Traditional 401(k) vs Roth 401(k): Best Retirement Plan For Your Income Level

Deciding between a Traditional 401(k) or a Roth 401(k) for your retirement plan? The majority of company retirement plans now offer both a Traditional and Roth 401(k) option but do not provide the resources or analysis to determine which is better for your specific circumstance.

Is the Roth option the best retirement account? High income earners have a difficult decision to make between the two plans, while lower income earners can almost always benefit more from the Roth 401(k).

Let’s jump in and analyze the differences to make the best decision between these retirement accounts and understand which one will save you the most money.

What is a Traditional 401(k)?

Let’s take a step back and clarify the traditional employer-sponsored retirement plan details. The Traditional 401(k) retirement account allows you to contribute part of your pre-tax income into the plan, thereby reducing your taxable income by the total amount of your contribution.

The second benefit of a Traditional 401(k) is that your contributions grow tax-deferred until retirement when you start taking distributions. As distributions are taken in the future, the initial investment and all investment gains are taxed at ordinary income tax rates.

What is a Roth 401(k)?

A Roth 401(k) differs from a traditional plan in that contributions are made with post-tax dollars, so money contributed will not reduce your taxable income. Although you will not receive any immediate tax deductions from a Roth contribution, benefits will come later.

Contributions made into a Roth 401(k) will never be taxed again, and any growth in the Roth account will also never be taxed for life.

I’ve heard a Roth 401(k) is Better. Is This True?

Often Roth 401(k) accounts are blindly recommended as the better choice. Indiscriminately recommending the Roth takes the assumption that the saver is not in the highest tax bracket. Therefore anyone who plans to move into a higher income bracket over their career should (in most cases) contribute to a Roth plan while still in lower tax brackets.

Although money grows tax free in both types of accounts, the tax benefits of the Roth structure (paying taxes now and never pay income taxes again) is more pronounced while you are in a lower tax bracket. Therefore, the Traditional plan only should be considered by individuals who currently pay taxes at a top (or near top) marginal tax bracket.

Roth 401(k) vs Traditional 401(k) Key Takeaways

- The choice between a Traditional or a Roth account ultimately comes down to taking a tax break today vs. the future.

- If you are not currently in a top tax bracket, I recommend choosing the Roth 401(k).

- If you are in a high tax bracket now, and believe you will be in a lower tax bracket in the future, a Traditional 401(k) makes sense.

- Opt for the tax deduction when you anticipate your income tax rate will be the highest.

Traditional 401(k) vs Roth 401(k) For High Income Earners

If you are currently a high income earner, you will find the decision to be extra complicated, primarily because the tax advantages of taking the tax deduction today are significantly greater.

The key consideration between a Roth 401(k) vs Traditional 401(k) for high income earners depends on whether you anticipate a future when you will be in a significantly lower tax bracket.

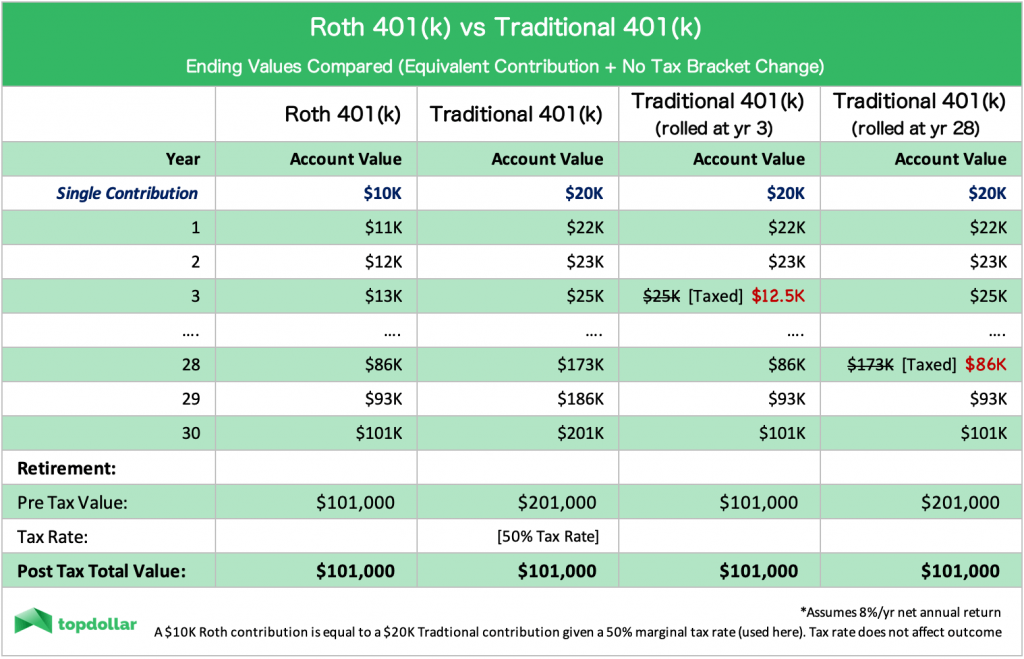

This lower tax bracket window can either come from deliberate retirement or occur sooner. The strategic opportunities that occur sooner than retirement stem from major milestones discussed below, which provide an opportunity to roll your account into a backdoor Roth IRA.

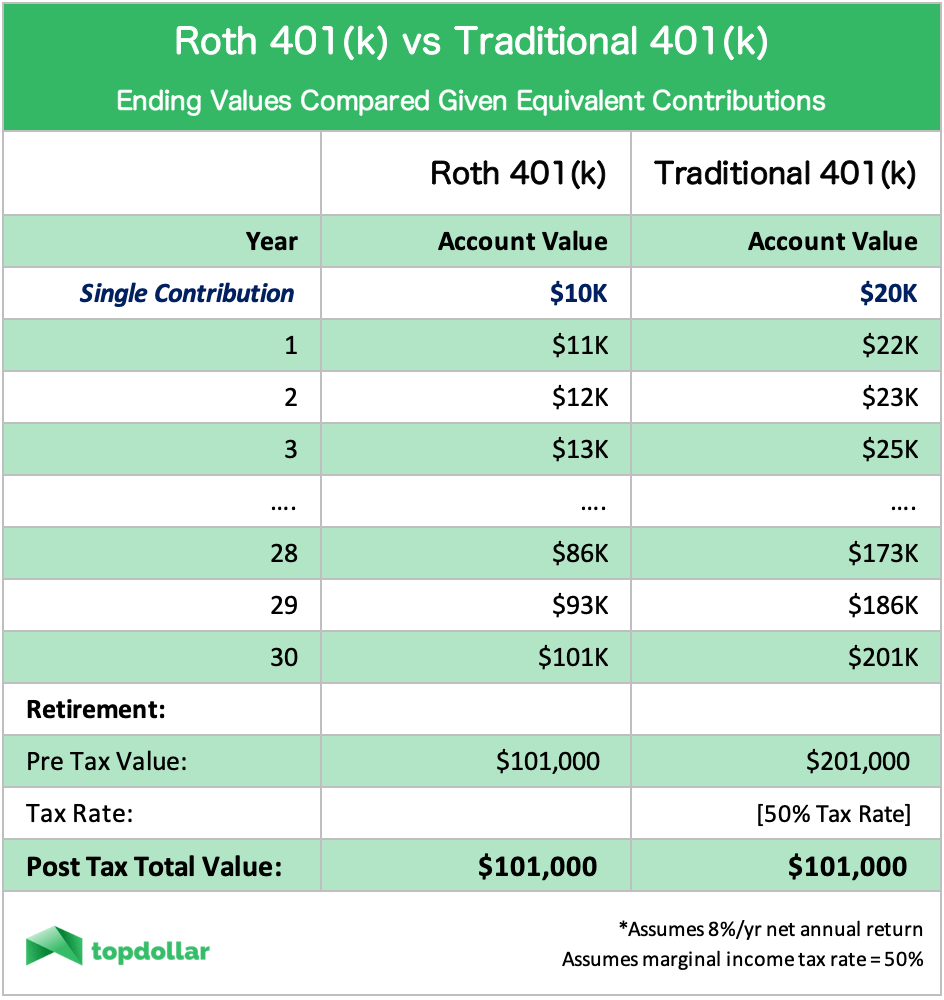

Given no change in marginal tax rate between today and retirement, an equivalent contribution in a Traditional vs Roth retirement account should yield no difference (assuming consistent returns). Below we compare a $10k contribution to a Roth vs a $20k contribution to a Traditional account. Note that the two contributions are equivalent, assuming a 50% marginal tax rate, which would cost the saver the same amount in after tax dollars. Both contributions are an investment of $10k in post tax dollars.

When A Traditional 401(k) Is The Best Choice

If you are currently paying income tax in the top federal tax bracket, contributing to a Traditional 401(k) is never a bad idea. However, here are some cases that can make the traditional option even more beneficial than a Roth.

Future Retirement Planning At A Lower Income

For many upper-middle-class to lower upper-class professionals, you may find yourself creeping into the top federal tax brackets at some point in your career. If you are fortunate enough to have high income earnings years, but anticipate you will be in a significantly lower tax bracket at retirement, taxing the tax deduction today in a Traditional 401(k) is an intelligent move.

FIRE (Financial Independence, Retire Early) Movement Planning

For younger professionals targeting an early retirement, choosing the Traditional 401(k) makes much more sense.

As a FIRE planner, you are inherently going to be moving into a budgeted, lower gross income category sooner than many of your peers. Once you achieve early retirement you will be in a prime moment to roll your Traditional 401(k) into a backdoor Roth IRA.

By planning on entering a significantly lower tax rate in the (not-so-distant) future, you should definitely take advantage of the tax deferment today while you are still earning income.

Technically, FIRE individuals have to consider two phases of retirement- the younger years (before age 59.5) and the ordinary retirement years, where they can tap their retirement accounts, social security, and medicare. The Roth IRA is a valuable tool to building significant wealth in the back end of retirement for FIRE.

If you do need to access funds before age 59.5, contributions (not total growth) can be accessed without penalty at any time. This further creates flexibility for the FIRE planner to choose the Traditional 401(k) into a backdoor Roth IRA as the top retirement account strategy for FIRE planning.

Moving: SALT Bracket Reduction

Because Traditional 401(k) contributions are made with pre tax dollars, your contribution reduces your income taxes at each level of government- federal, state, and local.

Because state and local taxes (SALT) are included in your total income taxes, any future plans to move from a high SALT area to a lower SALT region would increase the value of investing in a Traditional plan today instead of a Roth.

During the covid pandemic, many high income earners relocated from the northeast to Florida. If you are planning such a move from a SALT tax area such as this (10%+ for high earners in some cities to 0%), you can be strategic in contributing to a Traditional 401(k) which you are still in a higher tax bracket in the expensive state. After you move to the cheaper SALT region, you should then complete a backdoor Roth IRA, essentially arbitraging the difference in SALT rates.

In the event that you are planning on moving to a higher SALT region, this would be a reason to contribute to the Roth plan instead for the same logic previously mentioned.

Education: Going Back To School For An Advanced Degree

Another opportunity that may jump you from a higher to lower tax bracket in the plannable future is if you consider returning to school for an advanced degree.

Many high income earners choose to go back for specialty master degrees such as an MBA. Going back to school creates a strategic window with a lower annual income. If planning such a milestone, a Traditional plan should be chosen while still working, and then should be rolled into a backdoor Roth IRA once you are a student with a lower ordinary income tax rate.

Volatile Income Amounts

Jobs that include variable compensation (such as performance-based or sales roles) can often create years of high and low incomes. For these types of jobs it often makes practical sense to contribute to both types of 401(k)- the Traditional plan in high-earning years and the Roth plan in low-income years.

Possible Job Loss or Economic Recession

Most people don’t think about tax savings that may arise in the event of a surprise job loss or career transition. Regardless of whether such a transition may be voluntary or involuntary, having a year in a low tax bracket can be a great opportunity to roll your Traditional 401(k) into a Roth IRA.

Furthermore, economic downturns often force businesses to close and companies to cut jobs. In the unfortunate event that you get laid off during a recession, the stock market will likely also be in a negative correction. As troubling as this time may be in the moment, it would create a highly opportunistic moment to roll to a Roth IRA and pay reduced taxes on any tax free growth in the portfolio.

![]() Top Dollar Edge: Rolling from a Traditional account to a Roth account may seem like you are realizing a lot of taxes, but remember that your traditional account will all be taxed regardless during future retirement. When deciding to roll to a Roth, you should be concerned with your current marginal income bracket you will pay when rolling vs. your anticipated bracket at retirement.

Top Dollar Edge: Rolling from a Traditional account to a Roth account may seem like you are realizing a lot of taxes, but remember that your traditional account will all be taxed regardless during future retirement. When deciding to roll to a Roth, you should be concerned with your current marginal income bracket you will pay when rolling vs. your anticipated bracket at retirement.

Note that Roth accounts require a 5-year holding period, as well as a minimum age of 59.5 for withdrawals.

When A Roth 401(k) Is The Best Choice

Highest Taxable Income Bracket At Retirement

If you anticipate that your taxable income will keep you in the highest tax bracket at retirement age, then the best option is likely the Roth 401(k). Of course, all state and local taxes need to be included in your decision. As discussed previously, any plan to move to a lower SALT region would favor a contribution to the Traditional 401(k) now, and rolling to a backdoor Roth IRA once you have moved (all else equal).

Assuming no significant difference in SALT taxes, the Roth 401(k) is favored for two reasons:

- Greater contribution amounts

- More straightforward to roll a Roth 401(k) into a Roth IRA

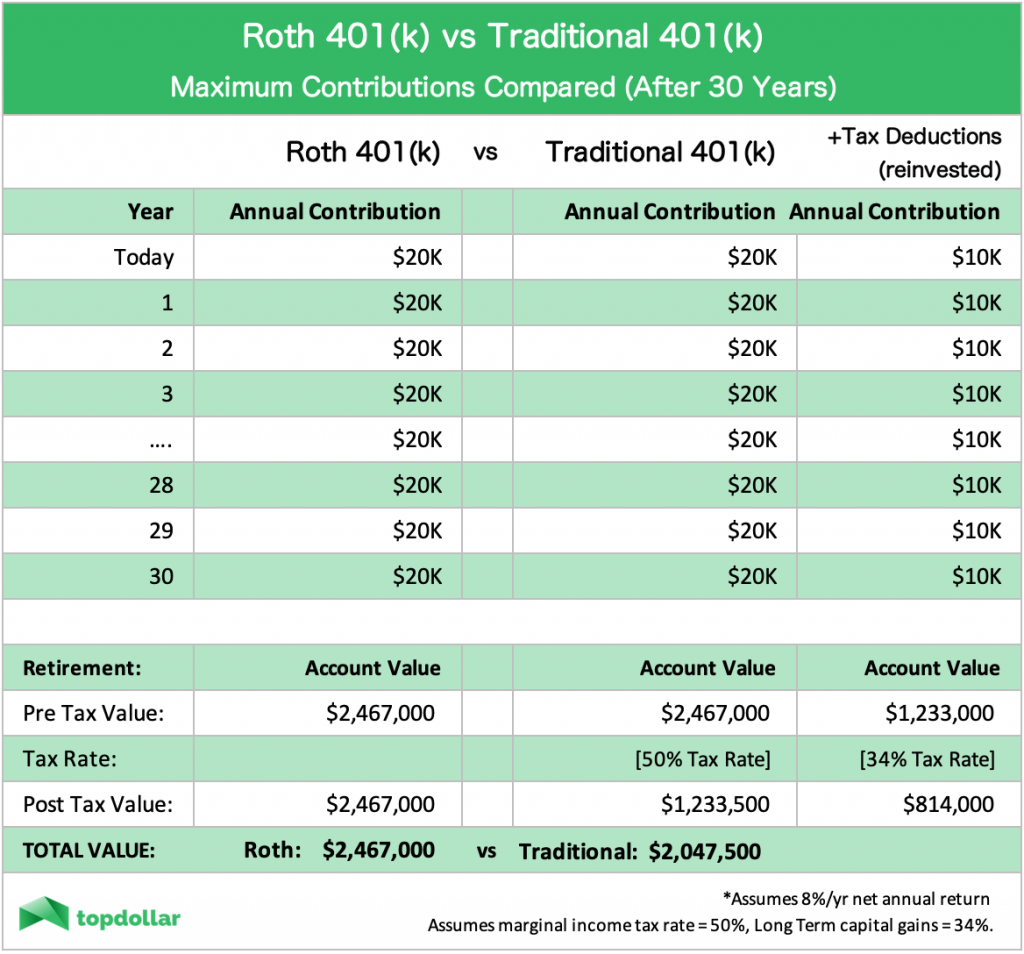

The Maximum Contribution Category

If you are a high-income earner, I assume you are trying to maximize how much you can contribute to your retirement account. If you find yourself in the “maximum possible contribution camp”, the Roth 401(k) account provides a greater net amount that you can contribute, because the annual contribution limit is made with after tax money.

For example, let’s say you are in the 50% total marginal tax rate (including SALT), the effective net total contributions impact is illustrated below if you were to contribute a hypothetical maximum of $20k per year for 30 years.

Note that by contributing to the Traditional 401(k) you would receive an immediate cash savings of $10k/year ($20k x 50%), so for fair comparison, I assume you reinvest that “free” $10K at the same annual return, and then take long term capital gains (not ordinary income gains) at the end of 30 years.

Backdoor Roth Conversion Considerations

Backdoor Roth conversions can be a bit more complicated if you have multiple regular IRAs. Legislation could also change, closing the current window, which allows high-income earners to convert Traditional accounts into a Roth IRA. Because of these unlikely, but possible changes, I would prefer to open the Roth account sooner than later, so I would recommend choosing the Roth 401(k) today over the Traditional account.

Roth IRAs not only have more flexibility in investment options than comparable 401(k) accounts, but they also have the added benefit of not requiring any minimum distributions (RMDs). Avoiding premature taxation from RMDs makes the Roth IRA a dominant tool for growing your money tax-free forever and an effective estate planning tool.

For anyone in an ultra-high net worth category, opening the Roth 401(k) and later rolling to a Roth IRA, allows for the maximum amount of tax difference and the ability to avoid RMDs if the money is not immediately necessary. Of course, tax-free withdrawals on the entire account are the hallmark of any Roth account.

Other Considerations

Legislation Changes

Tax bracket can and do change over time as politicians and legislation change policy. However, I don’t believe in trying to predict future tax rates and income limits that are purely speculative. It makes sense to plan based on the current tax laws, but trying to guess future tax rates is a poor decision as policy changes may be either beneficial or detrimental.

Employer Match Creates Both Types of Accounts

If your workplace offers any form of employer contributions or match on a 401(k), you should take full benefit of the maximum amount. The match is free money, and you should always aim to contribute as much as necessary to your 401(k) to take advantage of the maximum employer contribution possible.

Often employers only match on a pre-tax basis, essentially forcing you to create a second account- a Traditional 401(k) for your employer match portion. This is fine and should not change your decision process in whether to contribute to a Traditional vs Roth account with pre- or after tax money.

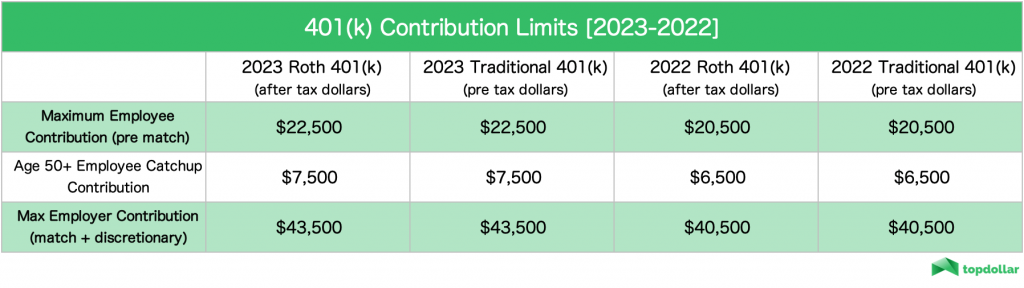

Annual Contribution Limits [2023]

There are no income limits for Roth 401(k) or Traditional 401(k) accounts (unlike a Roth IRA), so you are eligible for contributions as long as your employer offers the account. Below are the contribution limits for both 401(k) account options.

Have any questions or comments? Feel free to contact me.

References:

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.