ETFs vs. Mutual Funds: What’s the Difference?

Are you choosing between investing in ETFs vs. mutual funds and unclear on what’s the difference between these funds? This article will explain the similarities and differences between these common investments, and by the time you are done reading, you’ll be an index fund savant.

For over fifteen years, I have worked in ETF strategy on wall street and have dissected and traded thousands of different funds. I currently manage an investment portfolio that is heavily invested in index funds, and I must carefully consider each investment.

Needless to say, I love this topic. So let’s jump in and start with the basics on the different types of funds, and then we’ll explore whether ETFs or mutual funds are the best options for you.

What is a Mutual Fund?

A mutual fund is a collection of money managed by a financial institution. This institution pools money from various investors and allocates the funds based on a pre-defined strategy. All investors in a mutual fund maintain an identical exposure and fund composition, regardless of their investment size. Mutual funds often invest in stocks and bonds, but may invest in other assets- according to the details in their prospectus.

Mutual funds are managed by fund managers who directly handle all new investments (buying) or redemptions (selling). All purchases or sales are executed at the end of the day’s valuation (referred to as net asset value- NAV). Any mutual fund order placed during the trading day is held and executed by the fund manager at the daily closing price.

Because mutual fund shares cannot be actively traded during the day, they are unsuitable for short-term traders but rather intended for use by long-term investors only. Furthermore, a mutual fund investor is often required to purchase or redeem shares in large minimum increments – usually in hundreds or thousands of dollars.

Mutual funds’ assets now total approximately $27 Trillion in the U.S. (2023). Much of this has been fueled by the limited investment choices of investments in personal retirement funds, specifically 401(k)s. Unlike individual retirement accounts (IRAs), 401(k) plans only offer mutual funds, pushing significant assets into MFs over the past forty years.

Fee Structure

Mutual funds have various types of fees that should be clearly understood before investing.

- Load: “Load” refers to a sales fee or commission. The load can be charged when first purchasing the shares (front load), when redeeming/selling shares (back load), or throughout the year (level load). Often issuers who charge these different loads refer to different classifications as either Class A/B/C shares, respectively.

- No Load: Many mutual funds now have no-load fees (zero commissions). I recommend sticking only with no-load funds, as loads will ultimately erode your investment returns significantly, and there are many excellent no-load funds.

- 12b-1 Fees: These sneaky fees are charged for marketing expenses, which the issuer deducts directly from the mutual fund itself. That’s right- you may be paying for the issuer to advertise the funds to other investors. Sounds awful? It is. You should determine what the 12b-1 fees are (if any) in the prospectus before investing (and probably avoid these funds if the fees are substantial).

- Annual Management Fees: These are annual fees for fund management, funding, and administration costs. Fortunately, these fees have seen a significant reduction over the past 20 years and seem to be creeping slowly to 0% across the most competitive index funds.

What Are Index Funds?

Here’s where things get a little tricky- people like to throw around the term “index fund,” sometimes incorrectly.

Mutual funds have a clear mandate or strategy, which is defined in their summary prospectus. The fund manager (who is in charge of the fund) is obligated to execute the fund’s stated strategy. Some funds aim to track a specific index- these are known as index funds.

An index fund may track a well-known index- such as the S&P 500 or the Dow Jones Industrial Average. An index fund may also track a less common index, but what’s important is that the fund does not choose what to invest in itself, it must follow the methodology of the index it is tracking.

These fund managers must follow specific, defined rules and may not apply their own discretion to the investment strategy. Index funds offer the lowest fees across all mutual funds- usually having no loads and minimal management fees. I am a huge proponent of investing in index funds.

Active Funds

Active funds are the alternative to index funds- active funds permit fund managers to exercise discretion and pick individual stocks and holdings. Their investment objectives will not be as clearly defined as index funds. Actively managed mutual funds generally charge higher fees to compensate fund managers for their research, diligence, and efforts in attempting to maximize returns.

Whether or not you believe that active managers can outperform traditional index funds over time (an ongoing debate)- the data speaks for itself. Less than 10% of active managers have consistently outperformed the S&P 500 index over the past ten years. Furthermore, active funds create less tax efficiency by generating taxable capital gains on their “winners,” which creates more tax drag on active funds.

The scope of this article is not to argue against active funds, but I don’t invest in them personally, and don’t support them for 99% of individual investors.

What are Exchange Traded Funds (ETFs)?

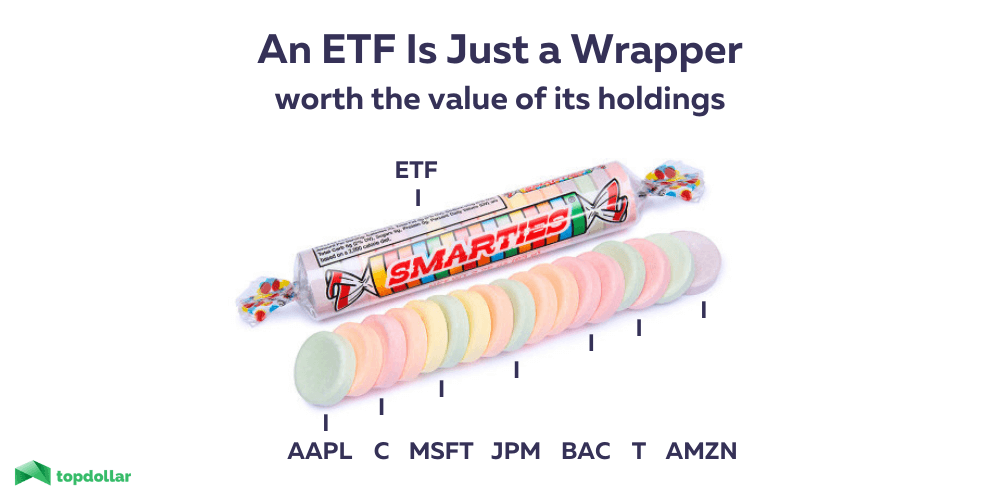

Like mutual funds, exchange-traded funds (ETFs) hold baskets of investment assets- such as stocks, bonds, commodities, or any other assets the fund states in their SEC filed prospectus. An ETF is just a wrapper that holds a diversified selection of multiple investments.

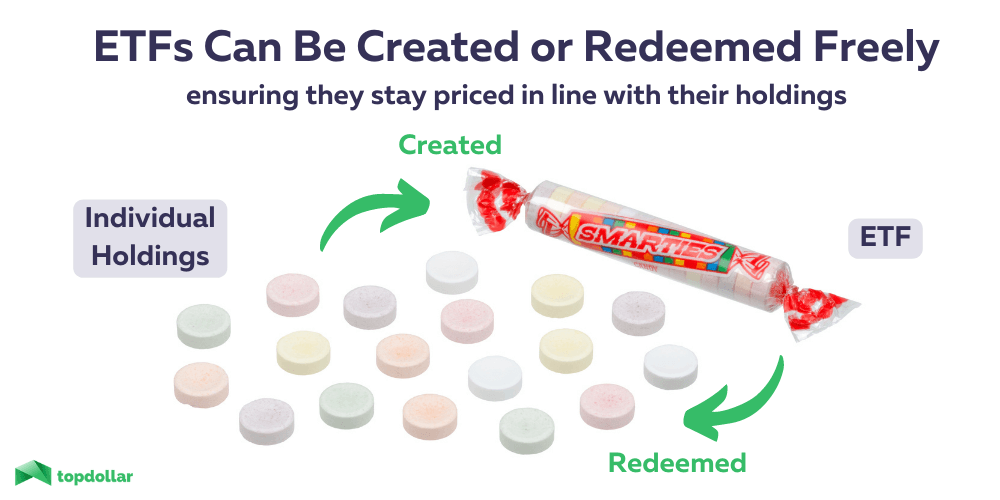

The value of any exchange-traded fund is simply the total value of the holdings inside. ETFs are completely transparent, and large broker-dealers (call authorized participants in the industry) can break open (redeem) the ETFs or create new blocks of ETFs in exchange for a complete basket of holdings. This process of converting holdings to ETFs (or vice-versa) is known as arbitrage and keeps all ETF trading in line with their fair values.

Quite different from mutual funds, ETFs trade throughout the day on a stock exchange just like any other individual stock does. As explained above, individual investors can buy or sell shares from active traders, banks, institutional investors, and liquidity providers who arbitrage the ETFs in the stock market. Because of this mechanism, ETFs are often very liquid and reflect a fair price for investors to buy or sell at any time during regular market hours.

Fee Structure

Because ETFs trade on an exchange, they don’t incur explicit sales or load fees, as some mutual funds do. Similar to mutual funds, ETFs charge annual management fees- often ranging from 0% – 1%, with most competitive funds charging between 0.05% – 0.45%. Like mutual funds, there are a lot of lousy, overcharging funds. I recommend checking out my list of best ETFs to invest in, with full explanations and methodology to stick with the cheapest ETFs.

Are ETFs Active Funds or Passive Index Funds?

In the same manner that mutual funds can be actively managed or passively track an index, ETFs come in the same two varieties.

Like mutual funds, active ETFs charge higher management fees than index funds, but have yet to show long-term outperformance to justify these higher costs. Therefore, I recommend sticking with passively managed ETFs over actively managed funds.

ETFs vs. Mutual Funds: Similarities

At the end of the day, exchange-traded funds and mutual funds are more alike than different.

Holdings

Most importantly, both fund types hold baskets of multiple assets- minimizing individual securities risk through diversification. A diversified portfolio is critical to an intelligent investment allocation- and many ETFs and MFs hold hundreds or even thousands of different assets.

If you are investing in passive index funds (which I highly recommend), both fund types offer similar low-cost choices. Additionally, both of these funds are excellent choices for non-professionals who do not have the time or interest to learn how to invest in individual companies (using research and valuation techniques).

Professional Management

Expert fund managers or management organizations handle ETFs and mutual funds. Despite being actively or passively managed, rest assured, fund managers will oversee the diversification and proper allocation of the fund’s strategy.

Choice Variety

Both fund types allow investors to access a wide range of asset classes, including stock funds, bond funds, commodity funds, real-estate trusts (REITs), money market funds (cash-equivalent instruments), or a combination of these. In fact, many fund issuers- such as Blackrock, Vanguard or Schwab, have the same fund manager oversee multiples classes (versions) of the same fund- one as an ETF and a second class as a MF.

Safety and Suitability For Investors

The individual holdings within the funds fully collateralize both mutual funds and ETFs. That means you don’t need to worry about the funds going under or something fishy happening with your investments.

Nevertheless, there are a few types of exchange-traded products that I would not recommend for long-term investors. This group includes leveraged or inverse ETFs. These funds hold complex derivative products – such as swaps and futures – to synthetically created opposite or increased exposures to their holdings. Feel free to read more about these types of funds and some of the additional risks they pose.

ETFs vs. Mutual Funds: Key differences

While both ETFs and mutual funds have similarities, intelligent investors should understand the difference between them to determine which is better for them.

Intra-Day Liquidity

The main difference between ETFs and mutual funds is that ETFs can be traded throughout the day, just like stocks. Mutual funds, on the other hand, can only be purchased or sold at the close of each trading day at the end-of-day calculated price- known as the net asset value.

Personally, I prefer investing in ETFs, because of the ability to trade intra-day. I like to set limit orders in the market and be confident that if the price moves below my order, I will buy shares (or the converse on the sell side). Nothing would infuriate me more than having to wait to buy a mutual fund on a day with heavy market volatility, only to see the market rally back up before the end of the day.

Spread Costs

Because ETFs are traded on an exchange, any time you buy or sell, you will have to pay a transaction cost, known as the “spread.” The spread is the difference between the prices quoted on the exchange between people willing to buy (the bid) or sell (the ask). You can learn more about spread costs in my guide to best ETFs.

The spread cost could accurately be considered a small trading commission. Because many mutual funds now offer no-load fees, investing in a no-load mutual fund will offer a slightly cheaper transaction cost.

For most competitive ETFs, spread costs are usually between 0.02% – 0.06%. This cost is only paid when buying or selling (not annually), so it’s less of a concern for long-term investors.

Additional transaction costs used to be charged by most brokers, but recent years have seen increasingly most brokers charging zero transaction costs on stock and ETF shares.

Premium / Discount Costs

As I briefly mentioned, ETFs are kept in line with their fair value due to the creation/redemption process, which allows traders and institutions to transfer the replicated fund holdings into and out of the fund based on supply and demand. Nevertheless, ETFs may trade at small premiums or discounts to their fair net asset values.

![]() Top Dollar Edge: Having traded ETFs professionally for over 15 years, I can tell you the concern that ordinary investors should have for ETF premium or discount is inconsequential. Professional traders only sometimes see funds trading below or above the fair value – and this amount is seldom more than 0.05% (only during periods of extreme volatility).

Top Dollar Edge: Having traded ETFs professionally for over 15 years, I can tell you the concern that ordinary investors should have for ETF premium or discount is inconsequential. Professional traders only sometimes see funds trading below or above the fair value – and this amount is seldom more than 0.05% (only during periods of extreme volatility).

I don’t believe ordinary investors should worry about the costs of premium or discount on their investments. Furthermore, these deviations are usually more pronounced on non-U.S. asset classes and rarely significant for the most active U.S. stock and bond ETFs.

Tax Efficiency

ETFs typically create smaller capital gains for investors because they have lower turnover and can manage the cost basis of their assets through the in-kind creation/redemption process.

Thus, ETFs are more tax efficient than MFs.

A sale of securities within a mutual fund may result in financial gains for owners, even if the total mutual fund investment has an unrealized loss.

Both fund types may either pay dividends or reinvest them, but dividend taxes will be similar for both types of funds.

Transparency

ETFs report their holdings every day- and professional traders and financial institutions can see what positions funds are holding, and what changes are made day-to-day. Mutual funds, on the other hand, are required to post their holdings on a monthly or quarterly basis giving ETFs the clear upper hand when it comes to total transparency.

For actively managed funds, investors could see what stocks the fund manager is buying or selling daily. An individual investor will have more information available and could decide to sell the ETF because they disagree with the fund manager’s strategy. Conversely, in an active mutual fund, an investor likely won’t know which positions a fund manager is buying or selling until the monthly or quarterly reports are published.

Minimum Investments

ETFs do not have a minimum initial investment and are acquired in whole shares. They are simply traded like stocks. An ETF can be purchased for the price of one share, referred to as the ETF’s “market price.”

However, even the minimum one-share investment has seen recent changes, as some brokers are now offering “fractional shares.” This service, offered by some brokers, lets investors own an exposure equivalent to the ETF (or an individual stock) for a fraction of the actual share price.

MFs have a more significant minimum entrance requirement than ETFs. These minimums can differ based on the fund and brokerage firm. Vanguard, for example, demands a $1,000 minimum commitment for most mutual funds, while American Funds’ Growth Fund of America requires a $250 first deposit.

Some mutual fund managers (such as Vanguard) have different classes within the same mutual fund with different fees. For example, a mutual fund may have a management fee of 0.24% for an investment of $1,000 – $100,000, while the same fund offers a 0.15% fee for investments between $100,000 – $5 million.

ETFs, by comparison, only come in the one version listed on the exchange for everyone- they are more democratic in that manner.

History

Mutual funds have been established for nearly a century, with the first mutual fund launched in 1924. Exchange-traded funds (ETFs) are novel in the investment world, with the first ETF, the SPDR S& P 500 ETF Trust, debuting in January 1993. (SPY).

Mutual funds’ more extended history and their universal adoption by most 401(k) plans (prior to ETFs) explain why there are trillions more in mutual funds vs. ETFs. However, ETFs have been the faster-growing asset class over the past fifteen years, as investors seem to favor the liquidity and transparency available within ETFs.

ETFs vs. Mutual Funds: Which is the better option?

Choosing between exchange-traded funds vs. mutual funds depends entirely on the investor. Any index fund, whether an ETF or MF, will mirror that index’s performance. Thus, if an index fund is set to track the NASDAQ, and the NASDAQ drops or gains 30%, the fund will follow suit.

ETFs offer several advantages to beginner investors over mutual funds.

- The entry capital requirements for ETFs are generally lower and thus allow people with less capital to compound their gains over time than with MFs.

- ETFs offer better tax efficiency than MFs as they turn over fewer capital gains and have fewer taxable events, like opening you up to lesser ordinary income tax rates than mutual funds.

- Mutual fund investors must wait to execute trades at the daily closing value (NAV). This constitutes a significant drawback compared to ETFs. ETF investors can see the market price of their ETFs at any time, without delay.

There are increasingly more ETFs being launched every day- bond ETFs, stock ETFs, currency ETFs, commodity ETFs etc. But remember, all ETFs are not created equal- some have overpriced management fees or low on-exchange liquidity. But don’t be worried- my unbiased list of best ETFs includes the ETFs with the lowest costs and highest liquidity.

Conclusion

There are various aspects to consider when selecting between funds. If you have a 401(k) plan, your investment options are likely limited to mutual funds. If you are investing in a regular brokerage account or a Traditional or Roth Individual Retirement Account (IRA), most funds will be available to you. Hopefully, my provided information will help you make the best choice based on your own needs.

Fear not, as most equivalent index funds will perform identically, whether they are ETF or mutual fund varieties. The important consideration comes down to tax-efficiently, liquidity, transparency, and cost structure.

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.