What Happens to Your 401(k) When You Quit or Get Fired?

Most investors are familiar with 401(k) plans, which offer valuable tax advantages to help employees save for retirement. Nevertheless, over the course of a lifetime, people often change jobs, sometimes by choice or at other times involuntarily.

So, what happens to your 401(k) when you quit or get fired? The good news is the hard-earned money that you contributed is safe. However, there are some instances where you may have to forfeit some of the money your employer contributed.

However, there are some important details you need to be aware of to make the smartest money decisions for your retirement savings when leaving a job. Some strategies can save you significant money, so let’s explore your options and make the wisest decisions.

What Happens To Your 401(k) When You Quit or Get Fired?

First, take a deep breath. Leaving a job can be very stressful, but you don’t need to be worried about losing your retirement savings. Any money you contributed to your 401(k) plan is protected and cannot be taken away by your employer, even if you left on poor terms.

However, some of your money likely consists of your employer’s match or profit-sharing contributions, which remain unvested for a specific period. In short, you don’t own your employer’s match until those dollars are fully vestest in the plan. Usually, you lose all unvested funds in your 401(k) even if you leave on excellent terms.

Vesting

Vesting determines the proportion of your employer’s contributions you’ll get to keep in your 401(k) after you leave your job. It doesn’t apply to any of the funds you have contributed yourself to your account. For example, if you are 100% vested in the plan, you qualify to keep all of the money in your 401(k). You can also take other types of contributions to your retirement account. Whether you attain “100% vested” or some different percentage depends on your specific employer’s vesting schedules.

- Graded vesting: This vesting schedule allows you to keep a portion of the 401(k) match based on your years of service. Most employees under a graded vesting schedule qualify for the total 401(k) match after serving the company for five or six years.

- Immediate vesting: If your employer offers immediate vesting, you will have access to your 401(k) match as soon as their contributions hit your account.

- Step-up vesting: This schedule allows you to gain a percentage of the contribution made by your employer each year as time passes.

Before you quit your job, you should inquire about the company’s vesting schedules from your employer’s human resources department. This information can help you determine whether you’re close to becoming fully vested and how much money you’ll essentially be “giving back.” You may only need to stick with the company for a few weeks or months to keep the entire amount in your retirement account.

Can You Leave Your 401(k) With Your Former Employer?

Yes, you can. But this option is usually only available to employees who have invested more than $5,000 in their plans. Most plans allow employees with substantial savings to leave their 401(k) even after leaving the company. But this arrangement comes with some constraints. Former employees can’t make contributions to their old employer’s plan. This option also limits your control over costs and investment choices. Furthermore, leaving a 401(k) with an old firm results in another account you’ll have to track and manage.

Employee Contributions vs. Employer Contributions

After enrolling in your company’s 401(k) plan, a percentage of your paycheck is paid directly into your retirement account. These allocations, which come from your paycheck, are known as employee contributions.

Your employer can match part or all of your contribution, which is laid out in the 401(k) policies. Often the details of the company match are laid out when you first enroll in the 401(k), but your HR department should be able to provide you with this information at any time.

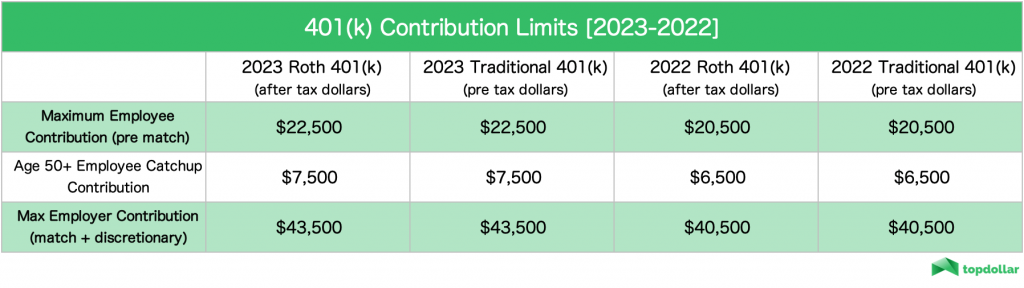

You can elect an employee to contribute up to the maximum amount (limits are updated annually by the IRS).

The maximum amount of your employer’s match is set forth based on your company’s 401(k) matching policy in accordance with IRS guidelines which outline parameters. Under these guidelines, employers could also choose to “profit share” and make additional 401(k) contributions to valuable employees- basically in the same way bonus are sometimes awarded.

Maximize Employer Match

The employer match contribution is free money which you should always aim to maximize. Often an employer will match a percentage of your employee contribution up to a maximum dollar amount. The match is an employer’s way to incentivize you to save more for retirement. I always recommend contributing as much as possible to your 401(k) to maximize as much of this free money as you can manage.

Of course, as mentioned above, employer-matched contributions often vest over time, so a portion of it may be “clawed back” from your 401(k) when you quit or get fired.

Strategies For Your 401(k) When You Leave Your Job

Your retirement savings will be secure, but you have several options available. First, take a breath. None of these strategies need to be performed immediately. Before shifting from one job to another, take some time for yourself to consider what future business, hobbies or passions you want to pursue next. Once you feel settled and have taken the necessary time to consider your future career or business move, consider your following options.

Roll Over Your Retirement Account

When you quit your job or get fired, you have three general options for your 401(k). You can roll it over, cash it out, or leave it with your old employer.

Switching or leaving a job grants an opportunity to roll over your old 401(k) plan into a better or cheaper plan. What are your rollover options? You can roll over your 401(k) to your new employer’s retirement plan or to an individual retirement account (IRA).

Roll It Over to Your New Employer

If you quit your old job to join another company, you can roll over your 401(k) plan to your new employer’s plan. The main reasons you would choose to do this are for consolidating accounts or if you prefer the investment options in the new company’s 401(k) plan.

401(k) plans are notorious for having limited investment options, and some plans have high fees. Older 401(k) plans often offer just a few mutual funds or target date funds, whereas some newer funds offer broader options you may be interested in. Fees differences include management fees of the funds you invest in and any general account maintenance fees which may be charged annually or more frequently.

If you prefer your new company’s 401(k), check first whether your new job accepts rollover contributions. However, you may not transfer your 401(k) balance into your new plan on your first day. Some employers do not allow new employees to enroll in a retirement savings plan for months, in which case you’ll have to wait until you are eligible to join your new employer’s plan. Before you roll over your old 401(k), ensure that your new account is ready to receive contributions.

Roll It Over Into an IRA

An alternative option for your 401(k) is to roll your account into a rollover IRA. Rollover IRAs are tax-advantaged retirement accounts with similar benefits to 401(k)s but offer many more investment options than 401(k)s, including individual stocks, bonds, and ETFs. Additionally, because of the competition between brokerage firms for new accounts, Traditional IRAs usually have lower fees than 401(k)s, often with account fees as low as zero, depending on balances.

According to 401(k) rules, your employer can move your 401(k) savings into an IRA if you have $1,000-$5,000 in your account. If you have less than $1,000, your previous employer can cash it out for you. But they’ll keep 20% tax withholding.

What if you had an outstanding loan from your 401(k)? You’ll have to repay it within a specified period. Overdue loans from the plan are treated as a distribution for tax purposes.

All financial institutions follow the same IRA regulations standardized by the IRS. But 401(k) rules depend on how your employer sets up their plans. Once you roll your plan to an IRA, you won’t have to worry about complex rules specific to your old 401(k).

Convert It Into a Roth IRA

Now may be an excellent time to consider a Backdoor Roth IRA conversion. These conversions are different than a traditional IRA rollover in that your 401(k) will incur taxes (on which a tax break was previously taken). However, the benefit is that your retirement savings will grow tax-free forever, and you will never owe taxes on any future growth and earnings.

There is no income limit when converting a Traditional 401(k) directly into a Roth IRA, as is the case in any backdoor Roth IRA conversion. Roth accounts offer many benefits over Traditional retirement accounts.

TD edge: Switching between jobs (and tax brackets) can offer a crucial tax planning window. Although such moments in life can often be quite stressful, opportunities to utilize money-saving tactics such as backdoor Roth IRA conversions should not be missed!

Backdoor Roth Conversion

You should only consider doing this variation of a Roth conversion if you can comfortably afford to pay the taxes from alternative savings or income, never from the retirement account itself. Lastly, if you are considering doing a Backdoor Roth strategy, do not roll your 401(k) into a rollover IRA, as this will create a future complexity specific to Roth conversions only.

Other Considerations

The Rule Of 55

Before converting your 401(k) into an IRA, you should be aware of one possible limitation- the rule of 55.

If you need to begin drawing from the funds by age 55, you can withdraw money from your legacy 401(k) plan without penalties. This “rule of 55” is only applicable to your latest employer. A 401(k) rollover to a new employer still allows you to benefit from this rule. By contrast, an IRA requires you to wait until age 59 1/2 to take withdrawals without incurring the 10% penalty.

How to Roll Over Your 401(k)

At its core, a rollover involves moving funds from your old account to your new plan. This rollover process can be simple if you learn the best practices. You can choose a direct transfer or an indirect rollover.

Direct Transfer vs. Indirect Rollover

Direct Transfer Rollover

A direct rollover protects you from the risk of missing a deadline. It also ensures you don’t owe taxes. A direct rollover allows you to transfer funds from your old 401(k) plan directly into another retirement account in the easiest method to choose. In a direct rollover, you set up the new account and discuss your intent with the administrator of both the sending and receiving institutions.

If an administrator insists on sending you a check directly, have the check made out to the new account. The administrator of your old plan fills out the paperwork to transfer the balance into your new account, and there is no tax withheld.

Trustee-To-Trustee (Seemless Direct Rollover)

The most ideal way to send funds in a direct rollover is called “trustee-to-trustee,” and there is nothing for you to mess up. I would always recommend requesting this type of transfer if possible. You will never have to handle a physical check, and you will not have to worry about any tax withholdings.

A “same trustee transfer” refers to a rollover within the same financial institution and is the most seamless form of a trustee-to-trustee rollover which can often be done online. For example, this would be possible if you roll your Vanguard 401(k) plan to a new Vanguard Rollover IRA.

Indirect Transfer Rollover

In an indirect transfer, the administrator sends you a personal check, and you will need to take action to deposit the funds in the new account and complete the rollover.

If you must do an indirect rollover, you’ll have 60 days to complete the deposit of the personal check into your new retirement account in order to avoid paying income taxes.

This option has several disadvantages. First, your former employer’s plan will withhold 20% of the funds for federal income tax purposes. You’ll receive 80% of your balance. Under the 60-day window, you’ll have to replace the 20% manually as well as deposit the initial lump sum check into your new account.

What happens if you don’t roll over 401(k) within 60 days?

If you’re under age 59½ and fail to deposit the entire distribution within 60 days, a 10% penalty for early withdrawal will be applied. You’ll have to pay income tax on the 20% withheld by your old employer if you roll over only 80% of the funds. To avoid paying income tax, charges, and complexities, always try to make a direct transfer if possible from your old 401(k) account to your new plan.

Cash Out Options

Can you cash out 401(k) if you lose your job? Yes, you can. However, I would not recommend this option as you’ll be required to pay taxes. Additionally, you’ll be hit with early withdrawal penalties unless you are over the age of 55.

How do you do a cash-out? First, contact your plan administrator and request a distribution form. Then, complete the form and submit it to the administrator for processing. Then, you’ll get a check for the amount of your savings. This option allows you to get a lump sum distribution. But your financial advisor won’t recommend cashing out your plan after leaving your job due to income taxes and penalties associated with this transaction.

Cash-out penalties and taxes

If you cash out your 401(k) before age 59½, you’ll have to pay an income tax and a 10% early withdrawal penalty. The tax and penalty will take a significant portion of your savings. For example, if you’re in the 24% tax bracket and withdraw $10,000 from your 401(k), you’ll receive $6,600 after paying taxes and penalties. Can you imagine how much you’ll lose if you cash out of your account each time you leave a job? Cashing out your 401(k) reduces your retirement savings unnecessarily. If you need a better cash-out option, consider a 72(t) distribution.

72(t) Distributions

A 72(t) distribution is a cash-out option that allows you to take some money from your IRA before age 59½ without the 10% penalty. Although this qualified distribution will allow you to access your money early without penalties, you will still be required to pay tax. You have to meet SEPP regulations to withdraw funds from your retirement account.

With a 72(t) distribution, payments are scheduled for five years or until you reach 59½ years. You must take at least five substantially equal periodic payments (SEPPs). Your payment amount and withdrawal schedules are determined through IRS-approved methods – amortization, minimum distribution, or annuitization.

Required Minimum Distributions (RMDs)

RMDs are the minimum amounts you must withdraw annually from an employer-sponsored retirement plan or a Traditional IRA after you reach age 72. The amount is determined by your account balance and expected lifespan, with the intent of making you pay back all the taxes you previously deferred with your pre-tax contributions.

Although you can begin withdrawing from retirement accounts by age 59 ½ without penalties (or 55 from a legacy 401(k)), by the age of 72, you must start taking from your 401(k) or IRA and start paying taxes at ordinary income rates.

You must withdraw the RMD amount each subsequent year. If you are still working for an employer at 72 or older, you may qualify for an exception to taking RMDs, but they will be required for Traditional IRA plans.

Note that Roth IRA plans do not require RMDs, giving them a decisive advantage for continued tax-free growth.

The minimum amount of required distribution is based on the current RMD calculation. Your plan administrator or account custodian will calculate your RMD and forward it to the IRS. But you can also calculate your RMD. Divide your account’s fair market value (FMV) from the previous year-end by the distribution period or expected life span. RMD is the minimum amount to withdraw, with no maximum limit. Therefore, you can always take more than the RMD amount.

Summary

You don’t have to worry about losing your retirement savings. Your savings, growth, and any vested contributions are still safely yours.

When you quit or get fired, you don’t necessarily need to move your 401(k), but there are often benefits from doing an IRA rollover or a backdoor Roth conversion.

The silver lining of having a reduced annual income after losing a job is the valuable window of a lower marginal tax rate. Remember, this moment is often an ideal time to convert a pre-tax account to a Roth account. But, of course, this only makes sense if you can comfortably afford to pay the taxes on the conversion from your savings or alternative income.

Several options allow you to secure or access the money in a former employer’s plan. As a review, your available options are:

- Leave your 401(k) with your former employer

- Roll over your 401(k) into a new employer’s plan

- Cash out your 401(k) (never recommended)

- Roll over your 401(k) into an IRA.

- Convert your 401(k) into a Roth IRA

Josh Dudick

Josh is a financial expert with over 15 years of experience on Wall Street as a senior market strategist and trader. His career has spanned from working on the New York Stock Exchange floor to investment management and portfolio trading at Citibank, Chicago Trading Company, and Flow Traders.

Josh graduated from Cornell University with a degree from the Dyson School of Applied Economics & Management at the SC Johnson College of Business. He has held multiple professional licenses during his career, including FINRA Series 3, 7, 24, 55, Nasdaq OMX, Xetra & Eurex (German), and SIX (Swiss) trading licenses. Josh served as a senior trader and strategist, business partner, and head of futures in his former roles on Wall Street.

Josh's work and authoritative advice have appeared in major publications like Nasdaq, Forbes, The Sun, Yahoo! Finance, CBS News, Fortune, The Street, MSN Money, and Go Banking Rates. Josh currently holds areas of expertise in investing, wealth management, capital markets, taxes, real estate, cryptocurrencies, and personal finance.

Josh currently runs a wealth management business and investment firm. Additionally, he is the founder and CEO of Top Dollar, where he teaches others how to build 6-figure passive income with smart money strategies that he uses professionally.