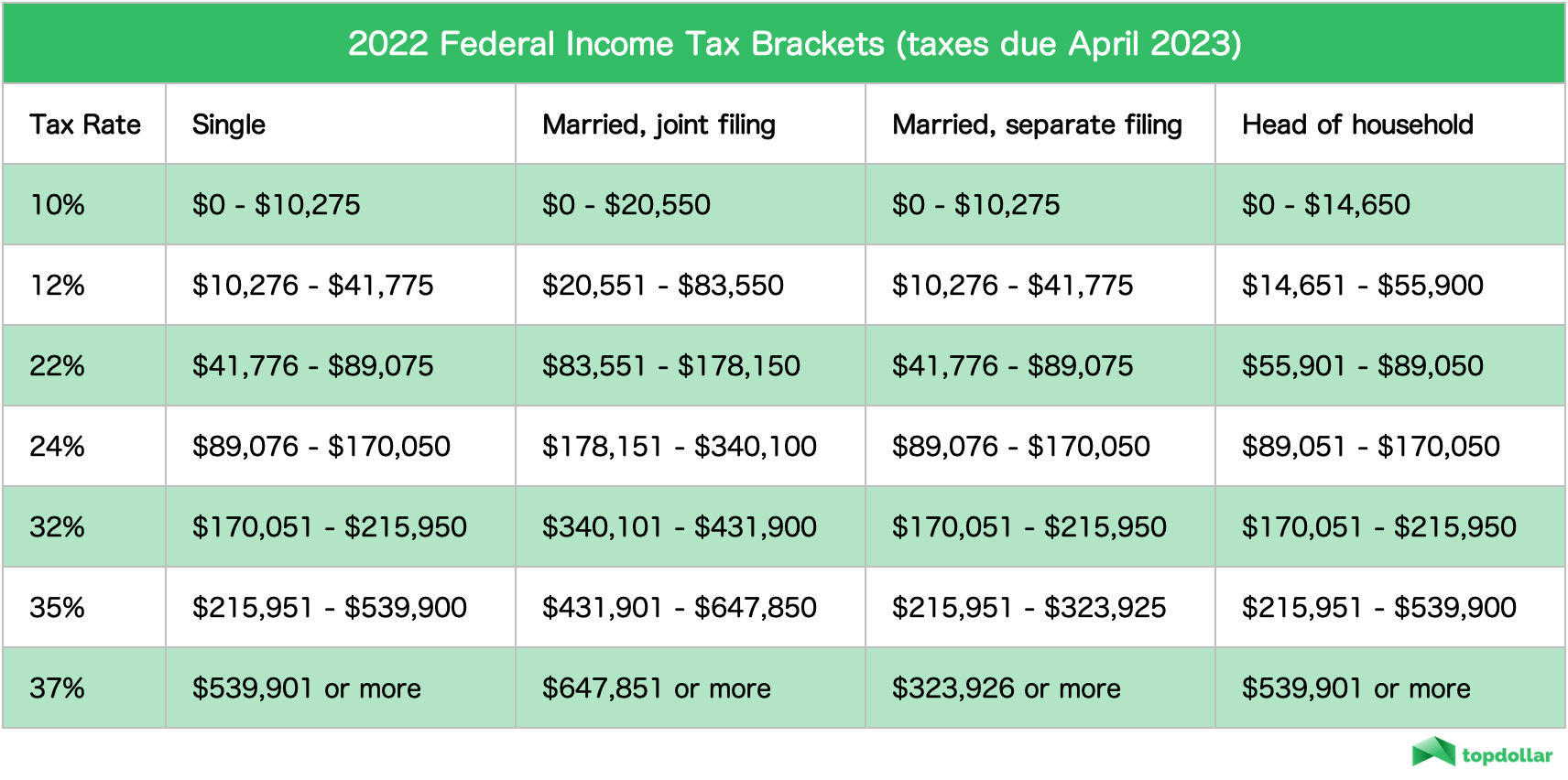

2022 Federal Income Tax Rates

For 2022 federal income tax, due in April 2023.

How Do Federal Income Taxes and Tax Brackets Work?

Ordinary income tax rates are applied to the following types of income you may receive throughout the year:

These forms of income are taxed in the United States under a progressive tax system. This means the more you earn, the higher your tax rate.

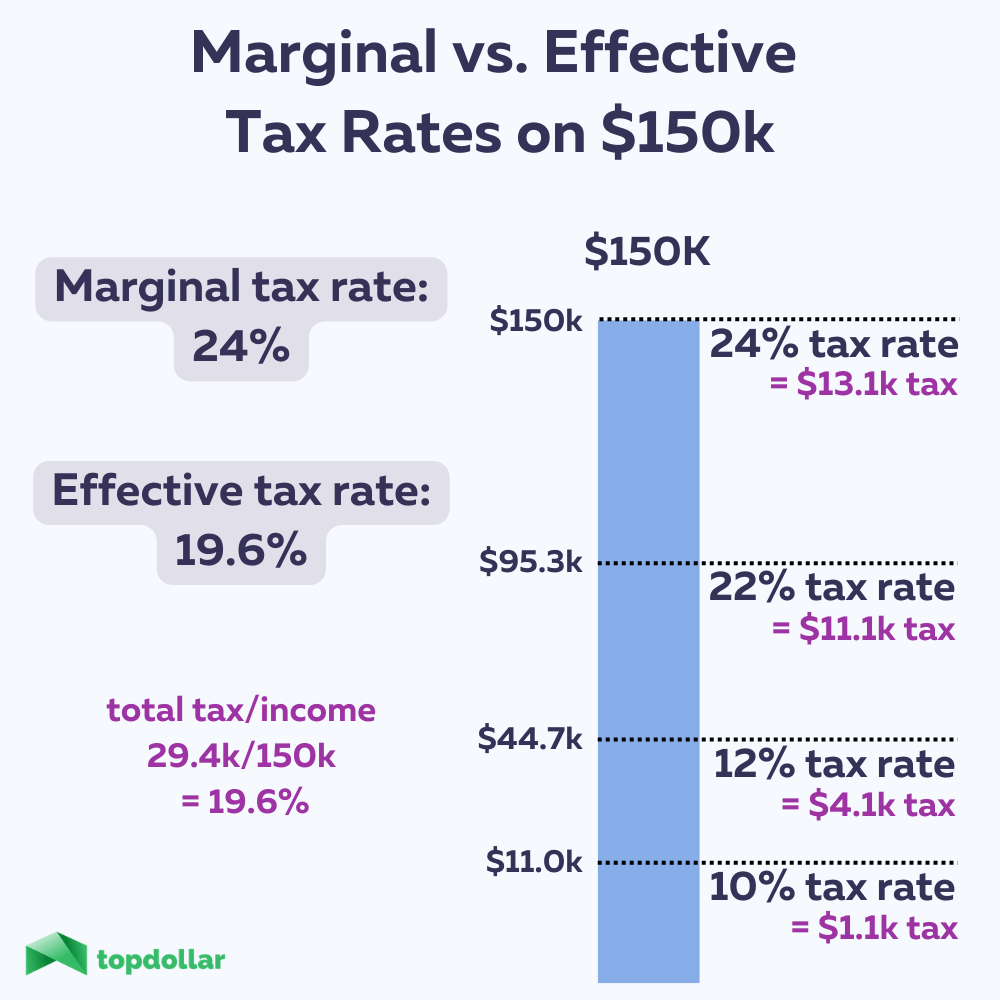

Marginal Tax Rates

Under a progressive tax system, your first dollar and your 50,000th dollar are taxed at different rates. The highest tax bracket you fall into is your marginal tax rate. “Marginal” refers to how much tax you pay on the next dollar you earn.

Marginal tax brackets are essential to understand for effective tax planning. Tax credits or deductions that lower your taxable income will reduce your taxes at the marginal tax rate. Therefore, when you consider various tax-advantaged strategies, deductions, or retirement plans, such as Traditional vs Roth plans, your potential tax savings and decisions should be based on your marginal tax rate.

Your marginal tax rate is your top rate, but your average tax rate will always be significantly lower.

Effective Tax Rates

Your effective tax rate is the average rate you pay over your entire income. The more you make, the greater your effective tax rate will be, as you will pay a larger percentage of your taxes at a higher marginal tax rate.

Effective tax rates are essential for financial planning because they tell you how much income goes to the government and how much is available for saving and spending needs.

State and Local Taxes

In addition to federal taxes, you must pay state and local taxes based on your jurisdiction’s tax rates. Some states have zero income tax, and some have rates that exceed 8% or more.

Payroll Taxes

Ordinary wages are also subject to payroll taxes which include social security, medicare, and unemployment taxes. Medicare and social security taxes are paid half by the employee and half by the employer.

Medicare Tax

Medicare tax is 2.9% on all your wages (of which you will be responsible for paying 1.45%).

Social Security Tax

Social security tax is 12.4% (6.2% is your portion), but the percentage is capped to the first $160,200 of wages (in 2023). Any wages you make above this threshold are not taxed additionally.

Additional Medicare Tax

An extra medicare tax of 0.9% is applied to all wages above $200,000 for individuals (or $250,000 married files jointly / or $150,000 married files separately). This tax began in 2013 under the Obama administration (sometimes referred to as Obamacare Tax).

Capital Gains Tax Rates

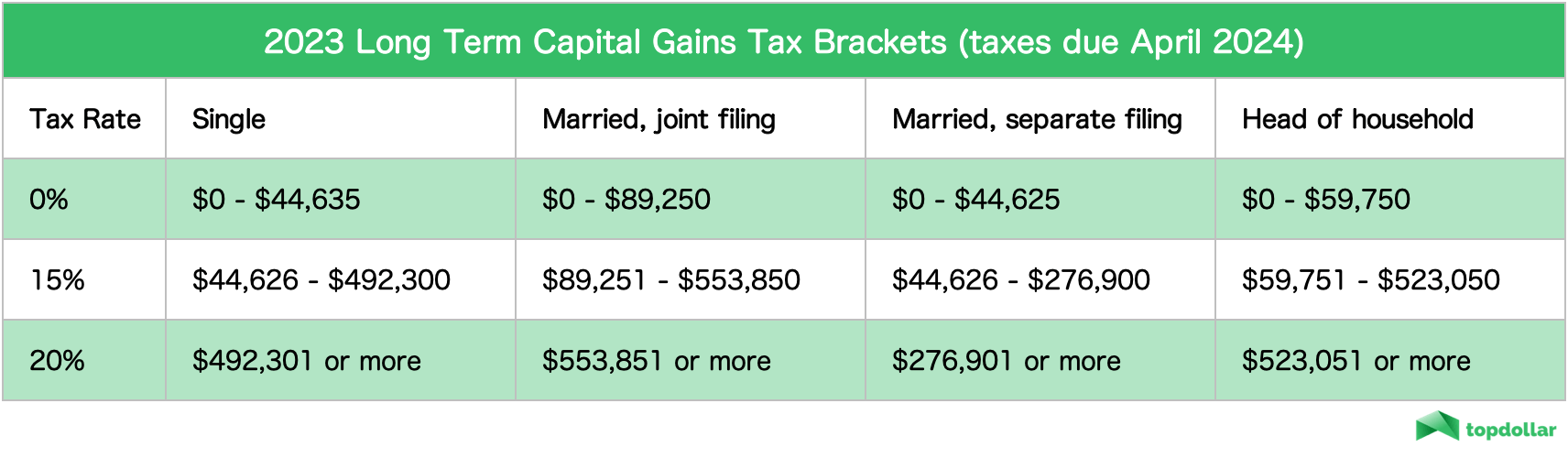

2023 Capital Gains Tax Brackets

For 2023 long-term capital gains and dividends, due in April 2024.

2022 Capital Gains Tax Brackets

For 2022 long-term capital gains and dividends, due in April 2024.

How Do Capital Gains Taxes Work?

Capital gains tax rates apply to profits on investments but are only due when positions are sold. The IRS categorizes capital gains as either short-term or long-term gains.

Long-Term Capital Gains Tax

Long-term capital gains tax is a tax on investments held for over one year. Long-term capital gains are the most favorable tax rates and are also applied to most types of stock dividends (called qualified dividends).

Short-Term Capital Gains Tax

Short-term capital gains tax is a tax on investments held for less than one year. Short-term capital gains rates are the same rates as ordinary income tax.

Irregular Capital Gains Taxes for Common Investments

Short Stock Positions

Short shock and short ETF positions are taxed as short-term gains. Even if the short position is held over one year, it is taxed as short-term capital gains.

Foreign Exchange Taxes (Forex Currency) and Futures Positions

Futures and forex are treated specially under section 1256 of the IRS code and are taxed at a hybrid rate of 60% long-term capital gains and 40% short-term capital gains, no matter how long they are held. These positions are considered “mark to market,” meaning taxes are due on the profit (or loss) at the end of trading on Dec 31 of the taxable year. Gains or losses are applied based on the final market price, regardless of whether the position is still open or closed.

Collectibles Taxes (Art, Antiques, Gold, Silver, Coins)

The IRS taxes collectibles at a maximum tax rate of 28%. However, this is only on physical collectibles, including precious metals. However, if you were to hold a gold ETF, you would be subject to long-term or short-term capital gains taxes depending on how long you hold the position. Similarly, you would be subject to the 60/40 rule for 1256 contracts if you purchased a gold future.

Cryptocurrency Taxes (Bitcoin, Etherium, NFTs, digital currencies)

The IRS taxes cryptocurrency in different ways depending on how it was acquired. If you mined the crypto, it’s treated as income and taxed on the value date it is produced. If you buy crypto and sell it (or spend it) the gain or loss is treated as property. Property is taxed according to regular capital gains rules, and long-term or short-term gains will apply depending on how long the position is held.

Real Estate (Investment Property) Income Taxes

Income from real estate investments is taxed at ordinary income rates. However, several deductions could reduce your investment property’s taxable income, including any maintenance, taxes, and insurance costs. In addition, a rental property can be depreciated over time, creating an accounting expense that can be deducted from your rental income.

Real Estate Sales Tax

If you buy or sell a physical property, real estate is traded as a capital investment. As such, it is taxed at a long-term or short-term capital gains rate depending on how long it is held.

If real estate was depreciated before the sale (for example, to reduce taxable rental income in prior years), the total depreciation would have to be recaptured and taxed.

If real estate is a primary residence, there is a capital gain exclusion for the first $250,000 for single owners (or $500,000 for married couples). So if you have a capital gain of $250,000 or less, you will owe zero capital gains tax on the sale of your primary home.

Additional Capital Gains Tax: Net Investment Income

Under the Obama administration, a tax of 3.8% was created, which is taxed on most types of passive investment income, such as capital gains, interest, dividends, and rental income. This tax is paid on investment income over $200,000 for individuals (or $250,000 married files jointly / $150,000 married files separately).

If you are below these caps, you will not owe net investment income. However, if your investment income pushes you over the threshold, you will only pay the 3.8% tax on any income over this threshold amount.

How Does Withholding Tax Work?

For most individuals who are employees, your company will withhold taxes from each installment of your paycheck. When you first begin employment, you fill out a W4 which gives the company guidance on how much tax should be withheld based on your tax status.

Nevertheless, employers may not perfectly withhold the exact amount owed as they cannot possibly take into account all of your specific circumstances, including tax deductions, tax credits, charitable contributions, etc.

How Does a Standard Deduction Work?

The IRS allows you to choose between itemizing your tax deductions or taking a standard deduction. It makes sense to itemize if your total qualifying deductions are above the standard amount. However, there are limits on most of the common deduction categories. Itemized deductions include:

State and local taxes are capped at $10,000. Home mortgage interest is capped on the first $750,000 of your mortgage loan (or $1,000,000 if the mortgage originated before Dec 16, 2017).

Medical and dental expenses can only be included if expenses are over 7.5% of your gross income. Student loan interest is capped at $2,500 per year.

Because of the limits on many of the items, most individuals benefit from taking the standard deduction option offered by the IRS. The standard deduction adjusts annually for inflation, and current amounts are listed below.

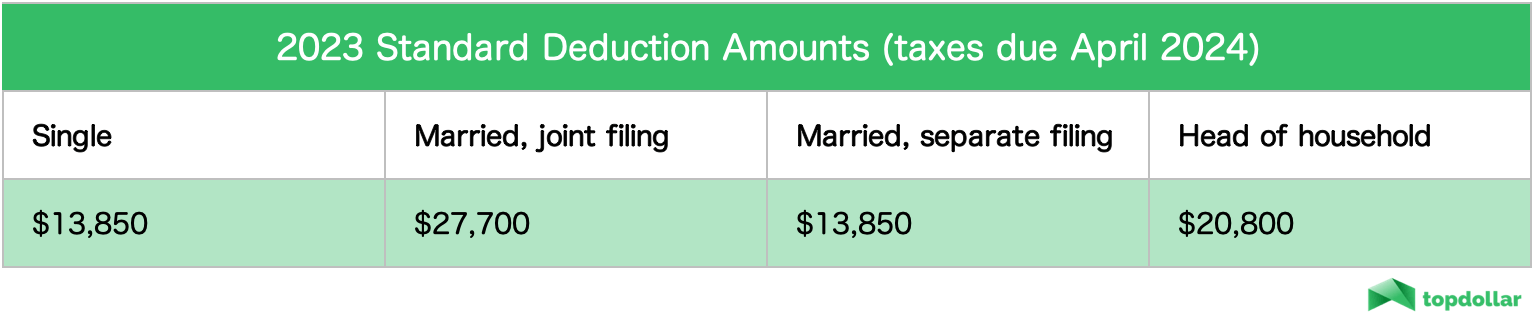

2023 Standard Deduction

For 2023 tax return, due in April 2024.

2022 Standard Deduction

For 2022 tax return, due in April 2023.

Will Future Tax Rates Go Up or Down in the Future?

The last time the government adjusted the tax brackets was in 2017 under the Tax Cuts and Jobs Act of 2017. The current rates are set to expire after 2025. With no new legislation, the top tax bracket will increase from 37% to 39.6%.

Of course, Congress can pass legislation at any time so trying to predict future tax rates is a political gamble. Generally, a Republican-controlled Congress will aim to lower rates or maintain the current tax cuts defined in 2017. However, a Democratic-controlled Congress would be more likely to raise tax rates sooner.

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.