Schwab vs. Vanguard ETFs and Mutual Funds: Which is Best?

This review will compare Charles Schwab vs. Vanguard on ETFs, mutual funds, index funds, platforms, trading tools, account types, fees, research, and more.

Introduction: Charles Schwab vs. Vanguard

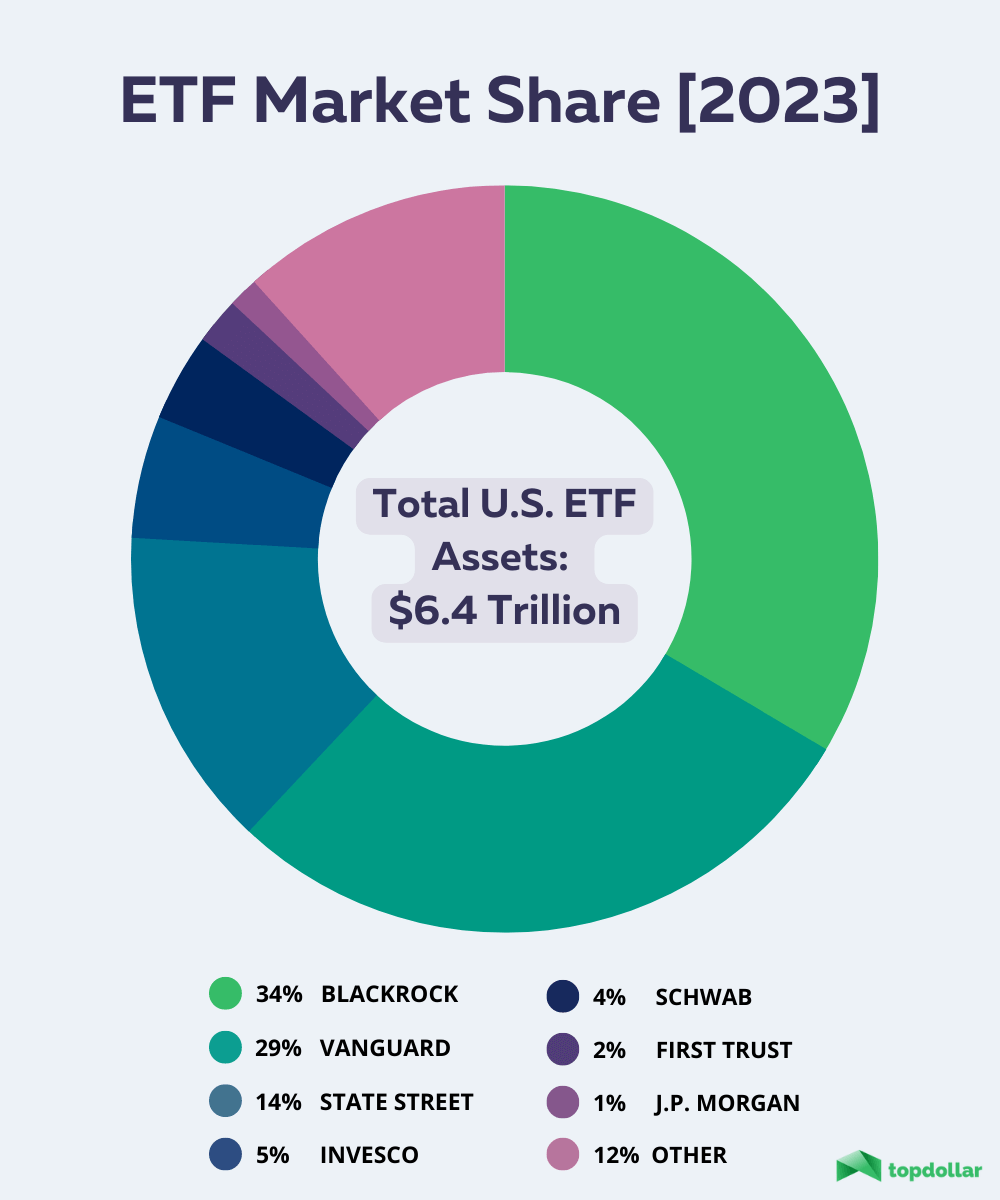

Schwab and Vanguard are both juggernauts in the world of brokerage and wealth management. Both financial institutions manage assets totaling around $8 trillion dollars, and each has a heavy percentage of assets under their mutual fund and ETF businesses.

As ETFs have been one of the fastest-growing asset classes over the past twenty years, both Schwab and Vanguard have chosen to double down on ETF and index fund offerings. Vanguard’s offering has always included a full range of passive index funds- a niche they pioneered since their inception. Schwab is equally formidable, often considered the pioneer of low-cost brokerage accounts, and also offers a wide array of low-cost options.

I have spent 15 years of my career as an ETF trader and strategist, so digging through all the nuances of these investment products is a favorite pastime of mine. If you are deciding between Schwab ETFs vs. Vanguard ETFs for your investing needs, I will break down all the significant differences you need to make an informed decision.

Additionally, I will provide some broader comparisons of Schwab vs. Vanguard and highlight which company performs best in each category.

Overview: Schwab vs. Vanguard

Schwab

Vanguard

Larger Selection of ETFs: Schwab vs. Vanguard

Regarding ETFs, Vanguard offers a broader selection of funds than Schwab. Vanguard is an asset manager with over 40 years of experience, and they offer a variety of ETFs that can suit any investor’s needs.

With Vanguard, you can choose from ETFs that track different indexes, are focused on specific sectors, or even ETFs that are designed for long-term investing. Vanguard also has a team of experts who can help you select the right ETFs for your portfolio and provide guidance on asset allocation. Vanguard currently issues over 80 ETFs.

In contrast, Schwab only has a limited selection of ETFs- approximately 30, and they do not have the same depth of experience as Vanguard. As a result, Vanguard has more choices for investors who want to build a diversified portfolio with exchange-traded funds.

Lowest Fees: Schwab vs. Vanguard

When it comes to investing, there are two main types of fees that you will encounter: management fees and transaction (trading) fees. Management fees are charged by the financial institution or fund manager that is managing your investment, while transaction fees are charged every time you buy or sell an investment.

Management Fees

When comparing Schwab and Vanguard, the two brokers are in a head-to-head battle to charge the lowest management fees in the industry. For example, the management fee for Schwab S&P 500 index fund is 0.03%, while the management fee for Vanguard S&P 500 index fund is 0.03%- the two cheapest in the business. I compare the best ETFs using criteria such as low fees and average expense ratio in this article.

Over time, small differences can add up to a significant amount of money, so always aim to minimize the management fee on any investment. Unfortunately, many investors don’t consider management fees, because they are charged in-house and are not reported on your brokerage statements.

Schwab and Vanguard both offer a variety of low-cost index funds that are perfect for investors looking to minimize their expenses. Schwab seems to be pushing the envelope to move fees to zero, while Vanguard continuously matches Schwab’s lower rates.

Higher Account Balances

Vanguard offers more competitive fees for wealthy retail investors or institutional-level investors. Vanguard refers to these improved rate classes as Admiral Shares or Institutional Shares, and these preferred rates can reduce fees by as much as half. Admiral shares require a minimum investment between, $3,000 – $100,000, depending on the fund. Institutional-level accounts, of at least $5 million, are offered the most significant discounts.

Transaction Fees (Trading Fees)

Both Schwab and Vanguard now offer zero trading fees for online trading of stocks, bonds, ETFs, and mutual funds. Schwab still charges minimal rates on options trades, while Vanguard offers several free option trades per month. Both Schwab and Vanguard have together defined the new industry norm- most brokers are no longer charging any transaction fees.

Other Fees and Restrictions

Vanguard does charge a flat $20 account service fee per year on all accounts (under $1 million). Schwab has no annual fees but has a minimum account of $1,000, while Vanguard has no minimum.

Both brokers also have various transaction fee schedules for over-the-phone trades (broker-assisted trades). Therefore, I advise you to use their online trading tools to avoid unnecessary trading costs.

Mutual Funds and Assets Under Management: Schwab vs. Vanguard

Regarding mutual fund offerings, Vanguard and Schwab are both industry leaders and likely comparable funds for most categories. Vanguard’s offerings include 300 proprietary mutual funds, covering a wide range of asset classes. Schwab funds, by comparison, offer about 50 proprietary mutual funds, with a heavy focus on target date funds.

Vanguard requires a minimum investment of $1,000 for mutual funds, while Schwab requires just a $100 initial investment.

When it comes to assets under management, Vanguard holds a slight advantage. Vanguard is one of the largest asset managers in the United States, with assets a bit above $8 trillion, second to Blackrock (iShares).

Schwab has been climbing the ranks rapidly over recent years and made a huge leap into third place after acquiring TD Ameritrade in 2020. Schwab has now amassed client asset totals just under that of Vanguard.

When it comes to mutual fund offerings and assets under management, both firms compete at the highest level, but Vanguard holds a slight edge.

Robo Advisor: Vanguard vs. Schwab

Robo advisors have been growing in popularity, as they offer many of the benefits of a traditional financial advisor (such as building your investment portfolio) at significantly lower fees. Both Vanguard and Schwab have robo-offerings services for individual investors.

Vanguard Digital Advisor fees are 0.20% to manage a Vanguard brokerage account. This is a lower fee than the industry average of 0.25% – 0.35%, the range charged by competitors such as Betterment, Wealthfront, Fidelity, and E-Trade.

Schwab has a fixed-fee model for their robo-advisor business, Intelligent Portfolios. Schwab charges $300 initially and $30/month going forward under the robo-advisor program. Therefore Schwab will be cheaper on a percentage basis if you have over $180,000 in your robo-advisor brokerage account.

Individual Retirement Accounts (IRAs): Vanguard vs. Schwab

Vanguard is famous for its focus on retirement accounts and long-term investment approach. Furthermore, Vanguard offers lots of investor education and retirement calculators to help account holders understand how much wealth they are on track to build for retirement. Truth be told, I use several brokerages- and have multiple retirement accounts with Vanguard.

Nevertheless, Schwab offers many of the same benefits that Vanguard pioneered. Today, both brokers offer thousands of funds (not all proprietary, but you’ll have access to funds from other companies). Both brokers offer the following retirement planning and the following retirement account types:

Tax Efficiency: Schwab vs. Vanguard

If you are investing in a non-retirement brokerage account, reducing taxable gains is often a focus, especially if you are in a high tax bracket. Tax drag in brokerage accounts will come from capital gains and dividends. Assuming you are a long-term investor and don’t actively create any taxable events yourself, your concern should focus on which broker’s funds are more tax efficient.

Capital Gains Tax

Just because you didn’t sell shares (and realize taxable gains) does not mean the fund itself did not sell any shares. Fund managers must buy and sell shares all the time- to conduct index rebalances, facilitate new investors, process corporate actions, and reinvest dividends.

Vanguard is in a league of its own when it comes to ultra-tax efficiency. Did you know Vanguard has a special tax status equivalent to a non-profit? It redistributes any profits to investors in the form of lower fees.

Additionally, Vanguard has a proprietary patent exploiting a tax fund provision for 14 of its funds, which crosses over to dozens of other mutual funds and ETFs. Because of this, Vanguard can distribute much fewer capital gains in its funds and may reinvest these amounts tax-free.

The total amount of capital gains paid (negative tax drag) varies fund by fund. But for many common funds, this “hidden tax fee” can be between 0.04% – 0.10% per year! This gives a significant edge to Vanguard over any other broker firm (including Schwab).

Trading Experience and Platforms: Schwab vs. Vanguard

Regarding trading platforms, Vanguard and Schwab have each established a different approach to their trading platforms. Vanguard offers a web-based platform that is easy to use and navigate, while Schwab offers a desktop platform that is more sophisticated and feature-rich. Vanguard’s platform is designed for investors who want to invest long-term, while Schwab’s platform is optimized for investors who want to invest more actively.

Schwab offers several enhanced tools- such as the StreetSmart Edge platform, for customizing charts and streaming real-time data and stock prices. Schwab offers several tools, such as the “All-In-One-Trade,” to build complex orders across various asset classes.

Schwab

Vanguard

In terms of offerings, both platforms provide access to a variety of options, including the ability to trade stocks, ETFs, bonds, options, and mutual funds. However, Vanguard’s platform is more limited than Schwab’s when it comes to the number of markets that you can trade. For example, Vanguard does not offer futures (derivatives) trading. As a result, Schwab is the better choice for active investors who want to trade more frequently in stocks, ETFs, options, and futures.

Mobile Apps: Schwab vs. Vanguard

Both the Vanguard and Schwab mobile trading apps offer a streamlined, user-friendly experience that makes it easy to trade and manage your portfolio on the go. However, there are a few key differences between the two.

The Vanguard app has a more minimalist design, with fewer bells and whistles than Schwab’s. This may make it less appealing to some investors, but it also results in a fast, lightweight app that doesn’t consume too much data or battery power.

Schwab’s app is packed with features, including news and market analysis, educational materials, and even social media integration. This can be helpful for investors who want to stay informed and learn as they go. However, it can also make the app feel bloated and slow down your device.

Both apps offer access to their broker’s online trading platform if you need to place a trade from your phone. Overall I would say Schwab has the better mobile app user experience. Schwab’s mobile app feels better designed but also more complicated for newer investors.

Banking Option: Schwab vs. Vanguard

Although a bit outside the scope of this comparison, Schwab does also offer full-service banking, while Vanguard does not. This can make it easier for investors to seamlessly transfer funds between their brokerage accounts and checking or savings accounts with lower costs and more simplicity.

Schwab offers full banking services, including credit cards, real estate mortgage loans (through Rocket Mortgage), and personal loans.

Schwab also offers competitive interest rates (for a bank) and debit card ATM fees reimbursement- not a worthless perk!

Education and Research: Vanguard vs. Schwab

Both Vanguard and Schwab differ significantly in terms of the quality and accessibility of their research.

Vanguard’s website is available to anyone looking to view its educational offerings. They have also integrated their learning center into the firm’s online account management system.

Vanguard offers basic stock screeners and charting for stocks, mutual funds, and ETFs. Vanguard does focus its research and planning on long-term focused asset allocation. I like the simplicity of Vanguard’s retirement calculators, which help you estimate your rate of return against your risk profile.

Schwab’s education and research offerings are way more comprehensive than Vanguard’s. If you want more options, Schwab will deliver, but I find their research tools to be a bit overwhelming (and I’m a semi-retired professional). Schwab’s stock and fund screens are most useful for active traders and more customizing with streaming data.

Furthermore, Schwab offers a ton of education, content, and market commentary through their quarterly “on investing” reports, “live daily” videos, “Choicology” podcast with Katy Milkman, and various workbooks and tutorials on complex trading strategies.

I would summarize the research by calling Vanguard’s offerings more ‘classic’, while Schwab has many shiny options and fancy tools. But will Schwab’s advanced tools make you a better return? That’s for you to decide.

Customer Service and Support: Vanguard vs. Schwab

Schwab has more comprehensive customer support, offering 24/7 support to customers both over the phone and online. Schwab also has over 300 branch locations throughout the U.S. for in-person walk-in help.

Vanguard offers only telephone and email support during ordinary business hours (8 a.m. – 8 p.m.), Monday – Friday. There is no online chat or support opinion through either its website or mobile app.

Vanguard says their wait time varies based on which client group you need to contract. Vanguard seems to favor account size when determining service priority; however, this is my speculation and can’t be supported with evidence.

Wrap-Up: Who Wins?

This was really a hard decision, and it ultimately depends on which factors are most important to you. Overall, I would have to give the overall edge to Schwab.

Schwab offers more comprehensive tools, support, and investment options which is important for many investors. However, I personally favor the low-cost fees and tax benefits of Vanguard. At the end of the day, I prefer greater savings and slightly higher returns over the features that Schwab offers.

Both brokers offer very similar investment options and competitive fee structures well beyond the industry average. Additionally, both brokers allow you to invest in ETFs and mutual funds from other companies- such as Blackrock or Fidelity.

If I were opening a long-term, buy-and-hold style investment account, I would choose Vanguard. If I preferred to be more active in my trading style, I would go with Schwab. Either broker is a great option. By the time I next update this review, the edge could easily swing the other way to favoring Vanguard.

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.