What Is a Backdoor Roth IRA: Benefits and How to Convert

In many ways, the Roth IRA is one of the greatest retirement and estate planning tools in existence for individuals to grow wealth over their lifetime.

After realizing the tremendous opportunity this provided high-income earners, legislatures closed the front door for Roth IRA contributions by setting a low-income ceiling for eligibility. Curiously, they opened a legal and widely used backdoor method that allows higher income earners to contribute to a traditional retirement account and then “backdoor convert” the account into a Roth IRA.

Legendary investor and billionaire Peter Thiel has used a Roth IRA to grow a $5 billion dollar account on which he legally owes zero taxes. Sounds too good to be true? Well, it’s not, but you need to know the rules and techniques to do the conversion correctly.

What is a Backdoor Roth IRA?

The good, old-fashioned version of the backdoor Roth IRA involves:

Backdoor Roth conversions allow high-income earners an opportunity to contribute to a Roth IRA, despite being over the low income thresholds.

Who is a Backdoor Roth IRA For?

Covered By Retirement Plan At Work

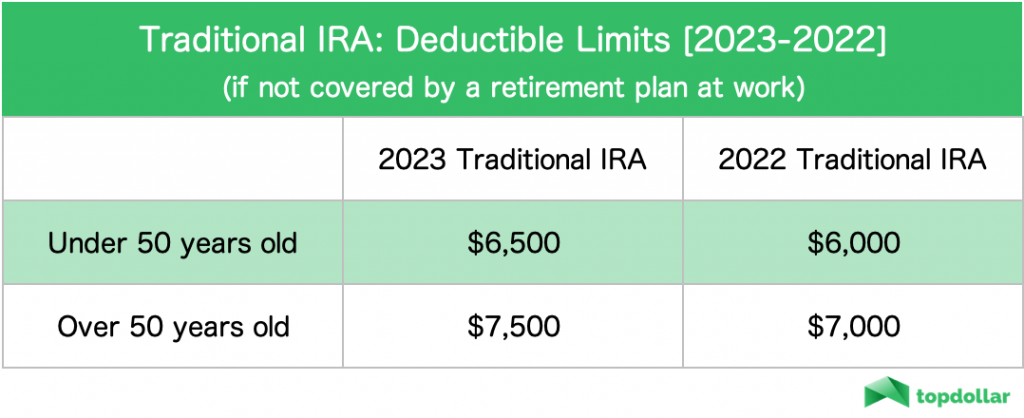

The regular backdoor method is best used by individuals already maxing out a company retirement plan such as a 401(k). If a retirement plan at work covers you, you are probably not eligible to make additional tax-deductible contributions (with pre tax income) to a Traditional IRA plan.

However, there are no income limits for making after-tax contributions (non-tax-deductible) to an IRA.

If you fund your Traditional IRA is funded with after-tax money, you will not owe taxes when doing a Backdoor Roth strategy. The net result after the Roth conversion is zero change in post-tax dollars, but the tax benefits are that the money is now in a Roth that could grow tax-free and never be taxed even when the investments are sold.

Basically, the backdoor Roth IRA is just (tax-free for life) gravy!

A tax-deductible contribution to a Traditional IRA isn’t an option for most people covered by a company plan; however, if you are under these income limits, you be eligible to contribute to a Roth IRA using the standard, front door method.

Not Covered By Retirement Plan At Work

If you are not covered by a company-sponsored retirement plan, you are then eligible to make a tax-deductible contribution to a Traditional IRA.

In this situation, because your opportunity cost of converting to a Roth IRA requires paying taxes, it is not as obvious a no-brainer to convert. This circumstance falls into a variation category listed below because of the tax consequences.

Backdoor Roth Variations

There are two slight variations to the “backdoor Roth” which we will discuss:

All variations raise the same essential question: choosing whether to realize the taxable income for the benefit of moving money into a Roth. The best choice for determining if it’s worth converting comes down to choosing the best time for the conversion process.

Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is a related but completely different variation of the strategy.

In a nutshell, this strategy uses a fully funded Traditional 401(k) (which is not available in most company-sponsored 401(k) plans). Mega Backdoors are also becoming a less necessary strategy as most company-sponsored programs now offer a Roth 401(k) option (which, curiously enough, has no income limit).

The logic for deciding to do a Mega Backdoor Roth IRA conversion is the same consideration as deciding whether to contribute to a Roth 401(k) or a Traditional 401(k) and is analyzed here.

Technically the Mega Backdoor Roth IRA may still be of interest to a small portion of ultra-high income earners, as its value allow one to maximize a Backdoor Roth contribution at the expense of getting an immediate tax deduction from a Traditional 401(k) contribution.

![]() Top Dollar Edge: I generally only recommend the Mega Backdoor Roth IRA to individuals who are both high earners (in the top marginal tax bracket) and who plan to generate enough passive income in future years that they will likely never drop into a lower tax bracket in the future.

Top Dollar Edge: I generally only recommend the Mega Backdoor Roth IRA to individuals who are both high earners (in the top marginal tax bracket) and who plan to generate enough passive income in future years that they will likely never drop into a lower tax bracket in the future.

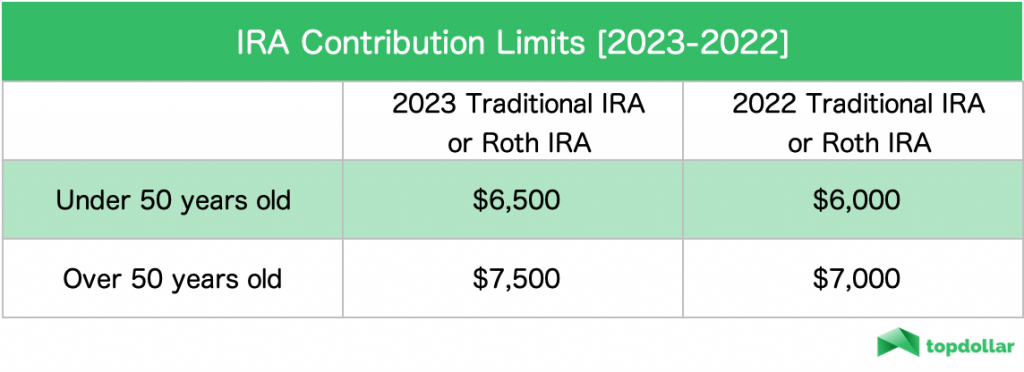

Backdoor Roth IRA Contribution Limits

Here are the maximum annual contributions for the Backdoor Roth strategy.

The amounts aren’t huge, but you could (and should) do a different Backdoor Roth IRA conversion every year- which I do myself.

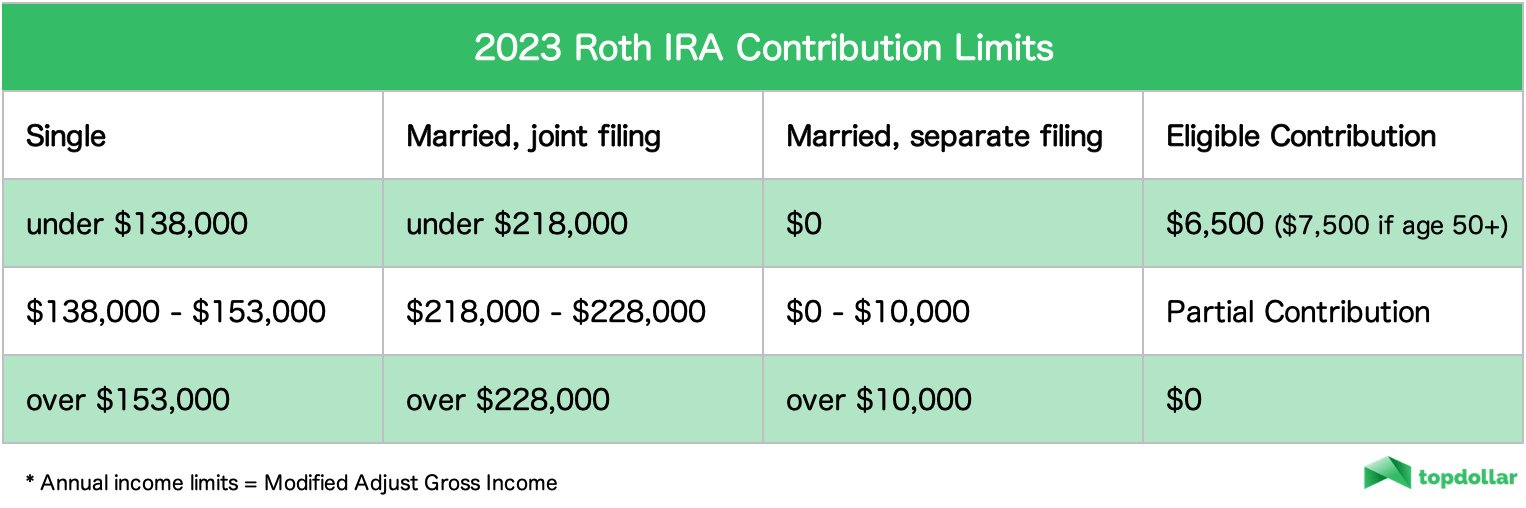

Roth IRA Income Limits

Remember, it is unnecessary to jump through the loopholes if you are a low-income earner and qualify directly for a Roth individual retirement account.

Advantages of a Backdoor Roth IRAs

Tax-Free Growth Forever

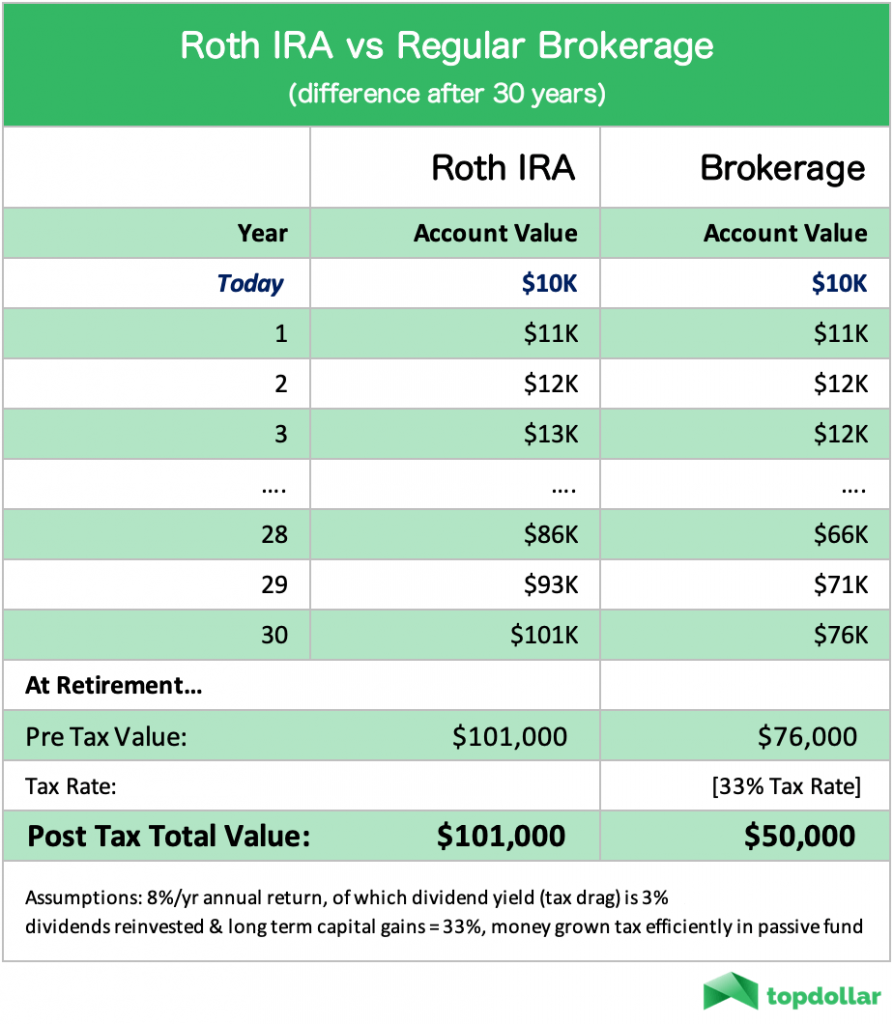

Doing a backdoor Roth with post-tax dollars (the standard method) is mostly all upside. All your earnings will grow tax-free, and you will incur no capital gains taxes and no dividend taxes ever again.

Without the backdoor Roth, the next best alternative a tax savvy investor could make is just to put the money in a tax-efficient index ETF and never sell until retirement. The comparison in retirement savings between the Roth account and the next best tax-efficient option is unmistakable.

No RMDs

Required minimum distributions (RMDs) exist for all types of tax-deferred retirement accounts except the Roth IRA. This means there are no requirements to withdraw the money from your account forever. By comparison, other retirement accounts (even the Roth 401(k)) enforce RMDs, ending the tax-free growth beginning at age 72.

Estate Planning

The lack of RMDs requirements and IRA inheritance rules make Roth IRAs an excellent estate planning tool. Because RMDs are not required, any money not withdrawn could continue to grow without having to pay taxes for life. Additionally, your beneficiaries can inherit the money tax-free and allow the Roth IRA to continue to grow tax-free for an additional ten years while they withdraw the money.

Disadvantages of a Backdoor Roth IRA

Investment Limitations

All retirement accounts, including Roth IRAs, have some limitations you should be aware of. Firstly, if you are trying to invest in certain assets that your plan sponsor doesn’t offer or isn’t approved for retirement accounts by the IRS.

Ineligible investments (for any Roth or Traditional IRA assets held) include physical collectibles, life insurance products, and certain types of derivate investments (such as selling naked calls).

Additionally, IRAs are not eligible for leverage. You cannot trade on margin or take any direct loan against the money in the account.

59 ½ Age

As a retirement account, money is intended to be kept within the Roth IRA until age 59 ½. If you need access to the cash before this age, your earnings will be hit with taxes and penalties. Once you meet the age requirement, all the money can be withdrawn without any penalties.

In a Roth IRA, you can always withdraw contributions at any time without penalty or taxes in the event you need the cash. But if you want to take out everything, any earnings you have accumulated will be hit with taxes and penalties.

5 Year Rule

The 5 year Roth IRA rule references the minimum number of years you must wait to withdraw earnings without taxes and penalties. This rule supersedes the age requirement, so if you opened a Roth IRA at age 58, you would have to wait until 63 to withdraw all of your converted funds without taxes. Technically if you break the 5 year rule after age 59 ½, you will have to pay only taxes on your earnings but not the 10% penalty.

The 5 year period begins on Jan 1 of the year of the Roth IRA conversion. For example, if you make conversions on April 1, 2023, you would only have to wait until Jan 1, 2028 to hit the 5 year rule. Note that the conversion date (not the initial contribution date) sets the year for the Jan 1 start date. Each conversion has its own 5 year period.

The “Other” 5 Year Rule (For Front Door Roth IRAs Only)

The other 5 year rule is being mentioned here for clarification but does NOT apply the Roth IRA conversions, but rather to front door Roth IRA contributions.

The “other” 5 year period begins on Jan 1 of the tax year of the Roth IRA contribution (which is due tax day, the year following the tax year). For example, if you made a front door contribution for a Roth IRA on April 1, 2023 (for tax year 2022), you would only have to wait until Jan 1, 2027, to meet the 5 year rule.

If you have multiple “front door” Roth IRAs or have made multiple contributions to the same “front door” Roth IRA- the 5 year clock also starts from your first contribution to any Roth IRA. Once you hit the 5 year rule on your first contribution, subsequent contributions or multiple “front door” Roth accounts are no longer restricted.

Best Time to Convert to a Backdoor Roth IRA

The timing is very straightforward if you plan to do a backdoor Roth with a non-deductible Traditional IRA contribution (the standard method).

Step #1 requires contributing to a Traditional IRA: You can do this anytime starting Jan 1 (the tax year) through April 15 (the following year).

For example, for tax year 2023, you can make your contribution anytime between Jan 1, 2023 – April 15, 2024.

Step #2 is the conversion, which you can do at any time with no deadline. Nevertheless, I recommend converting soon after you contribute to begin accruing tax-free growth. By waiting a significant amount of time, you may generate earnings on your Traditional IRA investments, which would require paying taxes when doing the conversion.

Depending on your brokerage firm, you can usually do the conversion within a few days after making the initial IRA contribution.

IRA and 401(k) Conversion Rules

When completing the conversion (rollover) process from the Traditional IRA to the Roth IRA, there are a few important rules to understand in order to avoid unintended tax consequences.

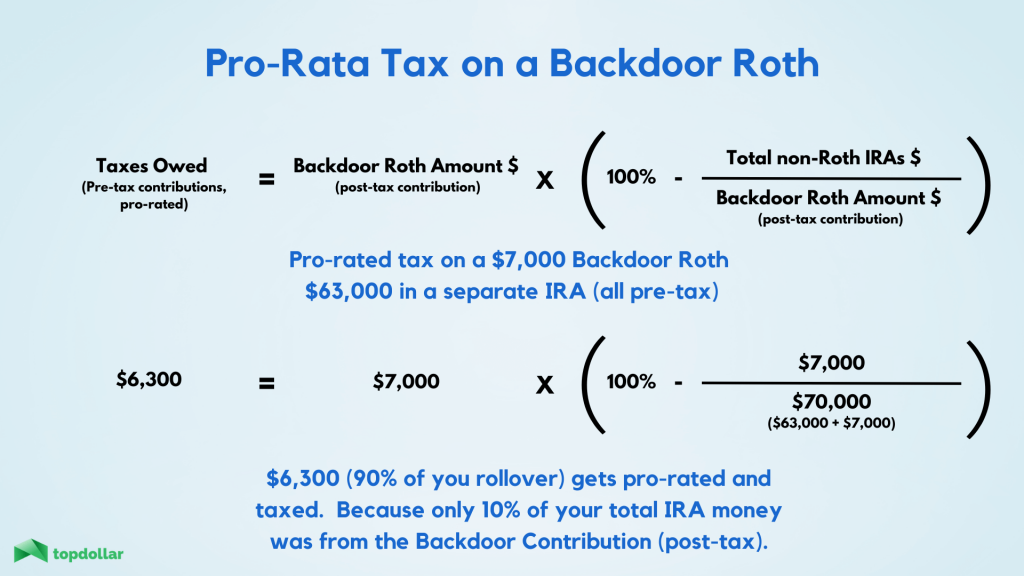

Pro-Rata Rule

The pro-rata rule is the most important rule to be aware of when converting to a Roth because a screw-up can cause you to accidentally owe taxes on other individual retirement accounts you may have. Not accounting for the pro-rata rule during the Backdoor Roth strategy is also the most common and painful mistake made, and can cause a significant tax bill on a prior year’s tax deduction.

The IRS requires that if you convert a pre-tax IRA plan to a Roth IRA, you need to convert all of your pre-tax IRA plans together on a pro-rated basis. This means you cannot have any other Traditional IRAs or pre-tax IRAs besides the one being converted.

Pre-tax IRA plans include:

The only way to avoid getting pro-rated on your conversion is to not have any other pre-tax IRAs outstanding by the end of the year. The following options exist for dealing with a potential pro-rata situation:

- Roll the other IRAs into a 401(k) or 403(b) company retirement plan.

- Open an Individual 401(k) plan, and roll the other IRAs there.

- Choose to convert the other IRA plans to a Roth and pay taxes.

Choosing to convert your IRAs (made with deductible contributions) only makes sense if you can afford to pay the taxes out of your current earnings without stress. This variation of the backdoor Roth is not recommended if your annual income puts you in the top marginal tax bracket for paid taxes. For high earners, there may often be a better time to convert a Traditional IRA or 401(k) to a Roth, especially if you have a sizeable account.

Direct Rollover vs Indirect Rollover:

Trustee-to-Trustee Transfer / Same-Trustee Transfer

An inter-trustee transfer is the best way to handle a rollover. This method has the financial institution move the money from one IRA to another IRA. Ideally, you could further simplify this process by utilizing a “same trustee transfer” by converting funds within the same financial institution.

For example, open a Vanguard Traditional IRA and a second Vanguard Roth IRA account, and have the trustee (Vanguard) move the money seamlessly from one account to the other.

Direct Rollover

A direct rollover involves contacting the administrator of the sending and receiving financial institutions. They will advise you of any paperwork you may need to fill out and will either handle the transfer directly or send you a check.

If they insist on sending you a check, the check should be made out to the new account, not your name. This will require one extra step, where you will need to forward the check to your new Roth account administrator and ensure the funds are deposited.

Indirect Rollover

Try to avoid an indirect rollover for backdoor IRA conversions, as it will often create unnecessary complications.

In an indirect rollover, an administrator will send you a personal check, and you will have to forward the check to your new Roth account in the same manner as a direct rollover.

The extra complication of the indirect rollover is twofold. First, you have 60 days to complete the rollover in order to avoid penalties. Second, normally taxes are withheld at 20% from indirect rollovers. Although your contribution is made with post-tax dollars, administrators don’t know the tax status of these funds and have been known to withhold 20%. This mess would require you to reclaim the withholdings on your tax return and will reduce the amount that is converted into the Roth IRA.

Is There a Once-Per-Year Rollover Rule?

There is a confusing rule surrounding once-per-year rollovers for IRAs. This rule only applies to indirect IRA rollovers and is not applicable to direct transfers. Additionally, the once-per-year rule only applies to rollovers (and not conversions) from a nontaxable IRA (Traditional, Rollover, SEP, SIMPLE types) to a different nontaxable IRA.

The rule does not apply when converting from company accounts such as 401(k) or 403(b) plans to a Backdoor Roth IRA either.

![]() Top Dollar Edge: If you are doing multiple backdoor Roth IRA conversions from multiple retirement accounts within one year, that’s allowed.

Top Dollar Edge: If you are doing multiple backdoor Roth IRA conversions from multiple retirement accounts within one year, that’s allowed.

Step-By-Step Guide To Creating a Backdoor Roth

Step 1. Fund a Traditional IRA account.

Contribute money up to the annual limit for yourself (single filers) and your spouse (if married filing jointly or married filing separately). If you do not already have a Traditional IRA account, you will have to choose an institution (such as Vanguard or Schwab) to set up a new IRA account.

After funding your Traditional IRA, I recommend not allocating your newly funded money to any specific investments; just leave it as cash, or cash equivalent funds, until after the conversion. The reason is to avoid unnecessary tax reporting complications and realizable taxable gains.

If you are converting from a pre-existing IRA or 401(k), this funding step does not apply.

Step 2. Backdoor Roth IRA Conversion

There is no time limit on the actual Roth conversion.

You may have to contact the administrator over the phone for instructions and paperwork, but often you can do it all online. Both Vanguard and Schwab offer straightforward online options.

![]() Top Dollar Edge: I only recommend either a trustee-to-trustee, same-trustee transfer, or direct rollover conversion method. The options are the easiest and will avoid the common complications of indirect rollovers.

Top Dollar Edge: I only recommend either a trustee-to-trustee, same-trustee transfer, or direct rollover conversion method. The options are the easiest and will avoid the common complications of indirect rollovers.

If converting within the same institution (same-trustee transfer), you could often make the account transfer online from the Traditional IRA to the Roth IRA. Some companies will let you transfer the funds immediately, while others will make you wait several days before converting.

If you perform a regular backdoor Roth (funding in Step #1 with POST-TAX dollars), there will be zero tax implications.

If you are performing a variation: backdooring a pre-existing IRA or 401(k) which was previously funded with PRE-TAX dollars, most or all of your accounts will probably be subject to ordinary income tax, as discussed earlier.

Nevertheless, when doing the Roth conversion, you will likely be notified that it is a taxable event. This is because the sending brokerage firm only knows the money is leaving from a Traditional (pre-tax) to a Roth (post-tax) account. The firm does not know if you funded the Traditional account with tax-deferred money or not.

Step 3. Allocate Investments

At this point, don’t forget the funds you transferred to your Roth IRA. Your money is likely sitting in cash or in a money market fund until you allocate it to specific investments.

Make sure to allocate your funds to investments that are consistent with your investment plan as soon as possible. Remember, an IRA is just an account; investments still need to be allocated as in any brokerage account.

![]() Top Dollar Edge: If you are looking to invest in passive index ETFs which specific asset classes (which I highly recommend), take a look at my list of best ETFs for investing.

Top Dollar Edge: If you are looking to invest in passive index ETFs which specific asset classes (which I highly recommend), take a look at my list of best ETFs for investing.

Step 4. Double Check For No Pro-Rata-Rule Accounts

At this step, please do a double-check, and make sure you don’t have any money left over in any Traditional IRA, Rollover IRA, SEP IRA, or SIMPLE IRA. If you do, don’t panic, you have until the end of the conversion year to roll the funds to another account if you forgot to do so beforehand.

As a reminded the following three options exist for dealing with funds in these IRAs:

You can leave any account opened that has zero dollars in it. Many investors keep a Traditional IRA open with no money, so they don’t have to reopen a new IRA every year to do another Backdoor Roth.

Step 5. Pay Taxes

Report the transactions correctly by filing IRS Form 8606 for each account (per spouse).

If you had any significant earnings between the contribution and the conversion, the profit is fully taxable at ordinary income tax rates, reportable on Form 8606. If the profits are less than 50 cents, they can be ignored based on IRS guidelines.

If you have a loss (unlikely, but possible), you can carry that loss forward on your 8606 and write it off against a potential Roth conversion with gains in the future.

Bottom Line

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.