‘Employer 401(k) Match Counting Towards 401(k) Contribution Limits’ and Other Common Mistakes People Make

Employer contributions to your 401(k) constitute a significant benefit that should not be overlooked. These contributions are made in tax-advantaged retirement accounts and provide owners with additional financial security and savings post-retirement.

Simply put, the Internal Revenue Service (IRS) establishes different contribution limits for 401(k) contributions made by an individual separate from 401(k) contributions limits made by an employer match or profit-sharing contribution.

In this article, we’ll review the employee 401(k) contribution limits and employer 401(k) match and profit-sharing contribution limits. Additionally, we’ll explain the differences between different types of retirement accounts and the contribution constitution.

401(k) Employee Contribution Limits Explained

The 401(k) is a retirement savings plan protected by the U.S. Internal Revenue Code to create a retirement account for employees’ future benefits. The employee who signs up for a 401(k) must agree to have a percentage of your gross income paid directly into this account. Income tax will apply depending on the type of 401(k) plan you have.

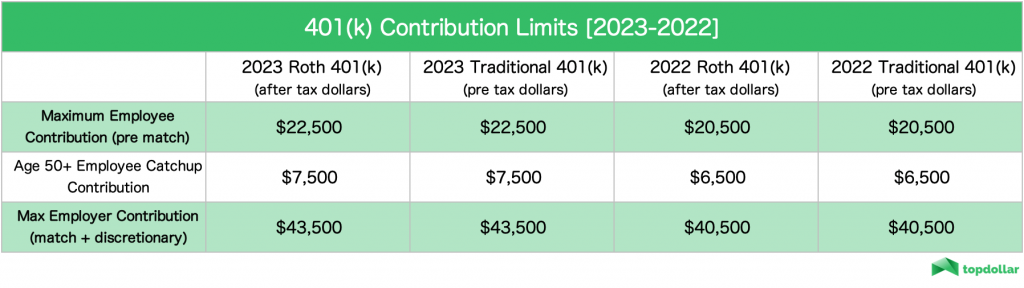

The following chart defines the maximum current contribution you can choose to make yourself. Note that the 50+ year-old catch-up contribution is an additional top-off you can make if you are over that age, increasing your maximum contribution.

Separately, your employer is bound to a different maximum contribution limit than individual contributions for your 401(k). However, most employers have matching policies that won’t reach their maximum allowed threshold. Unfortunately, besides following your company’s guidelines to maximize their contribution, there is nothing additional you can do to maximize an employer’s contribution to the allowable IRS limit.

Sadly, you cannot personally contribute or make up the difference between what an employer contributes and the maximum amount they are allowed to contribute. Some employers choose to contribute a profit share or discretionary bonus to maximize the employer 401(k) contribution portion. Any contribution made by an employer, whether a percentage match, profit-share, or bonus, is all combined and capped at the annual limit set by the IRS.

All limits are the same for both a Traditional 401(k) and a Roth 401(k). Unsure if a Traditional or Roth 401(k) is better for you? Check out this article for an in-depth analysis.

A Traditional 401(k) contribution is deducted from gross income and can therefore be reported as a tax deduction for that year. Do note, however, that you pay income tax on withdrawals.

A Roth 401(k) contribution is deducted from the employee’s after-tax income, resulting in no tax deduction for the contribution year. However, no additional taxes are due when the money is withdrawn during retirement.

Because of the tax benefits offered by 401(k) plans, annual contribution limits are set for employee contributions depending on your account type. The annual limits are subject to change by the IRS each year based on inflation and cost of living.

Safe-Harbor 401(k)

The Safe Harbor 401(k) plan is similar to the traditional plan and ensures that all eligible participants receive employer contributions. In this plan, the employer contribution is fixed and mandatory. Like the traditional 401(k) plan, the employee deferral limits are the same maximum contribution limits. Older contributors, those above 50 years old, can also contribute the additional catch-up benefit.

Simple 401(k)

Small businesses can establish a simple 401(k) plan with 100 or fewer employees and self-employed individuals. For these plans, the maximum contribution limits are listed in the following section.

Solo 401(k)

A solo 401(k) plan is also referred to as a one-participant plan, a Uni-k plan, or an Individual 401(k). The plan is designed for one-person businesses and has contribution limits as such:

There are also particular additional contribution limits for highly compensated employees. By definition, highly compensated employees are those who owned more than 5% of the interest in the business at any time during the year or preceding year, those who received compensation of more than $125,000 the preceding year and, if the employer chooses, was in the top 20% of employees.

What Are Employer Contributions?

Employer contributions are the financial contributions that employers make toward your investment fund. In the context of your 401(k) account, the employer’s matching contributions are the dollars your employer contributes to your 401(k) account, depending on the type of 401(k) account you own. For example, in 2020, the average employer match was about 4.7% of the employee’s gross salary.

The matching contribution offered by your employer means that the company will match the contributions you make up to a certain threshold as determined by your 401(k) plan. Employer matching contributions are as follows:

Partial 401(k) Match

In a Partial 401(k) match, the employer matches a fraction of the employee’s contribution with the total contribution capped as a percentage of the entire salary. Some employers would choose to match a percentage of their employee’s contributions, which is a benefit that employees should take full advantage of, given it’s effectively free money.

Dollar-For-Dollar 401(k) Match

Dollar-for-dollar matching is the most effective way to maximize your employer’s contribution portion. Dollar-for-dollar contributions are a matching method where the employer contribution equals 100% of an employee’s contribution. In that way, the employer contribution is equivalent to yours – meaning that if you put $10,000 into your 401(k), the employer will have to match it for every cent.

Although this will not get the employer to maximize their total allowable contribution, it will produce significantly more contribution than the percentage match.

Non-Matching 401(k) Contributions

Non-matching contributions are made by employers regardless of whether an employee contributes to their plan. The basis of the employer’s contributions remains the company’s annual profit or revenue growth. These additional contributions are generally necessary to reach the maximum employer contribution limit defined by the IRS.

As discussed previously, if your employer chooses not to make any other discretionary contributions (and most do not), there is no action you can take. You cannot make up the difference personally for any portion of the employer contribution that is under the limit.

For those over the age of 50, you can make additional contributions to your 401(k) plan. As mentioned before, taxpayers 50 and older can make additional catch-up contributions, increasing their personal contributions.

Does the Employer 401(k) Match Count Toward the 401(k) Contribution Limit?

Just to be extra clear, the employer match does not count toward the employee’s annual contribution limit. However, the IRS does limit the contribution to a 401(k) from both the employer and the employee.

Essentially, the IRS places separate contribution limits on the individual contribution, the employer’s match, and the combined employee-employer contribution in your 401(k). If you include catch-up contributions, this total limit will be increased.

Do You Pay Income Taxes On Your 401(k)? (And Other Fees)

Some people are unsure how taxation works for 401(k) plans. We have already mentioned how your 401(k) distributions introduce additional income taxes based on your yearly income. If you’re younger than 59.5 years old at the time of distribution, you’ll be looking to add a 10% early withdrawal penalty in most cases, and so is never advised. However, Roth 401(k) contributions do not tax you upon withdrawal as it is taken from your after-tax income.

Be especially careful of performing 401(k) withdrawals while still earning. The withdrawal could push your overall annual income into a different tax bracket and subject you to a higher rate.

You should also be aware that any excess contributions or deferrals are subject to penalties should they not be withdrawn by April 15. The withdrawn excess is includable in your growing income for the year before but is not subject to the additional 10% tax on early distributions. If, however, you fail to withdraw your excesses before April 15, your excess deferrals will be taxed twice, once when contributed and again after distribution. On top of this, the IRS will charge a 6% penalty on any additional amounts contributed to your 401(k) for the years you don’t correct the error.

What Does This Mean For You?

The 401(k) is one of the most powerful tools you could use to save for your future. Because the contributions your employer matches do not impact your individual contribution limit, you could contribute money to your account to the maximum individual limit. Get your 401(k) set up as early as possible to take full advantage of your tax-advantaged retirement plan.

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.