How Are RSUs Taxed: Restricted Stock Units Guide

Some employers offer restricted stock units (RSUs) as part of employee compensation. Have you recently received a job offer or compensation structure that involves RSUs, and need to better understand how they work?

This type of equity compensation is becoming increasingly common and can offer valuable upside, but also carries additional risks. Understanding the unique tax structure of RSUs is straightforward, but there are some smarter tax decisions you can choose to make only when the stock is first granted.

When I received my first RSUs as compensation, I was confused and didn’t quite understand some of the important tax decisions to be made. Let my research and personal experience act as your guide, as I was able to uncover all the benefits and detriments of strategies such as pull-forward tax elections and hedging.

Let’s dive in and explore the basics of RSU, how RSUs are taxed, and what advanced tax strategies you can choose to elect to optimize your future tax obligations.

What Are RSUs?

Restricted stock units (RSUs) are a form of employee compensation most typically issued by companies in high-growth industries. RSUs allow an employee to participate in equity ownership (stock) in their firm which can provide significant upside if the company continues to grow and prosper.

During the previous generation, stock compensation used to be reserved for higher-level management. Today, however, more companies are offering RSUs as a way to attract and retain top talent. Firms have come to understand that as shareholders, employees feel more connected to their employer’s mission or success.

As stock compensation has become more common, restricted stock units have become more standardized. The “restricted” part of RSUs limits how and when shares can be sold. Most employees need to stay with their employer for several months or years until the ‘vesting date’ at which they actually receive ownership of the stock. However, some companies have more restricted stock unit plans that combine vesting schedules with additional restrictions. Let’s look at the two types of RSUs.

Single Trigger RSUs (Time Vesting)

Single trigger RSUs vest your shares based on a specific time schedule. Single trigger RSUs can be classified as graded or cliff depending on the structure of the vesting schedule.

Example: You are granted 3,000 RSUs all of which become yours after 1 year.

Example: You are granted 3,000 RSUs of which you receive 1,000 RSUs per year over 3 years time.

Once the shares vest, you are free to do with them as you wish. You may continue to hold them as investments or choose to sell them.

Double Trigger RSUs (Time + Performance-Based Vesting)

Some firms have additional criteria restricting a holder’s ability to sell their shares. These double-trigger RSUs include time vesting in addition to a liquidity event trigger.

Common liquidity events identified in double trigger RSUs include initial public offerings, direct listings, sales or mergers, or private equity investments. These types of liquidity events bring in new investors and provide a more liquid market for the shares to be easily sold.

Firms that don’t have opportunities to raise investor capital early on are more likely to have double trigger RSUs. Although meeting the criteria for double trigger RSUs is significantly more challenging, these types of RSUs can often more lucrative, as they are a form of early stage investing.

Most employers use milestones beyond your direct reach or influence in a double trigger RSU compensation plan. Therefore it is important to be aware of the necessary liquidity triggers and make an assessment of the likelihood of success before accepting this type of compensation.

What happened to RSUs If You Leave Your Company?

If you have not yet vested all of your RSUs and you leave your company, you will usually forfeit any unvested shares. In this manner, RSUs are like bonuses that are awarded only at the vesting dates. You should always take into account any upcoming vesting dates before voluntarily leaving your company.

If you are vesting on a graded schedule you can always keep any vested portions of your grants that have been reached. For example let’s assume you are granted 4,000 RSUs to be vested at 1,000 shares per year, for 4 years. If you were to leave your company after year 2 but before the end of year 3, you would be allowed to keep the 50% of your shares that vested (2,000 shares).

In rare cases, employers may offer to accelerate your RSUs to vest as part of severance, retirement, or disability packages. These cases are quite uncommon and are often the exception and not the norm.

How Are RSUs Taxed?

RSUs have unique tax rules compared to other forms of compensation and stock options. Let’s jump in and review the RSU taxation rules in detail.

Taxed As Ordinary Income While Vesting

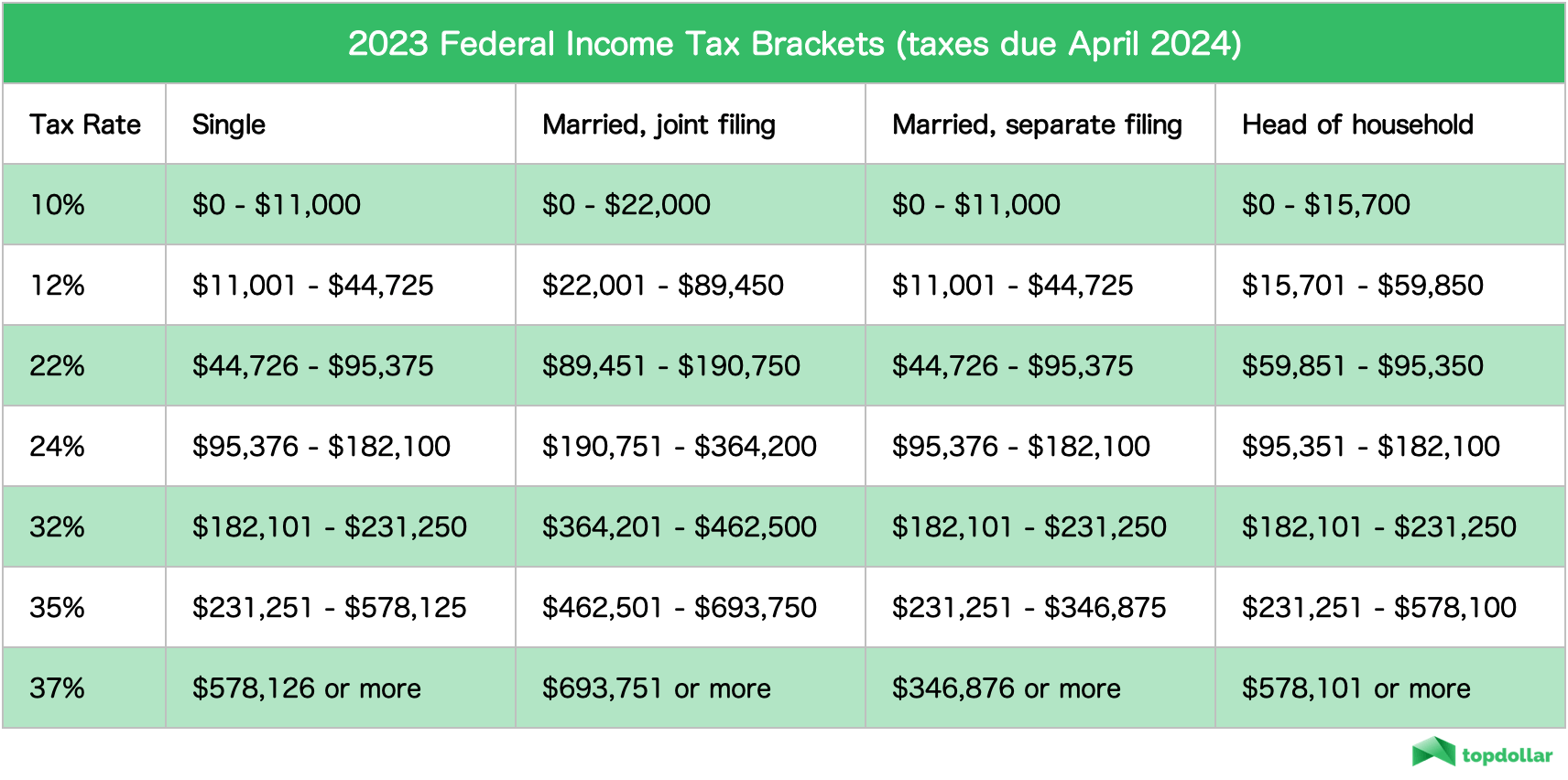

While restricted stock units are promises of future stock, they are not truly yours until they vest. Likewise, the IRS will only tax RSUs in the year they vest as ordinary income.

Taxed As Capital Gains When Sold

Once your RSUs are vested they are technically no longer restricted. You now own the stock as if you purchased it outright. The IRS now applies the same tax rules as if you bought any other stock.

The cost basis of your stock is simply the price that was used to calculate your ordinary taxes owed (the price on the vesting date). Any future price increase or decrease in the stock price will create a capital gain or loss, which will only be realized upon selling the shares.

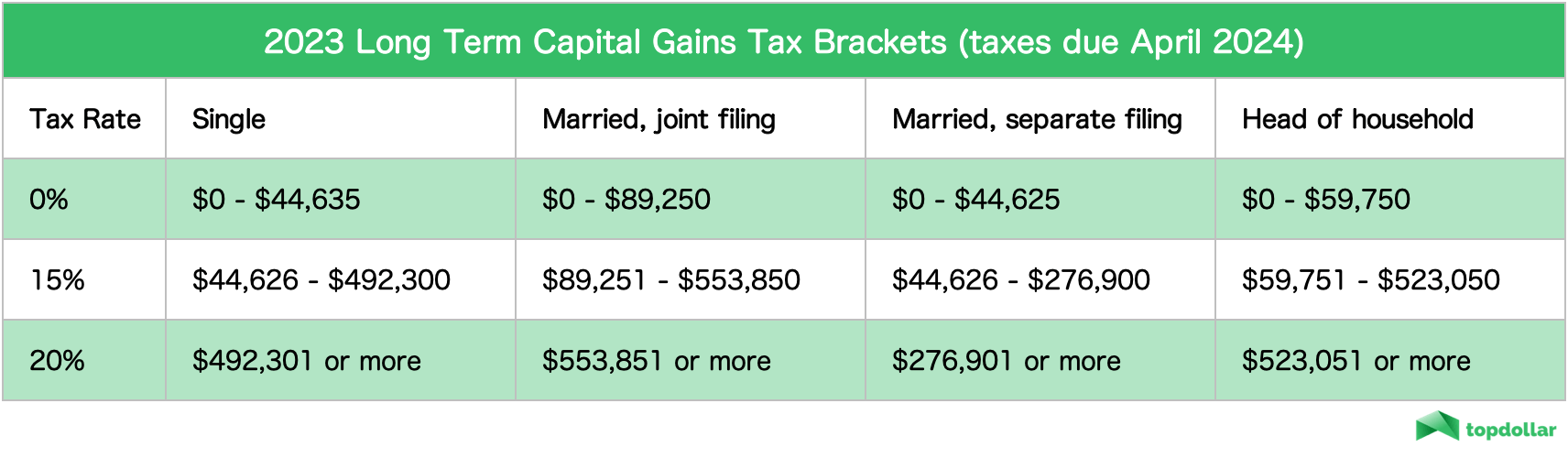

If you keep your stock for over a year, you’ll be taxed at a more favorable long-term capital gains tax rate. However, if you sell the shares within a year or less, short-term capital gains rates will apply. Capital gains taxes are only assessed on profits from the cost-basis price, so if you sell your shares at the price they vest you will not owe any additional taxes.

Are RSUs Taxed Twice?

There is a common misconception that RSUs are taxed twice, but this is not actually the case.

RSUs are taxed as ordinary taxable income when they vest, which is no different than how any ordinary wages or bonuses would be taxed. At this point you are always free to fully sell your RSUs, only pay ordinary taxes, and would not owe any additional taxes.

If you were to invest your wages in any stock (or keep it invested in your company) you would always owe capital gains taxes on any potential gains. This is simply how the IRS applies capital gains taxes on any investment. Of course, this only applies to investments that appreciate in value or pay dividends.

Because taxes are treated as investments after vesting, there is no taxable advantage in keeping your RSUs after they vest. You can choose to keep your company stock if you believe in the future success and profitability of the company. However, it is often smarter to diversify your investments. I recommend having no more than 20% of your net worth in any single investment (including your company).

Tax Withholding Practices for RSUs

Employers are required to withhold taxes on behalf of their employees. Vested RSUs will appear on your W2 statements just as any other wages.

As RSUs vest they will be treated as income and reported on your W2 tax forms, on Box 14, under “other” compensation. Make sure to check this number to make sure it aligns with what you expect to ensure that your taxes are being assessed on the correct value.

Note that this vested total value will also be included in your total wages on Box 1 on your W2 form.

Your employer will withhold taxes on your behalf, however, in order to raise the money to pay taxes you will have three options:

- You keep all your shares and fund the withholding tax out of pocket.

- Tender (sell) some of your vested shares in order to cover the tax bill.

- Sell all your shares, and cover the withholding tax with some of your proceeds.

The tax implications of these choices are all exactly the same. No matter which option you choose you are still paying ordinary taxes on the entire vested value.

Companies often withhold taxes on bonuses or RSUs at fixed rates which are not necessarily at your specific ordinary income tax rate. If your company does not withhold enough taxes, you should pay estimated taxes to avoid tax penalties.

Advanced Tax Planning: 83(b) Elections and Grant Dates

An 83(b) election can offer significant tax savings, but there are potential downsides. Before diving into the details of 83(b)s we first need to define “grant dates.”

Grant Date

The grant date is the official date a company contractually promises RSUs to an employee. Grant dates are usually set by the employer around the time you sign a willful employment contract. Grant dates usually have no importance for tax purposes, unless you decide to make an 83(b) election.

83(b) Advantages

The 83(b) election allows a RSU recipient to declare the fair market value on the grant date for tax purposes, instead of using the future vesting date. The primary benefit occurs if the shares are worth more in the future than today.

Under 83(b), ordinary taxes are owed on the price at the grant date. Any appreciation after the grant date will be considered a capital gain for future tax purposes and will benefit from the long-term gains tax rates if held for longer than one year.

Here is how it works. You need to send the IRS a certified letter declaring your 83(b) and report your stock’s fair market value within 30 days of receiving the grant. You report the fair market value, and your unvested shares will be valued at the grant date price. You pay the taxes now as ordinary income tax on this year’s tax return, although the shares have not been vested.

Furthermore, it is recommended to file an 83(b) if there is any chance your RSUs will pay a dividend during the vesting period. In this situation, dividends are collected and deferred until the shares vest. The IRS applies more favorable tax rates on dividends. By filing an 83(b), any dividend received will not be taxed as ordinary income. This filing ensures your dividend qualifies as dividends for tax purposes.

83(b) Downside and Risk

The main downside of the 83(b) is that you have to pay income tax immediately. Tax is paid on unvested shares, and cannot be reclaimed even if the shares never vest. Because you are required to pay tax immediately under the 83(b) option you should only consider electing under the following circumstances:

- You have enough free cash to cover the taxes owed. The current valuation of the RSUs (unvested shares x grant date price) will be taxed at ordinary tax rates in the immediate tax year.

- You are highly confident you will be able to achieve the full vesting criteria. You will pay tax regardless of whether your shares ever vest.

Employees don’t own RSUs until the vesting period ends. For example, if the company awards you 1,000 RSUs and allows 20% of the shares to vest each year. So, you’ll own 200 RSUs annually. If you quit after 3 years, you’ll get 600 RSUs. Unfortunately, 83(b) has a more stringent approach, and you will have already paid taxes on the unvested 400 RSUs. These taxes you paid will not be refundable.

For this reason, it is imperative that you weigh the likelihood of vesting against the potential tax savings.

In some cases, an RSU plan may require you to buy a portion of the stock at the grant date. Any amount purchased by you would be treated as a capital loss in the event you relinquish your rights to the stock units.

Restrictive Stock Units: Pros vs. Cons

Let’s review the pros and cons of RSUs to summarize this type of compensation.

Pros:

Cons:

Although unvested RSUs don’t directly offer dividends, your employer can pay dividend equivalents into an escrow account to help offset withholding taxes. The company can also reinvest the dividend equivalent by purchasing additional shares.

Employer Perspective

Restricted stock units offer several benefits for employers. Similar to stock options, the value of RSUs is linked to the company’s share price. So, employees are incentivized to help their employer perform better to boost the value of their shares. Employees cannot sell their RSUs until they vest. Unlike a cash bonus, RSUs can entice employees to stay with the company for the long term. RSUs also allow the employer to defer issuing RSUs to delay the dilution of their stocks.

RSUs vs. Stock Options Differences

Stock options allow employees to acquire the company’s shares at a specified price (the strike price). However, options will only have value at a future date if the stock price is above the strike price.

RSUs are always worth the full value of the share price upon their vesting date. RSUs are essentially stock options with a $0 strike price, meaning you receive the share for no additional cost once they vest.

Let’s take a look at two potential options offered to an employee. Option #1 receives $50K worth of RSUs vs. option #2 receives $50k worth of stock options.

The stock options have built-in leverage, allowing an employee to make more money if the share price increases. The stock options also have additional risk, and the options can become worthless if the stock price falls.

Smart Tax Strategies for RSUs

Vested stocks will always be taxed as ordinary income. The only tax savings action you can take is to file an 83(b) to reduce your potential tax burden.

However, once your RSUs vest, you can still delay or cut your tax bill. Here are two RSU tax strategies to help you manage your tax obligations more efficiently:

Take RSU Capital Gains Against Any Deductible Account Contributions

If you are not yet maximizing the total contribution limits of your 401(k) or other retirement plans, your RSU gains are a smart source for increasing contributions.

Retirement accounts should always be maximized if you have the means to save more. I would recommend selling RSU up to the amount that could be offset with deductible contribution limits.

Furthermore, investing in your retirement plan instead of holding more company-specific exposure provides better diversification of your investment portfolio.

Defer Taxes by Hedging With Options

Defer taxes by hedging with options if you are trying to delay taxes to a more favorable year. You can also use this strategy if you want to maintain your position in the company’s stock but reduce exposure. How? Here are two hedging strategies to defer your taxes:

The Covered Call: Under this strategy, you sell call options above the current price. You can generate additional income if the share price remains constant or goes down over the next year. However, the covered call strategy caps your maximum gain on the stock position. If the price rises, your gains will be capped to the strike price.

The Collar: You can implement this strategy in two steps. First, you hedge the downside by buying a put. Then, sell a call option. Buying a put can be expensive. So, you’ll need to sell a call to offset the costs. Under this strategy, you’ll generate minimal income.

Although both strategies come with risks and tradeoffs, they can help you defer the sale of your RSUs and delay the taxes. Consider if either option is right for your circumstances before the end of the tax year.

RSU Takeaways:

Have any questions or comments? Feel free to contact me.

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.